Why Rule 37A Recovery is the Biggest Goal for CAs in 2026

Managing GST compliance through Rule 37A Re-claims (ECRS Math) is not limited to just filing returns; It’s about protecting your client’s hard-earned cash. With the new Rule 37A updates, many professionals feel stuck after reversing ITC. But did you know this reversed credit is actually a ‘hidden asset’ waiting to be unlocked? Let’s look at how you can recover this legally and mathematically.

As a tax professional, you’ve already handled the “Defense” side of Rule 37A—reversing ITC by November 30th to avoid the Section 50(3) interest trap. But for a smart professional, the story doesn’t end at reversal.

The real challenge is the Recovery Phase. In 2026, with the Invoice Management System (IMS) and the Electronic Credit Reversal and Re-claimed Statement (ECRS) ledger, manual tracking is a liability. If you don’t have a mathematical audit trail, you are inviting an ASMT-10 notice for “Excess ITC Claim.

Important: Recovery Before a reversal, it is essential that the base is correct. Learn the Rule 37A Defense Strategy to protect your working capital from high interest penalties and IMS-based AI traps.

In my years of managing service-oriented websites, I’ve seen many businesses lose lakhs simply because they didn’t track their reversals.

1. The Deep Pain Point: The “Reconciliation Black Hole”

“When you deal with thousands of invoices, losing track of even one delinquent supplier can lead to massive cash leakage. Think of reversed ITC as a ‘Floating Asset.’ If your team changes or your Excel sheets crash, that money is gone forever. To avoid this, we need a system that doesn’t rely on memory, but on a clear audit trail.

The Risk of “Silent Leakage”: If Supplier A files in 2027 and your accountant has changed or your Excel sheet is lost, that ITC is gone. This is Cash Flow Leakage. To solve this, a professional must move beyond memory and use Forensic Math.

Think of it as a digital audit trail. In 2026, the GST portal’s AI doesn’t just look at numbers; it looks at the history of every single Invoice Reference Number (IRN).

The Recovery Math (Formula 1)

To calculate your true recovery potential without over-claiming, use this filtered approach:

ITC Recovery Audit Formula

2. Advanced Scenario Analysis: The “Partial Filing” Trap

Smart audiences know that suppliers rarely file everything at once. How do you handle a supplier who files for 2 out of 5 pending invoices?

Case Study: The Proportional Recovery

- Original Reversal (Nov 2025): ₹1,00,000 (across 5 Invoices).

- Current Status (May 2026): Supplier files GSTR-3B for only 2 invoices (Tax Value: ₹40,000).

- The Problem: Should you re-claim the full ₹1 Lakh? No.

Imagine a practical situation: You reversed ₹1 Lakh last year. Now, your supplier has only paid for 2 out of 5 invoices. Many accountants make the mistake of reclaiming the full amount or nothing at all. Both steps are dangerous. The 2026 IMS system expects you to be precise—claim only what is visible in your GSTR-2B to stay in the ‘Safe Zone’.

Don’t let your client pressure you into claiming the full ₹1 Lakh. If the GSTR-2B only shows ₹40,000, that is your hard limit. Anything more is a direct ticket to an automated GST notice.

Rule 37A(4) Legal Provision

Caption: Figure 1: Statutory Provision of Rule 37A(4) confirming that ITC can be re-availed once the supplier pays tax. (Source: cbic.gov.in)

The Proportional Recovery Formula (Formula 2)

Eligible Re-availment Formula

Claiming even ₹1 more than the proportional amount triggers the IMS AI validation, as the system tracks the specific IRN (Invoice Reference Number) linked to the original reversal.

3. Step-by-Step SOP: The 2026 “Dual-Reporting” Framework

In 2026, the GSTN portal is no longer a passive ledger; it is an Active Validator. Your reporting in GSTR-3B must be surgically precise.

Pro-Audit Tip: Surgical precision in your GSTR-3B is the only way to stay off the departmental radar. Explore how to Eliminate ASMT-10 Risks using advanced formula strategies tailored for the 2026 framework.

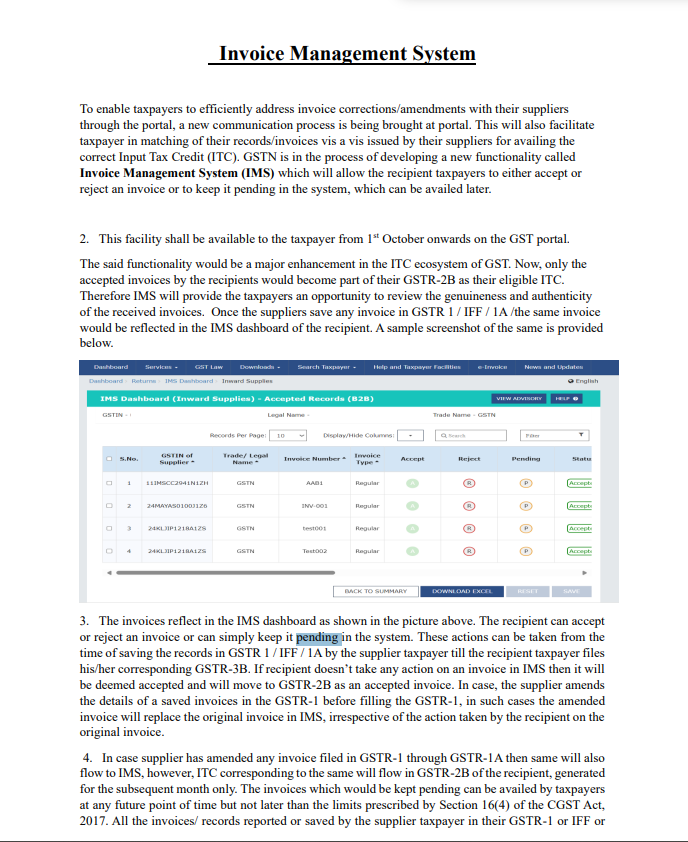

Step A: The IMS Validation (Pre-filing)

Before touching GSTR-3B, you must log into the Invoice Management System (IMS). * Action: Identify invoices marked as “Pending” due to Rule 37A.

IMS Pending Invoices Interface

Caption: Figure 3: A view of the IMS Dashboard where professionals can track ‘Pending’ invoices for Rule 37A compliance. (Source: gst.gov.in)

- Status Check: Ensure the “Tax Paid” flag is green. In 2026, the portal introduces a “Rule 37A Eligibility Flag” in the GSTR-2B. If this flag is ‘No’, your math doesn’t matter—the portal will block the claim.

Step B: The 3B Mapping (The Dual-Entry Method)

To satisfy the AI-monitoring system, you must “Balance the Scale”:

- Table 4(A)(5) [All Other ITC]: This is the Inflow.

- Table 4(D)(1) [ITC Re-claimed]: This is the Disclosure.

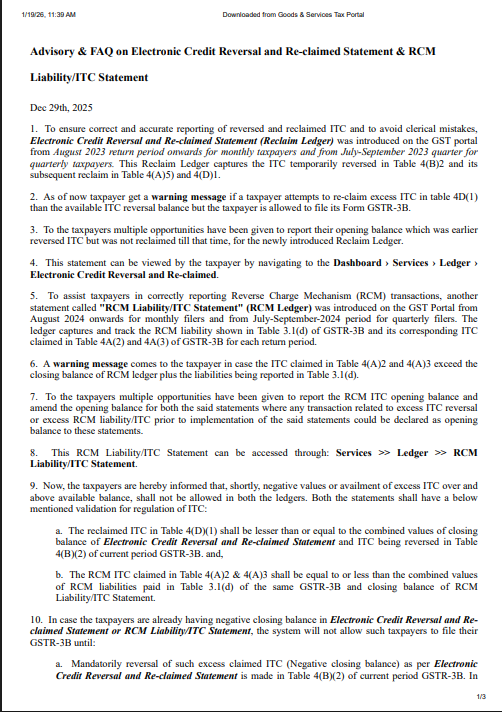

ECRS Ledger Validation Rules 2026

Caption: Figure 2: Official GSTN Advisory stating that negative ECRS balance will now result in a ‘Hard-Block’ during GSTR-3B filing. (Source: mahagst.gov.in)

The ECRS Validation Logic (Formula 3)

Before clicking ‘File’, the GSTN back-end runs this check. If this results in a negative value, you face a Hard-Block.

ECRS Closing Balance Formula

Strategically, your Table 4D1 should never exceed the sum of Opening Balance and Current Reversals.

4. Strategic Advantage: The “Never-Ending” Deadline

The best part about Rule 37A(4) is that it has no expiry date. Unlike Section 16(4) which kills your right to claim ITC after November, this rule acts as a ‘Permanent Tax Insurance.’ You can trigger this recovery whenever your client faces a high cash liability, even years later.

Verification Tip: Don’t just take my word for it. Check the latest GST Law Manual to see why Rule 37A recovery is a statutory exception to the standard time limits.

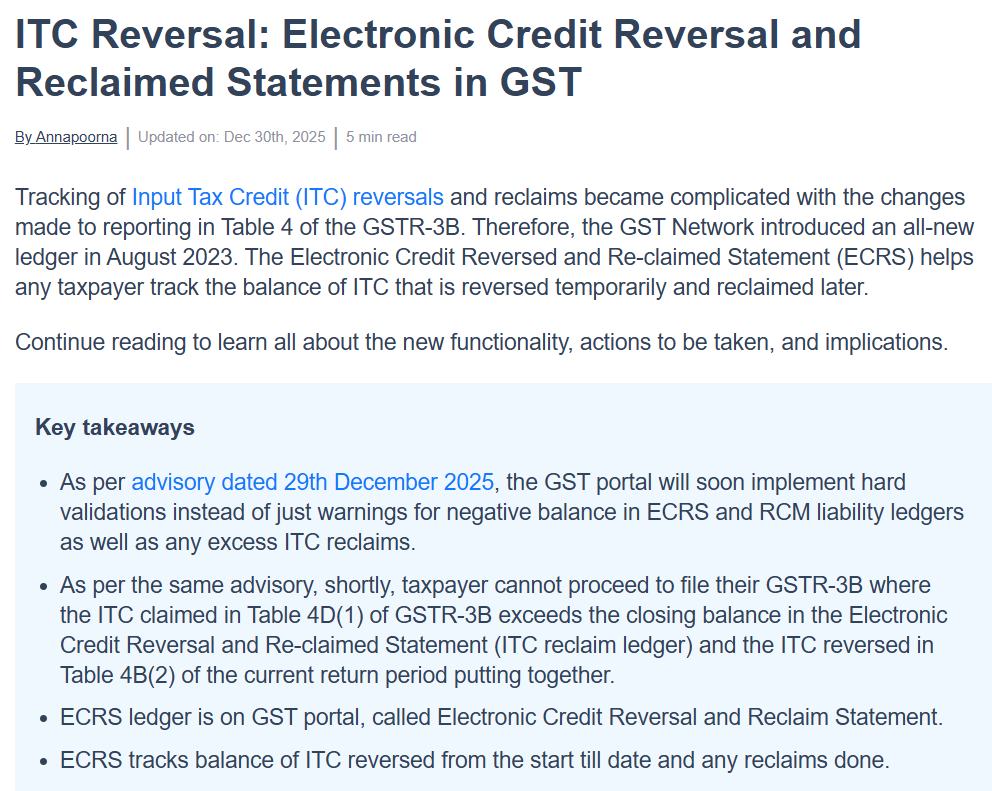

ECRS Ledger Functionality Summary

Caption: Figure 4: Summary of ECRS functionality ensuring an audit trail for re-claimed ITC. (Source: GST Technical Guides)

The Time-Value Strategy:

Since there is no time limit, this reversed ITC acts as a “Tax Insurance Policy.” If your client faces a high cash liability 3 years later, you can “trigger” these recoveries to offset the cash payment.

The Client Value Metric (Formula 4)

Show your client the ROI of your tracking service:

Total Value Unlocked Formula

5. The “Mirror Ledger” & Accounting Forensics

A CA’s best friend is the Audit Trail. In your ERP (Tally Prime / SAP), do not mix Rule 37A reversals with regular 4(B)(2) reversals.

Recommended Ledger Hierarchy:

- Duties & Taxes

- GST Input Credit

- Rule 37A Suspense (Un-recovered) — Nature: Current Asset

- Electronic Credit Ledger (Available) — Nature: Cash Equivalent

- GST Input Credit

Proper ledger grouping is the secret to a stress-free GST audit. By separating ‘Rule 37A Suspense’ from your regular taxes, you can justify every penny to the department without digging through old files.

🏛️ Government Guide: Don’t get lost in complex jargon. You can verify the official conditions for ITC eligibility directly from the CBIC GST Knowledge Portal. It’s the ultimate source for checking Section 16 rules and the latest Rule 37A statutory amendments.

The Neutrality Formula (Formula 5)

When the GST auditor asks why you are claiming credit from 3 years ago, present this:

Net Interest Liability Formula

Referencing Rule 37A(4) specifically protects you from Section 50(3) demands.

6. Common Pitfalls & “Red Flag” Defense

Even smart professionals make these mistakes:

- The GSTR-1 Fallacy: Supplier filed GSTR-1 but not 3B. Result: Re-claim is illegal.

- The 2B vs. 3B Mismatch: Re-claiming based on a 2A statement instead of the ECRS-linked 2B. Result: IMS Notice.

- Ignoring Circular 170: Failing to report re-claims in Table 4(D)(1). Result: AI Red Flag.

Technical Alert: Misunderstanding portal logic can lead to mismatches. Refer to the GST Council Updates to track recent changes in Rule 37A and reclaim validation rules.

7. Professional Checklist for FY 2026-27

To ensure your firm is “Audit-Ready,” keep a digital folder for every Rule 37A recovery containing:

- [ ] The “Master Reconciliation” Sheet: Mapping original GSTR-3B month of reversal to the current month of recovery.

- [ ] Supplier Communication Log: Proof that you followed up with the delinquent supplier (useful for Section 16(2)(c) defense).

- [ ] ECRS Ledger Snapshot: Showing the balance before and after the re-claim.

Emergency Resource: If the portal flags a mismatch, do not panic. Follow our expert guide on GST ASMT-10 Replies using proven AI-drafting templates and professional response formulas.

8. Conclusion: From Compliance to Tax Strategy

In the era of AI-driven taxation, the role of a CA has shifted. You are no longer a “Tax Filer”; you are a Data Architect. Rule 37A(4) provides a unique opportunity to recover millions in “lost” credit. By implementing the Dual-Entry SOP and the Mirror Ledger Strategy, you convert a compliance burden into a competitive advantage for your clients.

The shift from 2025 to 2026 has turned tax professionals into ‘Data Architects.’ Rule 37A(4) isn’t just a rule; it’s a tool to improve your client’s bottom line. Start your audit today and unlock that frozen capital.

Don’t let the Reconciliation Black Hole swallow your client’s capital. Start auditing your “Suspense ITC” today.

F&Q (Frequently Asked Questions)

Q1: Can I re-claim ITC if the supplier was struck off by the ROC ?

No. If the GSTIN is cancelled retrospectively, the “Tax Paid” condition of Section 16(2)(c) can never be met. Even if you have the invoice, the absence of tax payment to the government makes the recovery legally void. Formula 1 will result in zero.

Q2: Is there a maximum cap on re-availment ?

Yes. You can never re-claim more than what you originally reversed for that specific supplier/invoice combination.

Q3: How does the “Safe Harbor” under 37A(4) affect my Audit Report (3CD) ?

It ensures that you don’t have to report “Undue ITC Claims” or interest liabilities for these specific transactions, provided the ECRS trail is clean.

Disclaimer

This technical guide is based on GST provisions and portal logic as of April 2026. Tax laws are dynamic; professionals must correlate these strategies with the latest CBIC Circulars and Portal functionalities.

Meet the Expert

Author Bio: Anurag Panchal is the Founder of AllRoundUpdate & ServiceMoney and a dedicated Financial Educator. With over 135+ technical guides on YouTube, he has helped 10,000+ readers simplify complex GST compliance, Tally Prime workflows, and Digital Marketing strategies through practical, formula-driven insights. Follow his expert masterclasses on YouTube @Educationanurag.