Rule 88D is no longer merely a legal provision; it serves as the ‘Automated Enforcement Engine’ of the GST portal—wielding the powers vested under Section 75(12)—capable of freezing your cash flow at any moment.

By 2026, the GST portal has evolved from a mere filing utility into an Artificially Intelligent Auditor. Here, even a minor omission within the Invoice Management System (IMS) creates a ‘High-Risk Compliance Zone’ at the intersection of Rule 37A and Rule 88D.

Is your ITC claim legally prepared to withstand this algorithm-driven scrutiny and the ensuing automated demand notices?

If you are managing portfolios with turnovers exceeding ₹50 Crores, a single ‘click’ or ‘inaction’ in the IMS can trigger a chain reaction that hits your cash flow, your credit rating, and your legal standing.

1. Decoding Rule 88D: The Automated Executioner

Rule 88D is not just a regulatory clause; it is a Real-Time Digital Compliance Engine. Introduced to eliminate manual scrutiny, it acts as an automated gatekeeper between your GSTR-2B (Input) and GSTR-3B (Claim). By integrating with the Invoice Management System (IMS), it ensures that not a single rupee of ITC is claimed beyond what the system officially recognizes. If the variance exceeds a pre-set tolerance, the system bypasses human intervention and issues a demand notice instantly.

Rule 88D Compliance Analysis

Caption: Source: ClearTax Analysis on Rule 88D & DRC-01C Guidelines

Portal Alert: System-driven interest under Section 50 is now live. Don’t let the algorithm penalize you for minor delays. Verify the official logic here: GSTR-3B Interest Advisory.

Rule 88D: The Rise of Algorithm-Based Tax Governance

Simply put, Rule 88D acts as an Auto-Pilot Notice Generator. Previously, notices were issued by an officer; now, they are generated by the portal’s algorithm. This rule is triggered whenever a discrepancy is detected between your system-generated GSTR-2B and your filed GSTR-3B. If this discrepancy exceeds the prescribed threshold, the portal—without seeking prior approval from anyone—directly issues a DRC-01C notice.

2. Rule 88D: Defining the Compliance Tolerance & Danger Zones

The Executioner (Rule 88D) triggers the moment you cross these two lines:

- The 10% Variance: If your ITC claim in 3B is more than 10% higher than what is reflected in your GSTR-2B.

- The ₹50,000 Cap: If the absolute difference between 2B and 3B exceeds ₹50,000.

Pro-Tip: In 2026, even if you are off by 10.1%, the system won’t wait. The IMS locks your data, making Rule 88D the ultimate Verification Shield for the GST Department.

3. The DRC-01C Mechanism: Seven Days to Survive

Once Rule 88D flags your account, the process is lightning fast:

- Part A (The Attack): You receive an automated DRC-01C Part A on your portal and registered email.

- The 7-Day Clock: You have exactly 7 days to either:

- Pay the tax (with interest) using DRC-03.

- Explain the reason for the mismatch in Part B.

- The Penalty (GSTR-1 Blocking): If you ignore this for 7 days, the system will Block your GSTR-1/IFF for the next month under Rule 59(6). Your business comes to a standstill because you won’t be able to pass on ITC to your customers.

Future-Proofing: Rules like IMS weren’t built overnight. They are part of a massive algorithm-based roadmap. Explore the vision behind these changes: GST Council Strategy Archives.

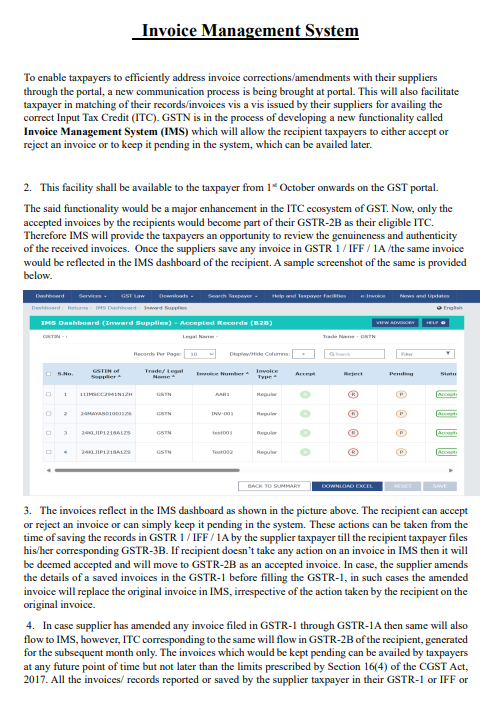

4. Why 2026 is Different? (The IMS Factor)

Earlier, 2B was static. Now, with IMS (Invoice Management System):

- Active Selection: You Accept, Reject, or Keep Pending invoices.

- Direct Link: Rule 88D now uses the data YOU finalized in the IMS.

- No Excuses: You can no longer say I didn’t see that invoice. Since you interacted with it in the IMS, the system assumes your GSTR-2B is 100% accurate.

IMS Dashboard Actions – Accept Reject Pending

Caption: Source: GSTN Official IMS User Manual Preview

Ensure your suppliers follow the 30-day IRN reporting window. An outdated e-invoice is an ‘Invalid Document’ in 2026, triggering an immediate ITC blockage.

Rule 88D Compliance Cheat Sheet: At a Glance

| Feature | Impact under Rule 88D |

| Trigger Point | >10% or >₹50,000 Mismatch |

| Notice Form | DRC-01C (Part A) |

| Deadline | 7 Days (Strict) |

| Consequence of Delay | GSTR-1/IFF Blocking & Recovery |

| Best Defense | Real-time IMS Reconciliation |

The DRC-01C Threshold Audit

Before filing, every professional must run the Rule 88D Mismatch Tolerance Formula to check if they are entering the Red Zone:

Rule 88D: The ‘Safe Zone’ Limit

- The Trigger: If your claimed ITC exceeds this limit, the system issues Form DRC-01C.

- The Deadline: You have exactly 7 calendar days to respond.

- The Penalty: Failure to respond results in an automatic block of your GSTR-1 under Rule 59(6).

2. The IMS Action Paradox: Why ‘Deemed Acceptance’ is Financial Suicide

Smart professionals often ask: Should I Accept, Reject, or Keep it Pending ? Every choice has a hidden consequence. If you take no action, the system assumes Deemed Acceptance.

Many professionals fall into the trap of ‘Deemed Acceptance’ by not interacting with the IMS dashboard. In a professional audit, ‘inaction’ is seen as ‘acceptance of liability.’ We recommend a weekly review of the IMS to ensure that only verified and physically received goods/services are ‘Accepted,’ while doubtful entries are moved to ‘Pending’ to avoid Rule 37A interest hits.

Don’t just focus on Invoices; track Credit Notes in IMS too. Rejecting a valid Credit Note creates an artificial liability for your supplier, leading to reconciliation ‘deadlocks’ and potential scrutiny.

The Risk-Weightage Strategy

Instead of guessing, use the IMS Risk-Weightage Ratio to decide which invoices require manual intervention:

Beyond basic matching, we use a custom Risk-Weightage Ratio to identify high-risk vendors. This helps in deciding whether to ‘Accept’ an invoice immediately or wait for further verification, keeping your compliance rating intact.

IMS: Risk-Weightage Calculation

Strategic Insight: If the result exceeds 15%, it signals high exposure. In 2026, the GSTN’s internal AI uses this exact symmetry to flag “Circular Trading” risks. Manual IMS ‘Acceptance’ is highly recommended for these cases.

- Expert Advice: If the Risk Factor is > 15%, never leave it for ‘Deemed Acceptance’. Manually verify and ‘Accept’ to signal to the AI Grid that your compliance is active, not passive. Passive recipients are often flagged for manual scrutiny under Section 61.

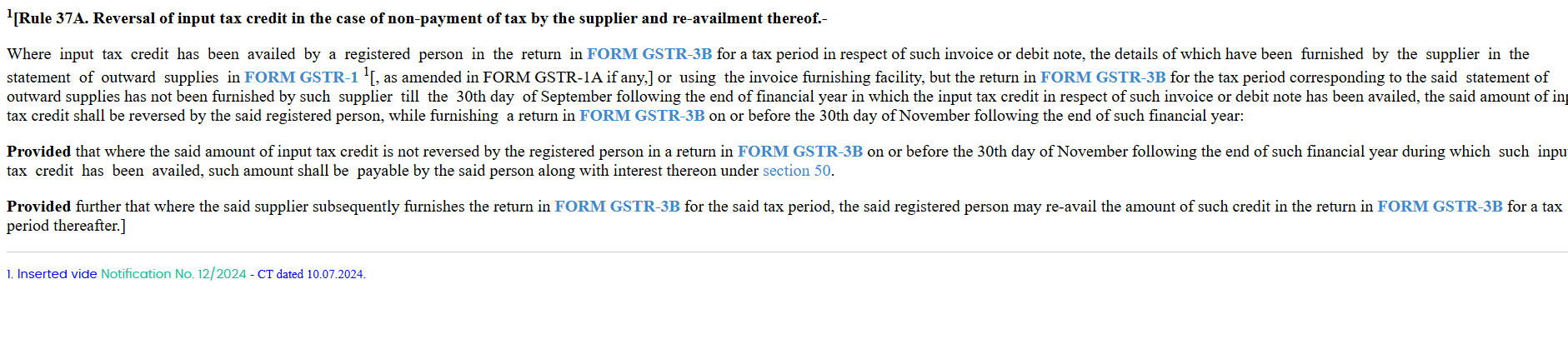

3. Case Study: The Pending Safety Valve vs. Rule 37A

When goods are in transit or quality checks are ongoing, the Pending status is your best friend. It prevents the ITC from flowing into your GSTR-2B, thus saving you from future reversals.

GST Rule 37A Compliance

Caption: Source: Taxmann/ClearTax Legal Database – Rule 37A Provisions

Don’t Get Flagged: A supplier’s mistake shouldn’t become your liability. We’ve decoded a specialized math to shield you from departmental heat. Read How to Avoid ASMT-10 Notices and learn how to defend your ITC claims during real-time audits.

Rule 37A: The Interest Exposure Audit

Keeping an invoice ‘Pending’ protects you from the Rule 37A Reversal Liability:

Rule 37A: Potential Reversal Liability

Critical Alert: In 2026, the GSTN portal identifies these delays in real-time. Use this formula to create a ‘Provision for Contingent Liability’ in your monthly financial audits.

By keeping doubtful invoices in ‘Pending’ status, you avoid claiming ITC that you might have to return later with 18% interest if the supplier defaults on their GSTR-3B.

Pro-Insight: Managing cash flow in 2026 is like walking on a tightrope. If you want to master the art of protecting your liquidity, check out our guide on Rule 86B & 37A Strategy. It’s the ultimate roadmap to stop the 1% cash trap from hitting your working capital.

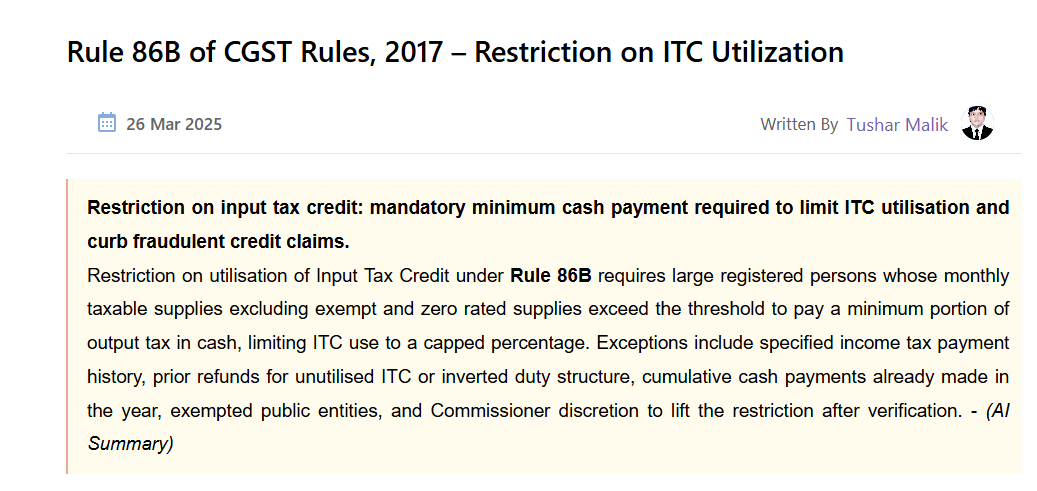

4. The Deep Link: Rule 88D and the 1% Cash Trap (Rule 86B)

This is the most critical intersection. Many CAs treat Rule 86B and Rule 88D as separate silos. They are not. If you ‘Reject’ too many invoices in IMS to avoid a Rule 88D notice, you might inadvertently lower your ITC balance below your liability.

Rule 86B Compliance Summary

Caption: Source: Tax Compliance Database – Understanding Rule 86B Cash Mandate.

The Liquidity Optimization Formula

To protect your working capital, use the Optimal Acceptance Value:

Rule 86B: Optimal Acceptance Value

Strategic Insight: Is formula ka use karke aap IMS mein sirf utne hi invoices ‘Accept’ karein jitne ki zaroorat hai. Isse aapka cash flow optimize rahega aur Rule 86B ke tehat mandatory 1% cash payment ki liquidity bani rahegi.

The Result: If you don’t accept enough valid invoices to meet this value, you won’t just be paying the mandatory 1% Cash; you will be forced to pay 100% Cash for the shortfall.

Strategic Solution: Use the GSTR-1A window. If there is a mismatch, force the supplier to amend it before your 2B is finalized. This keeps the ITC valid, avoids Rule 88D, and keeps your cash outflow at the bare minimum of 1%.

The 7-Day Race: Once a DRC-01C hits, the clock never stops. Sync your internal audits with this real-time deadline engine: May 2026 Compliance Tracker.

5. Step-by-Step Response Strategy for DRC-01C (Part B)

If hit with a notice, use this legal template in your response:

- Reference Section 155: Remind the officer that the burden of proof is discharged via the IMS Acceptance Log.

- Rule 37A Compliance: Explicitly state that ITC is only claimed for suppliers who have filed GSTR-3B.

- The Reconciliation Formula: Attach a sheet showing:

Final Claimed ITC Calculation

Strategic Insight: Ye calculation 2026 ke new IMS dashboard ke hisaab se crucial hai. Rule 42/43 ka reversal aapki net tax liability ko affect karta hai, isliye isse as-is formula ke roop mein maintain karein.

6.The ‘Grey’ Areas: Strategic Nuances of 2026 Compliance

- Financial Year End: Invoices left as Pending past the Section 16(4) deadline (Nov 30th) will lead to permanent ITC loss. Conduct a Mega-IMS Audit every September.

- Partial Acceptance: IMS is binary. For partial disputes, Reject the full invoice, get a Credit Note (Section 34), and a new invoice. Do not manually adjust in 3B, or you will trigger the 88D AI immediately.

GST ITC Claim Deadline Section 16(4)

Caption: Source: ClearTax Guide on Section 16(4) ITC Deadlines

The Final Shield: The legal landscape is shifting. To ensure you don’t lose your hard-earned ITC forever, we’ve built a Section 16(2)(c) Survival Guide. It’s a must-read for every professional conducting a Mega-Audit before the November deadline hits.

Conclusion: From Accountant to Strategist

Mastering GST in 2026 is about moving from a reactive accountant mindset to a proactive strategist. By syncing your internal audits with these four formulas and maintaining a strict 7-day watch on DRC-01C notices, you don’t just file taxes—you protect your business’s credit standing and liquidity.

Compliance Checklist

2026 Professional Strategy

Mega Audit

Sept mein Sec 16(4) check karein.

Risk Scan

Vendors ka monthly risk check.

7-Day Watch

DRC notice ka 7 din mein reply.

2B Sync

Safe Limit se 2B match karein.

• PRECISION COMPLIANCE •

Frequently Asked Questions

Q-1 Can I ignore IMS if my reconciliation is 100% matching?

No. Deemed Acceptance still happens. Manually verify to maintain your GST Compliance Rating (Section 149).

Q-2 Does Rule 88D apply to IGST on Imports ?

No, that flows from ICEGATE. However, any manual entry of import ITC will trigger a mismatch notice.

Q-3 What if the supplier files GSTR-1 but not 3B ?

IMS will show the invoice, but Rule 37A will eventually force a reversal. Acceptance in IMS is not a permanent guarantee of ITC.

Disclaimer: This professional guide is based on the GST framework as of May 2026. Tax laws are subject to frequent changes. Always consult with a qualified professional before taking high-value financial actions.

Anurag Panchal

Founder of AllRoundUpdate.com & ServiceMoney.in.

Specialist in Indian Tax Compliance and GST Rules (86B & 37A). Follow @Educationanurag for latest updates.