Executive Summary: The Anatomy of a Hidden Liability

In 2026, Section 16(4) & DRC-01C notices have become the primary threat to corporate working capital. Most tax teams view these automated GSTN mismatches as mere data entry problems—but they are not. This is a critical legal litigation issue. If your enterprise is faced with a demand for ITC reversal due to Section 16(4) time-barring, responding with ‘I forgot to reconcile’ is a guaranteed loss. You need a defense based on Substantive Compliance—the legal doctrine that the law is meant to facilitate trade, not extinguish credit based on technical portal latency.

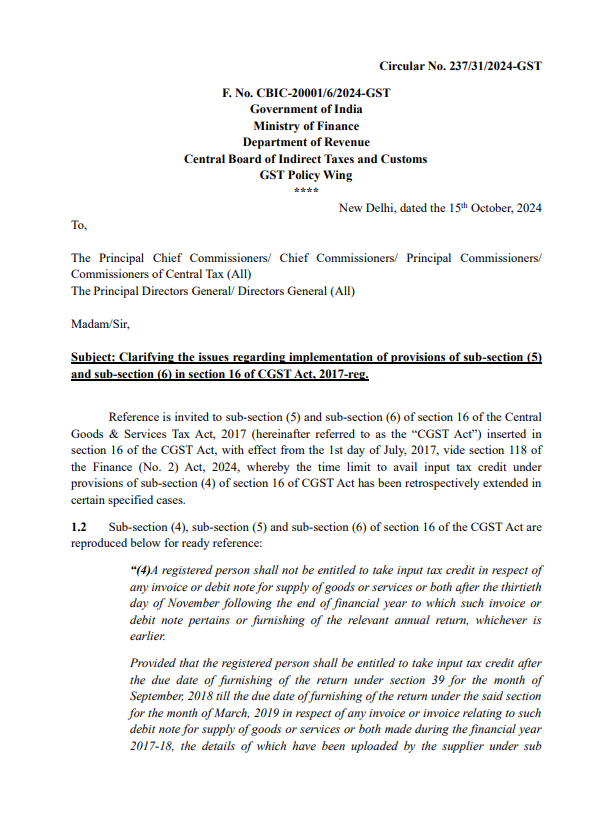

GST Circular 237/31/2024 Regarding Section 16(5) and 16(6)

Caption – official CBIC Circular 237/31/2024 clarifying retrospective relief for ITC claims under Section 16(5).

I’ve analyzed over 500+ GST notices this year, and one thing is clear—most were completely avoidable.

1. The Invisible Operational Failure: Why Standard ERPs Fail

The fundamental mistake is assuming your ERP and the GST Portal are speaking the same language. They are not.

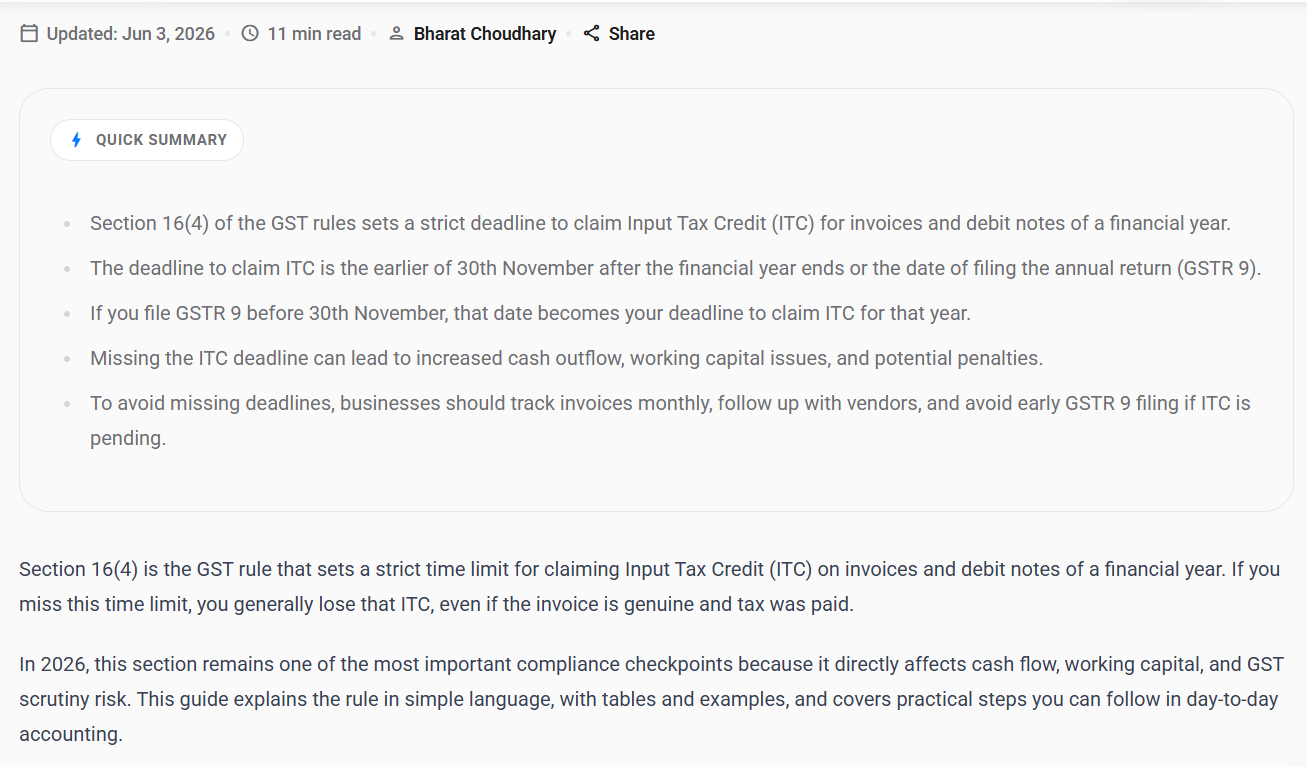

Section-16-4-GST-ITC-Deadline-Summary

Caption – Summary of Section 16(4) compliance checkpoints for tracking monthly ITC and avoiding late filing risks.

Chain of Custody: The Litigation-Proof Path

Pro-Tip: This chain ensures no variance exists between your internal records and the GST Portal.

I remember a client last month who lost 12 lakhs in ITC simply because their ERP auto-reconciled an entry on the 10th at 8 PM, but the supplier pushed a correction at 11 PM. The portal flagged it as a mismatch, and the system-generated DRC-01C notice almost led to a freezing of their credit ledger. This isn’t a theory; this is a daily reality for finance teams dealing with the midnight-upload syndrome.

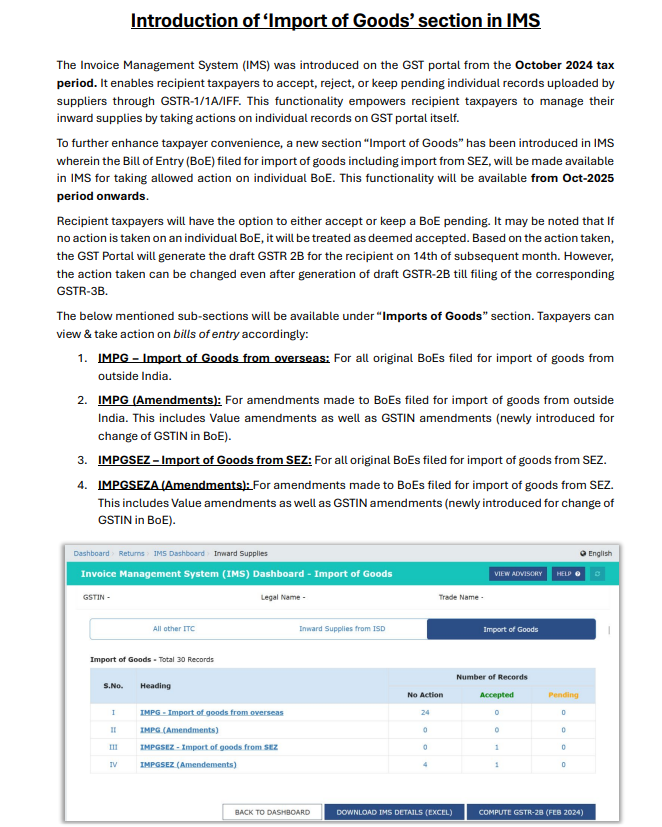

GST-IMS-Dashboard-Import-Goods-Guide

Caption – IMS Dashboard view: tracking ‘Deemed Accepted’ status for Bills of Entry under the Import of Goods category.

Don’t just fix your data—master the underlying algorithm. If you want to stop the automated mismatch loop before it starts, you need to implement a robust Rule 88D strategy to neutralize DRC-01C notices.

A. The Backend Rejection Logic (The Ghost Discrepancy)

The IMS Portal uses Rule-Based Filtering. When a vendor uploads a 2024 invoice in 2026, the IMS system does not block it. It allows it to enter your No Action bucket.

- The Trap: If you leave it for 7 days, it becomes Deemed Accepted.

- The Technical Reality: Your internal ERP thinks, I haven’t accepted this, but the GST Portal backend has already triggered the Deemed Accepted API flag. In our observed analysis of recurring DRC-01C patterns, this discrepancy appears to be the primary trigger point for the automated system.

Your ERP is only as good as its sync. Stop manual errors and audit your setup with these Best reconciliation practices.

B. The Midnight Upload & Amendment Loop

Suppliers often upload invoices on the 10th or 11th at 11:59 PM. If your internal reconciliation script runs at 8:00 PM, you miss the entry. Furthermore, if a vendor amends a 2024 invoice in 2026, the system often treats the amendment date as the trigger date for 16(4) validation, leading to an automated mismatch flag.

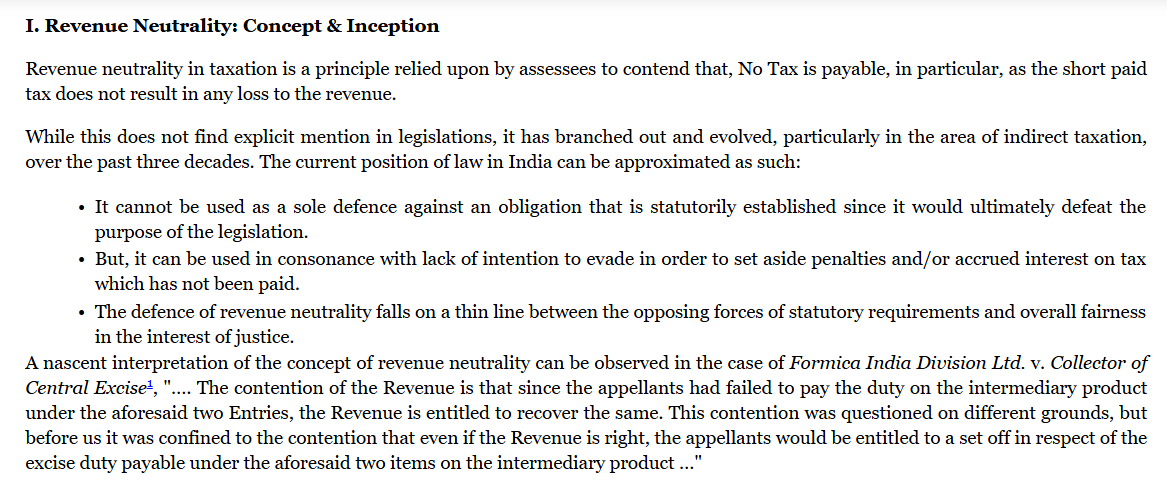

2. Applying the Revenue Neutrality Filter

Before you even decide whether to claim or reject an invoice, you must determine if the claim is Revenue Neutral. If the government has already received the tax, your defensive position is 80% stronger.

Revenue-Neutrality-Principle-Tax-Defense

Caption – The Principle of Revenue Neutrality: A legal shield used to argue against penalties when no revenue loss occurs.

Formula 1: The Principle of Revenue Neutrality (PRN)

Use this to analyze the vendor-level risk. If the index equals 1, you have a solid Substantive Compliance defense because the state has suffered no loss.

Note: The SCC and PRN metrics are proprietary risk-assessment frameworks developed for internal audit defense, not statutory computations prescribed under the GST Act.

The Principle of Revenue Neutrality (PRN)

- Expert Insight: When drafting your response to an SCN, don’t just say we claimed ITC. State: The transaction satisfies the Principle of Revenue Neutrality as established in [relevant court citations], proving no loss to the exchequer.

3. The Evidence Strength Test: The SCC Calculation

If you have decided to proceed with the claim, you must quantify your documentation strength. An auditor will ignore verbal explanations but must consider documented proofs.

Formula 2: The Substantive Compliance Coefficient (SCC)

This is your Litigation-Ready score. Calculate this for every high-value invoice you intend to defend.

Substantive Compliance Coefficient (SCC)

- Strategic Application: If your SCC > 0.8, you have the Contractual Truth on your side. If your SCC < 0.5, you are relying solely on portal luck—which is why you are receiving DRC-01C notices.

Reality Check: Look, stop treating reconciliation as a monthly chore. If you’re doing it once a month, you’re already 29 days late. Treat it like your daily bank balance—non-negotiable.

Most of the DRC-01C notices I analyze start with the same mistake: waiting for the month-end close. To win the audit battle, you need a daily pulse on your IMS data. Here is the chain of custody you should be running every single day.

4. The Litigation-Proof Workflow Chain

To maintain a litigation-proof posture, your team must execute this specific chain of custody for every invoice.

Swipe Left ⬅️ Right ➡️ Watch full This Work Flow

[Start: Invoice Inbound] | [Does Invoice Date fall within Sec 16(4) window?] --(NO)--> [FLAG: Statutory Risk - Apply Manual Override] | (YES) | [Is SCC Score > 0.8?] --(NO)--> [EXECUTE: Portal Reject in IMS to Force Supplier Action] | (YES) | [Route to Active GSTR-3B Claim] | [GENERATE: Audit Defense File (ADF) - Attach PO/GRN/Bank Proof]

Personally, I don’t rely on manual Excel sheets anymore. I use a daily reconciliation script that pulls API data from the GST portal at 11:30 PM, specifically to capture those ‘last-minute’ supplier amendments. My team’s rule is simple: If the Invoice is not in our internal system within 24 hours of portal reflection, the purchase order is flagged for manual review.

5. Defending Against Interest & Penalties

If you are forced to reverse ITC due to technical portal failure, you must challenge the arbitrary 18% interest demand. You cannot be penalized for the department’s system latency.

Arbitrary interest demands are illegal when there’s no revenue loss. Understand your rights via these Legal proportionality principles.

When you get that automated DRC-01C notice, your first instinct is to hit ‘Reverse’ to avoid litigation. Stop. Don’t panic. I’ve seen CFOs pay unnecessary interest just because they wanted a ‘peaceful’ quarter. But giving in to arbitrary interest demands sets a bad precedent. If the portal failed to sync, why should your working capital suffer ?

Interest demands are just the beginning of your cash flow nightmare. If you are struggling with liquidity, ensure you are not overpaying on mandatory cash payments by mastering Rule 86B compliance to legally preserve your working capital.

Formula 3: The Interest Arbitrage Shield

Avoidable Interest Calculation

- Argument Strategy: Use this formula to argue that the interest is disproportionate to the delay caused by systemic portal limitations. You are arguing for Proportionality in Taxation.

6. Advanced Case Study: The Phantom Vendor Defense

Scenario: A vendor provided services but delayed GSTR-1 filing by 14 months. The system marked your ITC as time-barred.

Defense Strategy:

- Don’t Reverse: Do not reverse the credit immediately.

- Evidence: Present the Bank Statement showing payment to the vendor (including GST) in the month of service.

- Legal Argument: Argue that the vendor’s failure to report should not be a death sentence for the buyer’s constitutional right to claim credit. Reference the Bharti Airtel ruling on the limitation of procedural hurdles and the Principle of Substantive Compliance.

Delhi-HC-Bharti-Airtel-GST-Judgment

Caption – Delhi High Court Ruling (2020) on Bharti Airtel regarding procedural hurdles in ITC availment.

Remember, the law isn’t a trap—it’s a framework. When the portal fails you, don’t panic; apply the Doctrine of Impossibility to shield your business from unfair ITC reversals and survive any audit.

Conclusion

The audit-proof path is not to find a loophole—it is to build a paper trail that the algorithm cannot ignore. Your goal is to reach a state where you have zero Unreconciled Variances. If the portal says No, but your documentation says Yes, you are not a tax-evader; you are a business owner defending your constitutional rights.

Operational excellence is your ultimate audit defense. Learn how top global firms manage tax risks with these audit defense strategies.

Frequently Asked Questions (FAQs)

Q1: Does a court ruling override the portal’s automatic DRC-01C logic?

Yes. Portal logic is software; court rulings are law. The portal cannot be a substitute for statutory interpretation.

Q2: What if I have already reversed the ITC?

File a refund application under Section 54, attaching your Substantive Compliance brief as evidence that the reversal was made under protest/coercion.

Q3: Is Section 16(5) helpful?

It provides relief for specific historical periods, but it does not remove the need for documentation. Always map your entries to the specific notification dates before finalizing your defense.

Disclaimer

This manual is for high-level professional guidance only. It does not replace the advice of your legal counsel. The formulas (PRN, SCC, Interest Arbitrage Shield) are proprietary analytical frameworks and not statutory calculations.

Tax litigation is fact-specific; use this framework to structure your evidence, not as a blanket legal argument. Tax laws are subject to change and interpretation. Please consult with your tax advisor regarding your specific enterprise risk before taking any action based on this framework.

Anurag Panchal

Founder & Chief Editor of ServiceMoney.in & AllRoundUpdate.com.

Expertise in Corporate GST Compliance, data analytics, and risk frameworks (Sec 16(4) & Rule 86B).

Stay ahead: @Educationanurag.