By Anurag Panchal | Founder, ServiceMoney.in

The landscape of Input Tax Credit (ITC) has shifted from compliance-based to litigation-based. For a tax professional in 2026, the challenge is no longer just matching GSTR-2B; it is defending the very right to credit when the supplier defaults. While Rule 37A provides the procedure for reversal, the real battlefield lies in Section 16(2)(c)—the Innocent Buyer’s Trap.

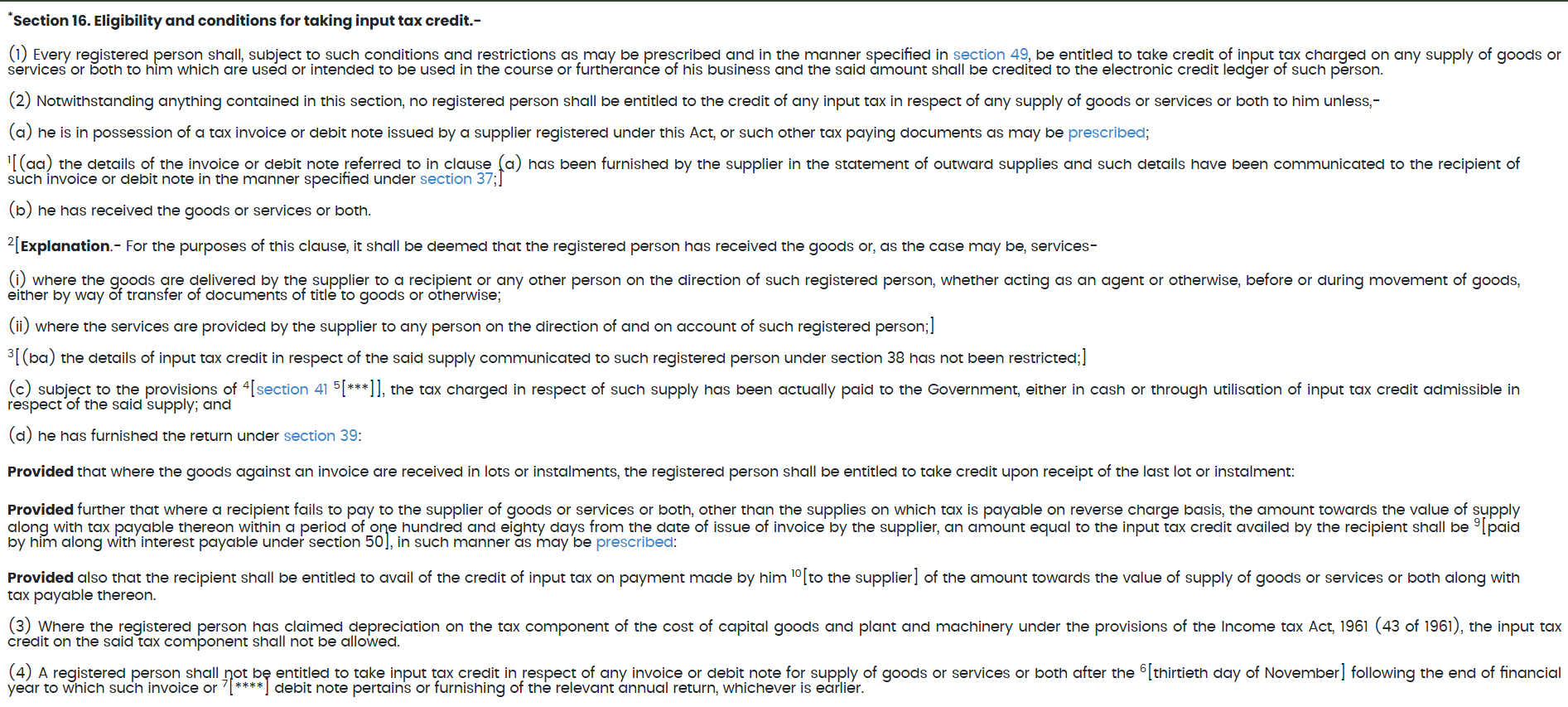

Eligibility Conditions for Availing ITC under Section 16

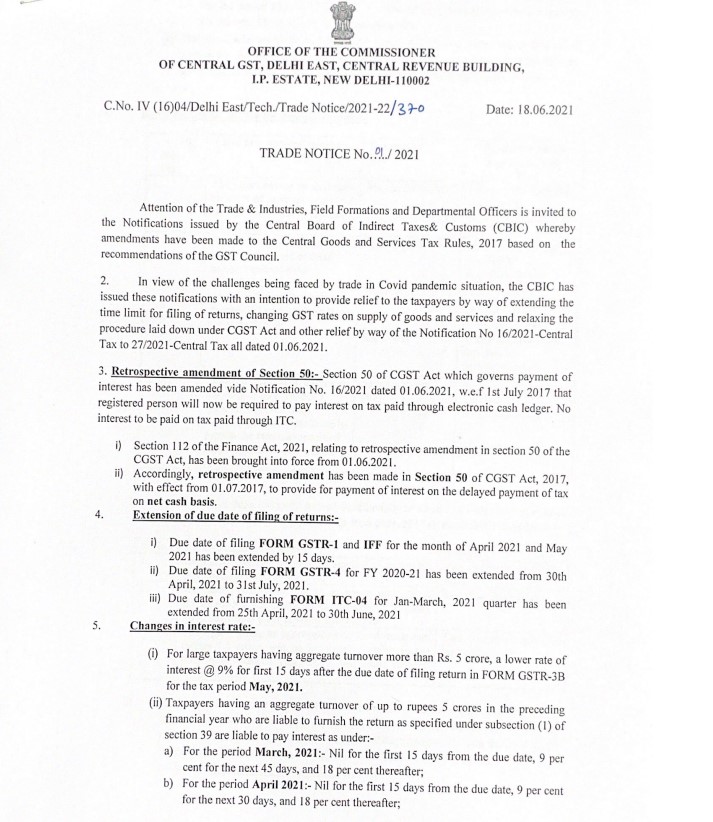

Caption: Source: Official CGST Act Guidelines on ITC Eligibility Conditions.

If you are a CA or an Accountant defending a client against an ITC demand notice, simply quoting the law isn’t enough. You need a Strategic Defense Matrix backed by practical audit formulas and a deep understanding of the Grey Areas that automated scrutiny often overlooks.

1. The 2026 Pain Point: The Innocent Buyer’s Trap

Lately, I’ve seen a massive surge in automated notices where the buyer is being treated like a criminal for the supplier’s default. It’s a frustrating ‘black hole’ in the law.

Based on my recent discussions with fellow practitioners, the biggest headache isn’t the law itself, but the lack of a structured defense when the SCN (Show Cause Notice) hits your desk.

The Obstacle: A buyer does everything right—pays the invoice via bank, receives goods, and files returns—but the supplier either vanishes or their GSTIN is cancelled retrospectively.

The Statutory Paradox : Why should the buyer act as the Department’s recovery agent? Is it legally sound to punish the recipient for the supplier’s tax heist ?

Legality Check: Is it really your job to police vendors? Before drafting your reply, verify the exact wording of the [Official Section 16 CGST Text]. Knowing the statutory boundaries is your first step to a winning defense.

In 2026, the GST portal is smarter, but it is also more rigid. Automated notices (ASMT-10) are issued the moment a mismatch is detected, leaving professionals with very little time to gather Substantive Evidence.

2. 5 High-Level Audit Formulas for Professional Defense

To move beyond theory, you must use these 5 formulas to assess risk and draft replies that the Department cannot easily dismiss. These are your ServiceMoney Formulas for 2026.

Formula 1: The Rule 37A Reversal Trigger

Use this to identify exactly which credits are at risk before the November 30th deadline.

Rule 37A: The ITC Exposure Math

Professional Tip: If this calculation shows a positive gap after 30th September, start the reversal process immediately to avoid Section 50 interest penalties. In 2026, automation is your best defense.

- Professional Insight: If the supplier has filed GSTR-1 but not 3B, the system now auto-triggers a mismatch. If not reversed by 30th November, interest applies under Section 50.

Don’t Lose Your Credit: Reversing ITC under Rule 37A isn’t the end of the road. You can bring that money back into your books! Follow our [Step-by-Step ITC Re-claim Guide] to recover your taxes safely without getting an ASMT-10.

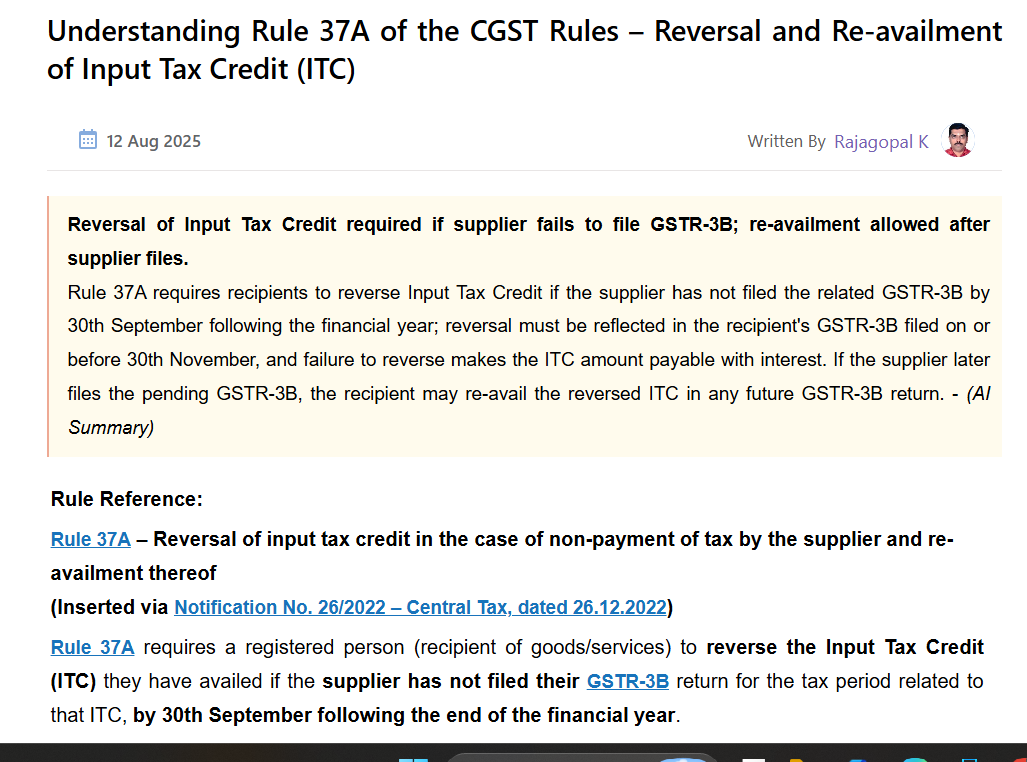

Rule 37A ITC Reversal and Re-availment Procedure

Caption: Source: TaxTMI – Detailed Analysis of Rule 37A and ITC Reversal Timelines.

Formula 2: The Minimum Interest Liability (2026 Revised)

As of January 2026, the GST portal auto-calculates interest on the Net Tax Liability only. Use this to challenge over-calculated interest demands.

Section 50: Net Cash Liability Impact

CA Insight: Proviso to Section 50(1) clarifies that interest is only payable on the portion of tax paid in cash. This is a massive relief for taxpayers who have enough balance in their Credit Ledger.

- Net Cash Shortfall = Total Liability – Minimum Cash Balance in ECL during the delay period.

Stop Overpaying Interest: Manual calculations often lead to higher demands. To protect your cash flow, learn how to use the [Section 50(3) Interest Shield] to challenge inflated notices and save your ITC from automated AI traps.

Section 50 Interest Calculation on Net Cash Basis

Caption: Source: Retrospective Amendment of Section 50, CGST Act via Official Trade Notice.

Formula 3: The Common Credit Reversal (Rule 42)

For clients with both taxable and exempt supplies, the nuance lies in the D1 and D2 variables.

ITC Reversal: Mixed Supply Logic

CA Strategy: Accurate calculation of ‘E’ and ‘F’ is crucial under Rule 42. Any error in identifying exempt turnover leads to incorrect reversal, inviting scrutiny and interest under Section 50.

Formula 4: The Vendor Risk Score (Due Diligence)

A mathematical way to justify Good Faith to the auditor.

Audit Defense: The Vendor Risk Score

ServiceMoney Strategy: Use this formula during audits to prove you are an ‘Innocent Buyer’. It demonstrates that you have exercised standard vigilance in selecting compliant business partners.

- Target: >98%. A high score supports the argument that any single supplier default is an exception, not a systemic failure.

Formula 5: The 180-Day Payment Ageing Audit

Ineligible ITC: The 180-Day Deadline

Professional Insight: According to Section 16(2), if you fail to make the payment within 180 days, the ITC must be reversed. However, once the payment is made, you can ‘re-claim’ this credit without any time limit.

Most junior accountants miss a tiny critical detail : the 180-day clock starts from the Invoice Date, not the date you received the goods. I’ve seen notices where the only mistake was a 2-day delay in payment. Ensure your ageing report is set to ‘Invoice Date’ to stay 100% safe.

- The Detail: Ensure the Payment includes the GST portion. Partial payment leads to proportionate reversal—a minute detail often missed.

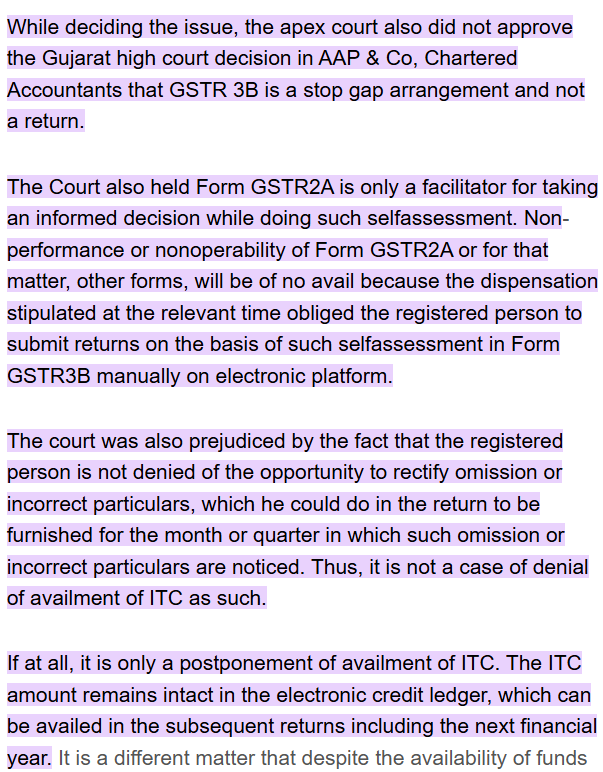

3. The Doctrine of Impossibility (The Professional’s Armor)

Think of it this way: the Government has all the data of the supplier’s bank accounts and properties. You, as a buyer, only have an invoice. How can the law expect you to do what the entire GST Department couldn’t?

This isn’t just a legal theory; it’s common sense, and you must use this to challenge the ‘Arise India’ logic in your replies.

- The Argument: A buyer cannot be expected to perform the impossible task of policing the supplier’s private treasury.

Judicial Precedent on GSTR-3B and ITC Rights

Caption: Source: ITATOnline – Supreme Court Ruling in Union of India vs. Bharti Airtel on GSTR-3B and ITC Eligibility.

- Deep Insight: You must argue that once the buyer has paid the tax to the supplier, the supplier holds that money as a Trustee for the Government. If the Trustee commits fraud, the Government should sue the Trustee, not the Buyer.

Your Legal Armor: Courts are now siding with honest taxpayers. Reference the latest [Landmark SC Ruling on ITC Rights] to prove that you cannot be forced to perform the ‘impossible’ task of tracking a supplier’s tax deposit.

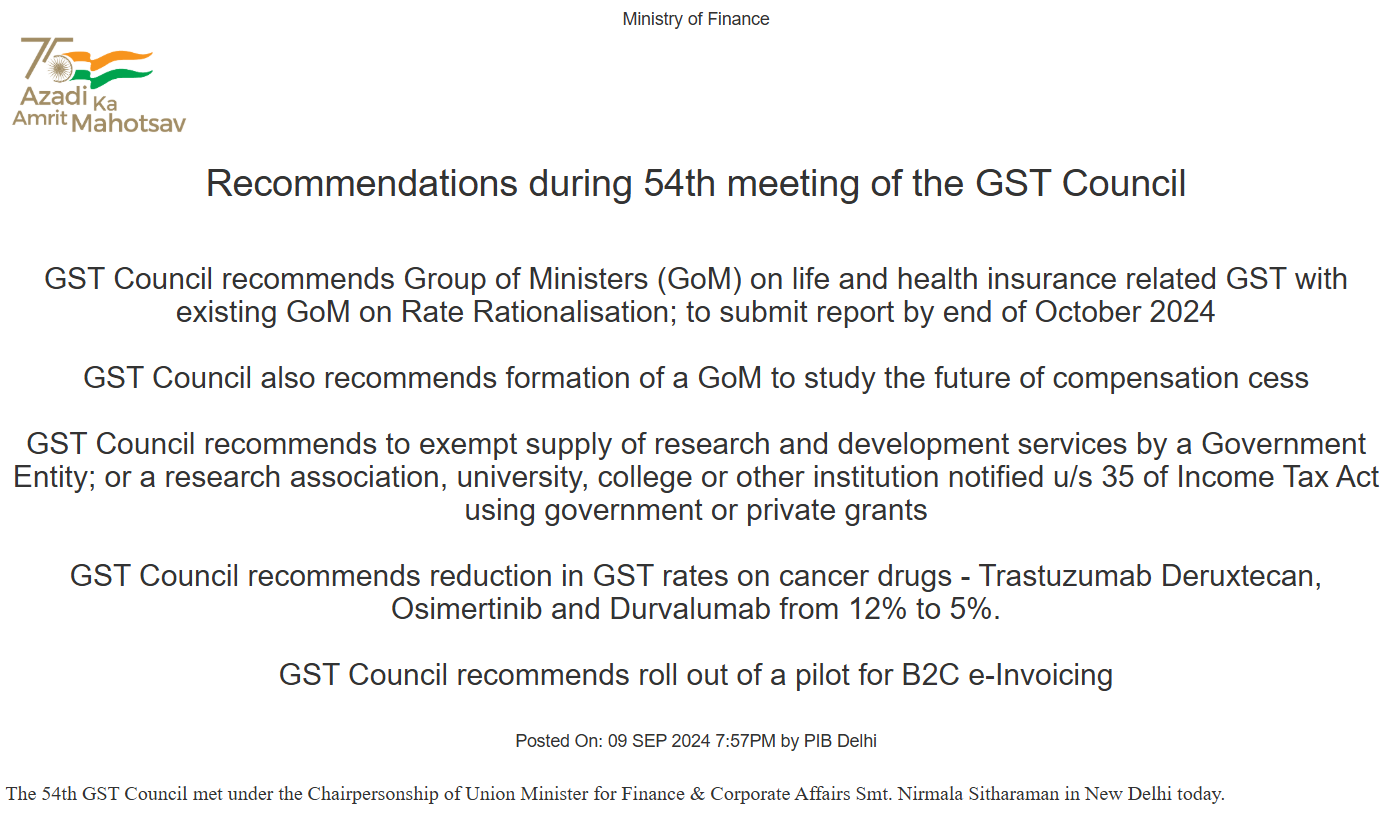

4. Minute Technical Nuances: Solving the Unsolved Doubts

PIB Press Release: Recommendations of the 54th GST Council Meeting

Caption: Source: Press Information Bureau (PIB) – Official Press Release of the 54th GST Council Meeting.

A. The Ghost Supplier (Retrospective Cancellation)

What happens if the GSTIN was active in 2024 but cancelled retrospectively in 2026 ?

- Solution: Your defense must include a Compliance Snapshot. Use digital tools to archive the supplier’s Green Status at the time of the transaction.

Procedural Shield: If your vendor’s GSTIN was cancelled retrospectively, don’t panic. Check [GST Notification No. 12/2024] for the official SOP on re-availment to ensure you aren’t missing out on valid credits.

- A retrospective act of the department cannot invalidate a vested right of the buyer.

B. Partial Payment & Quality Holds

If a client holds 5% payment due to a quality dispute:

- The Risk: Auditors will demand 100% reversal.

- The Solution: Use the Proportionate Reversal logic. Maintain a Quality Dispute Register to show the hold is legitimate and not a failure to pay within 180 days.

C. The Toll Plaza Evidence (Proving Movement)

In Fake Invoice allegations, GSTR-2B is useless.

- Strategic Insight: To save the ITC, you need External Proof. Link your E-way bill with FASTag data and Weighbridge slips. In 2026, this Physical Proof Chain is the only way to beat a Section 74 (Fraud) notice.

5. The Double-Edged Sword: Errors by Buyer vs. Seller

GST litigation isn’t always the result of a buyer’s mistake; often, a minor oversight by the seller can jeopardize the buyer’s credit. For a seamless compliance ecosystem in 2026, both parties must understand their specific pitfalls and how to rectify them.

| Aspect | Seller’s Default (The Trigger) | Buyer’s Oversight (The Risk) |

| Reporting Error | Entering an incorrect GSTIN in GSTR-1. | Claiming full ITC without verifying GSTR-2B. |

| Filing Gap | Filing GSTR-1 but failing to file GSTR-3B (triggering Rule 88C). | Failure to pay the seller within 180 days (triggering Rule 37 reversal). |

| Classification | Erroneously reporting a B2B invoice as B2C. | Mixing Ineligible ITC (Section 17(5)) into the common credit pool. |

Year-End Safety Net: Even a small mapping error in your annual returns can trigger a fraud notice. Make your filings bulletproof by using our [GSTR-9 & Rule 42/43 Audit Guide] to sync your data perfectly with the 2026 IMS portal.

The Professional Solution

For Sellers: Prioritize Accuracy Over Adjustments

If you discover a reporting error, utilize the GSTR-1 Amendment (Table 9A/9C) in the subsequent month immediately. Prioritize these amendments over issuing Credit Notes, as amendments directly update the buyer’s GSTR-2B, ensuring their credit remains secure.

For Buyers: Proactive Reconciliation

Prepare a Vendor Reconciliation Statement every quarter. If a vendor consistently defaults, instead of simply withholding payment, require them to sign a GST Compliance Undertaking. This legal framework ensures that the responsibility for any future tax loss due to their non-compliance rests with the supplier.

6. Strategic Self-Audit Checklist for Professionals

Key Highlights from the 55th GST Council Meeting

Caption: Source: Razorpay Learn – Key Takeaways and Highlights from the 55th GST Council Meeting.

| Obstacle (The Problem) | ServiceMoney Solution (The Defense) |

| GSTR-3B vs 2B Mismatch (QRMP) | Maintain a Holding Ledger for valid but uncommunicated ITC. |

| Notice for Ineligible ITC (17(5)) | Segregate Blocked Credit at the time of entry to avoid interest. |

| Supplier Non-Payment (Rule 37A) | Set up automated Payment-Block for vendors whose 3B is pending for 2+ months. |

7. Drafting the Reply: A Sample Snippet for CAs

The recipient has fulfilled all conditions under Section 16(2)(a), (b), and (d). Regarding Section 16(2)(c), the tax has been paid to the supplier as part of the invoice value via banking channels (Transaction Ref: XXXXX). The recipient possesses no statutory power to compel the supplier to file GSTR-3B. Denying credit here violates the principle of ‘Doctrine of Impossibility’ as upheld in [Cite Latest 2025-26 Case Law].

Conclusion: From Data Entry to Tax Strategy

In 2026, compliance is your shield. By using the 5 Formulas and focusing on the Audit Trail, you move from a Return Filer to a Financial Defender.

- If the fault is the Supplier’s: Fight with the Doctrine of Impossibility and Case Laws.

- If the fault is the Buyer’s: Fix it immediately with DRC-03 to minimize interest and penalty.

ServiceMoney.in is committed to simplifying these complexities for the elite accounting community. Stay curious, stay compliant.

FAQ (For Smart Professionals)

Q1: Can we reclaim ITC after the 16(4) deadline ?

Yes, for Rule 37A reversals, the 16(4) deadline does not apply to re-claims. You can reclaim it once the supplier pays, even after 2 years.

Q2: Does Net Tax Liability interest apply to old notices ?

Generally, yes. Retrospective amendments usually allow interest calculation on the cash portion only, but check the specific notification year.

Q3: How to handle a supplier who has filed GSTR-1 but not 3B ?

Issue a formal Legal Communication to the vendor immediately. Under Rule 37A, this is a ticking time bomb for your November reversal.

Disclaimer

This blog is for educational purposes only. 2026 GST rules are dynamic. Always consult the latest notifications on the CBIC portal before filing legal responses.

Meet the Expert

Anurag Panchal is a seasoned Digital Marketer and Tech Strategist, widely recognized as the Founder of ServiceMoney.in and AllRoundUpdate.com.

Specializing in simplifying emerging technologies and financial compliance for an Indian audience, Anurag has authored over 135+ technical guides to help more than 10,000+ readers navigate the complexities of GST litigation, Tally Prime automation, and technical SEO.

Through his professional platforms, he focuses on transforming dry statutory laws into formula-driven defense strategies, empowering tax professionals to protect their businesses from automated scrutiny and the ‘Innocent Buyer’s Trap’.

Connect with his expert masterclasses:

- YouTube: @Educationanurag.

- Professional Portals: ServiceMoney.in | AllRoundUpdate.com.