Rule 37A Reversals & ECRS Ledger of mechanics Regarding lately, I’ve been receiving messages from fellow CAs worried about a specific ‘Red Alert’ in their GST dashboards.

We are seeing a clash between Rule 37A and Section 16(4) that feels like a glitch in the matrix. Having handled several ASMT-10 replies this quarter, I realized that the logic being applied by the portal’s AI isn’t always aligned with the law. This isn’t just about filing; it’s about protecting our clients’ hard-earned capital.

Law Fact-Check: Don’t rely on rumors—verify the actual legislative text. You can access the [Official CBIC Notification] to see how Rule 37A was legally inserted into the GST law by the Ministry of Finance.

If you are managing high-volume ITC, you are standing in a Dead Zone where the law permits a re-claim, but the portal’s algorithm triggers a demand. This is not a mere technical glitch—it is a risk of permanent financial loss.

The Big Pain : When an Asset Becomes a Liability

In accounting, an Expired Asset is a catastrophe. To explain the gravity to a client, we must look at the Net Cash Impact Formula:

Net Cash Impact: The Cost of Denial

If a CA fails to navigate the Dead Zone, the business pays twice: once to the supplier and once to the Government (via lost ITC). This makes the Rule 37A re-claim a high-stakes litigation battle.

Segment 1: The ECRS Ledger – Your Digital Defense

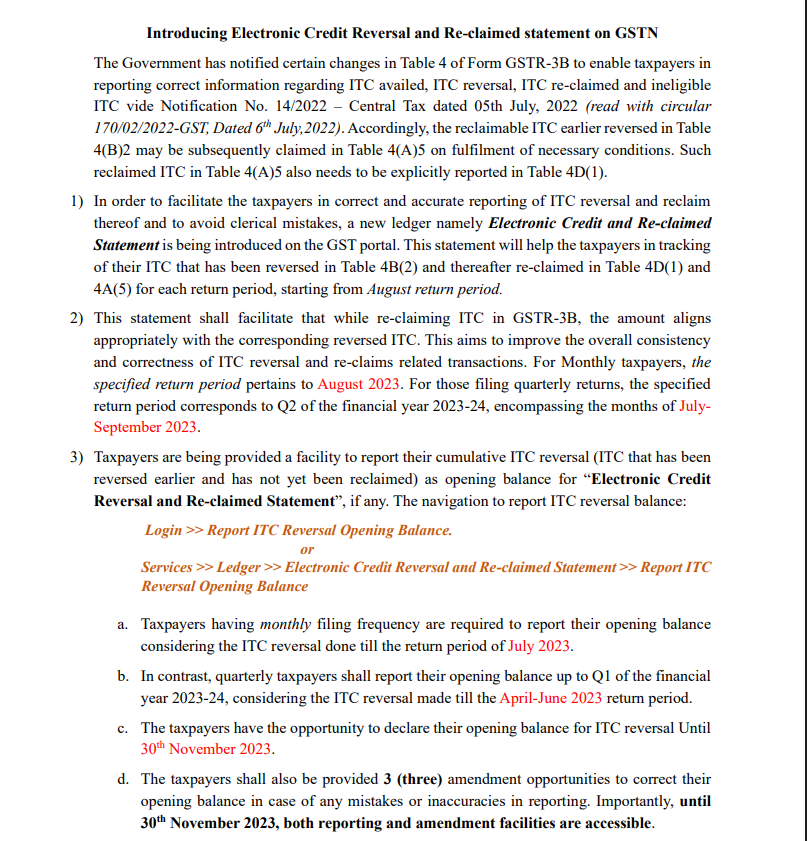

The Electronic Credit Reversal and Re-claimed Statement (ECRS) was introduced to bring transparency, but for many, it has become a source of Technical Mismatches.

GST Rule 37A and Circular 170/02/2022-GST Official Logic

Caption: Source: Official GSTN Advisory on Reversal and Re-claim mechanics.

The Opening Balance

Many professionals ignored the initial ECRS reporting. If your opening balance wasn’t declared correctly in 2024-25, your 2026 re-claims will hit a Hard Stop.

Master the Math: Reversing ITC without tracking interest is a costly mistake. Don’t overpay—use our [Section 50(3) Interest Formula] to protect your cash flow today.

The Opening Balance Validation Formula:

ECRS Opening Balance Formula

I noticed that most mismatches start because the opening balance in the ECRS ledger was carried forward with old errors. Think of it like a bank reconciliation—if your starting point is wrong, your 2026 re-claims will never balance. Before you trust the portal’s numbers, run your own math using the Audit-Trail formula. It’s better to find a 1-rupee error yourself than having a GST officer find it for you.

The Solution: If the formula doesn’t balance, you must reconcile your GSTR-9 of the previous year before filing the 3B of the current month. The portal’s AI cross-references the ECRS ledger against the Annual Return to verify the Reclaimable Pool.

Segment 2: Solving the Partial Payment Dilemma

A common minute doubt among CAs: What if the supplier pays only part of the tax? Rule 37A requires reversal by 30th November if the supplier hasn’t filed GSTR-3B. But 2026 has seen a rise in Short-Filings.

The Rule 37A Eligibility Ratio:

Rule 37A: Partial Reversal Math

The Strategy:

Don’t reverse the whole amount if the supplier has paid 80%. Reverse the 20% deficit. This protects the client’s working capital while maintaining 100% compliance.

💡 Rule 37A: Practical Case Study (Numerical Example)

Let’s assume that one of your client’s invoices amounts to ₹1,18,000, and the supplier has made a partial payment in GSTR-3B. Refer to the table below to understand exactly how much ITC needs to be reversed:

| Particulars | Amount (₹) | Remarks |

| Total Invoice Value (incl. 18% GST) | ₹1,18,000 | Total billing amount |

| ITC originally claimed (A) | ₹18,000 | Full ITC taken in GSTR-3B |

| Tax Payable by Supplier | ₹18,000 | Amount reflecting in GSTR-2A |

| Tax Paid by Supplier (GSTR-3B) | ₹14,400 | Supplier paid only 80% tax |

| Tax Deficit (Short-payment) | ₹3,600 | Balance tax not paid by supplier |

| Final Reversal Amount | ₹3,600 | That is all that needs to be reversed! |

Mathematical Breakdown for Audit-Trail:

You do not need to reverse the entire ₹18,000. The calculation will be as follows:

Rule 37A: Reversal Logic

Portal Accuracy: To ensure your math aligns with the GST portal’s logic, cross-reference your steps with the [GSTN Ledger Manual]. This is the official blueprint for ECRS management.

Segment 3: The Symmetry Check (Anti-ASMT-10 SOP)

The GST portal’s AI triggers a notice when it sees a spike in Table 4A(5). It assumes you are claiming Fresh ITC after the Section 16(4) deadline. To tag this credit as a re-claim, you must maintain Symmetry.

The Symmetry Formula:

The Symmetry Check: Table 4A(5) Logic

The Constraint:

The Mirroring Rule: Table 4D(1) Constraint

Here is a minute detail that many junior staff miss: they fill Table 4A(5) for the re-claim but leave Table 4D(1) blank. In the eyes of the GST AI, 4D(1) is your ‘Tag’. Without this tag, the system doesn’t know it’s a re-claim and instantly flags it as time-barred ITC. Ensure your 4D(1) entry is an exact mirror of your re-claim amount. This symmetry is your first line of defense against an automated notice.

Many juniors forget to fill Table 4D(1). In 2026, Table 4D(1) is not just informative; it is a mandatory flag for the AI. If 4D(1) is empty, the system applies the Section 16(4) logic and issues an automated notice.

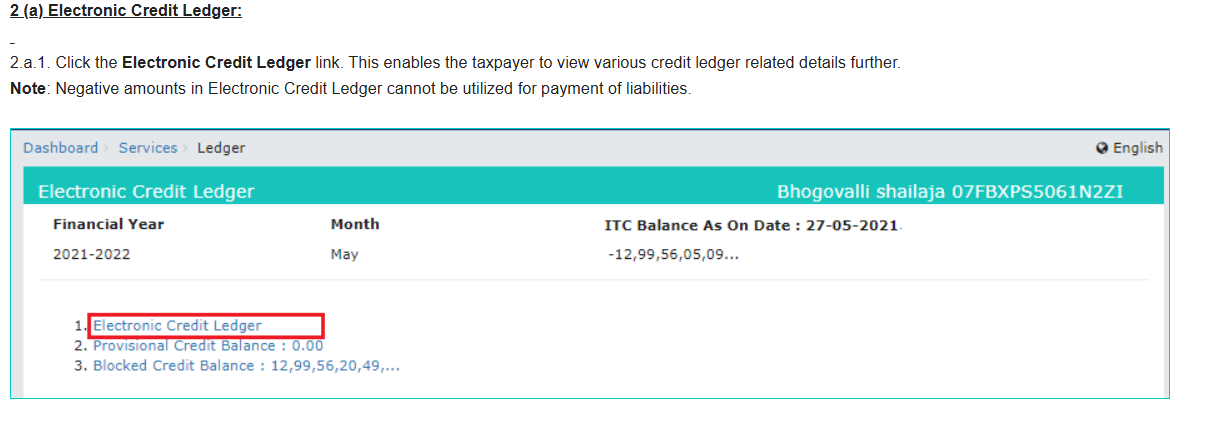

Navigation to view ITC balance and Reversal Statement on GSTN

Caption: Source: GST Portal User Manual for Ledger Management.

Stop the AI Notice: Most ASMT-10s are triggered by simple reporting gaps. Secure your filings with our [2026 Anti-ASMT-10 SOP] and stay ahead of the portal’s algorithm.

Segment 4: Navigating the Section 16(4) Dead-Zone

This is the most critical part of the blog. Section 16(4) says you can’t claim ITC after Nov 30th. Rule 37A says you can re-claim anytime the supplier pays.

The Collision: The portal’s validation engine is often programmed with 16(4) as the Master Rule, ignoring the Rule 37A exception.

The Maximum Re-claimable Limit Formula:

The Re-claim Cap: Maximum Limit Formula

Audit-Proof Your Data: Beyond Rule 37A, common credit reversals need a different logic. Check our [Rule 42 & 43 Strategy] to eliminate all technical risks in your tax audit.

How to defend this in an Audit ?

You must maintain a Month-wise Reclaim Tracker. If the department challenges a re-claim made in 2026 for an invoice of 2024, your defense is the Reversal Reference. You must be able to point to the exact GSTR-3B (Month/Year) where that credit was originally sacrificed.

Segment 5: The Legal Shield (ASMT-10 Template)

I have used this specific drafting in three recent cases, and it effectively shifts the burden of proof back to the department.

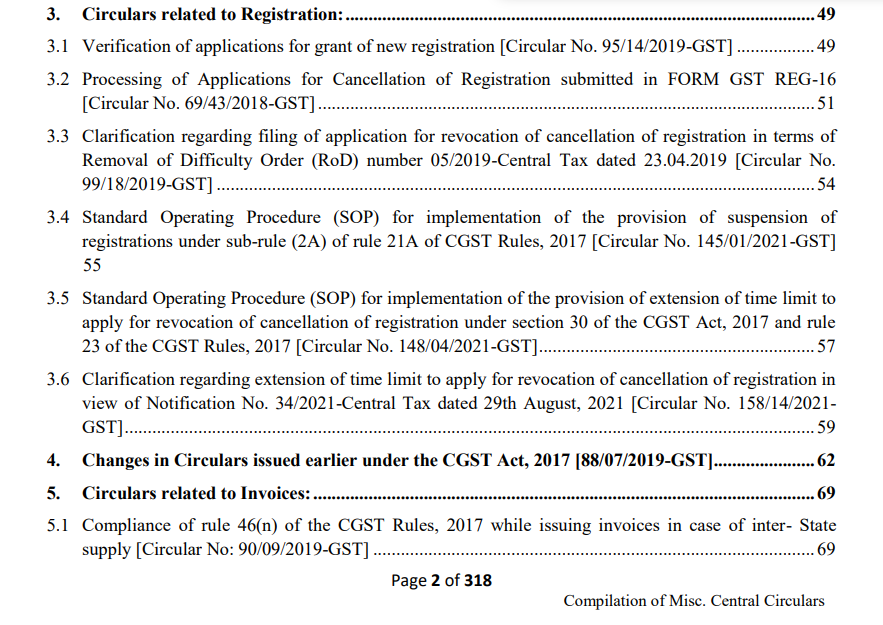

Official SOP and Circular index for GST Revocation and Invoices

Caption: Source: CBIC Compilation of Central GST Circulars.

Audit Strength: Every strong legal reply needs a solid circular reference. Cite the [CBIC Circular No. 170] to prove your re-claim’s legitimacy during tax audits or litigation.

When the notice arrives, do not give a generic reply. Use a Vested Rights argument.

Subject: Reply to ASMT-10 — Mismatch in ITC Re-claim

We submit that the ITC of ₹[Amount] in Table 4(A)(5) is a Re-availment, not an Availment. Section 16(4) imposes a time limit on the ‘initial’ taking of credit. However, Rule 37A provides a specific mechanism for re-claiming credit that was previously reversed. Once the supplier discharges their tax liability, the ‘Dead’ credit is resurrected. Under the principle of ‘Lex Specialis Derogat Legi Generali’ (Specific law overrides general law), the proviso to Rule 37A overrides the general limit of Section 16(4).

Deep Dive: The Minute Doubts

1. The Interest Trap

Problem: If I reverse under Rule 37A and re-claim later, do I get the interest back?

Reality: No. Interest paid at the time of reversal is generally treated as a Compensatory Payment for the delay. There is currently no provision in the GST Law to re-claim interest.

2. The Supplier’s Suo-Moto Cancellation

Problem: My supplier’s GST was cancelled. I reversed ITC. Now his GST is restored and he paid the tax. Can I re-claim?

Yes, but the portal might show a GSTR-2B Mismatch. You must bridge this using the Audit-Trail Formula. The restoration date of the supplier must be linked to the ECRS ledger entry to prove the link.

3. The Block Credit Conflict

Problem: What if the ITC I reversed under 37A later falls under Section 17(5)?

Analysis: If the nature of the expense changed (e.g a commercial vehicle converted to personal use), you cannot re-claim it even if the supplier pays. The Eligibility check happens twice—once at initial availment and once at re-claim.

🚀 Professional Tool: Download the Rule 37A Audit-Trail & Reclaim Tracker (Excel) to reconcile your ECRS ledger in minutes.

Conclusion: From Compliance to Solution Architecture

In 2026, being a CA is about Mathematical Defense. The conflict between Section 16(4) and Rule 37A is the ultimate test of your technical depth. By using these five formulas and maintaining a strict ECRS tracker, you move from guessing to guaranteeing your client’s tax safety.

Do not let an automated algorithm steal your client’s capital. Build your Audit-Trail today.

Frequently Asked Questions (Professional Grade)

Q1: Is there a 100% guarantee that the ASMT-10 will be dropped ?

No. While the law is on your side, the portal’s AI is rigid. If the automated notice isn’t dropped, you must move to manual adjudication with the documents we discussed.

Q2: Can we re-claim ITC in GSTR-3B if it’s not appearing in GSTR-2B again ?

Yes. Rule 37A re-claims are based on the fact of payment by the supplier, not necessarily a second appearance in your 2B. Your evidence is the supplier’s GSTR-3B filing status.

Q3: What if I forget to report the reversal in ECRS ?

This is a major risk. If the reversal isn’t in the ECRS, the portal treats your re-claim as Fresh ITC and will almost certainly block it under 16(4).

Note : Always take a screenshot of the supplier’s ‘GSTR-3B filing status’ and keep it in your audit file. In 2026, documentation is your greatest insurance.

Disclaimer

This guide is for CAs, Tax Heads, and Accountants. It is based on 2026 GST interpretations. Tax laws change rapidly; always consult the latest GSTN circulars. ServiceMoney.in is an educational platform and does not provide legal guarantees.

Meet the Expert

Author Bio: Anurag Panchal is the Founder of AllRoundUpdate & ServiceMoney and a dedicated Financial Educator. With over 135+ technical guides on YouTube, he has helped 10,000+ readers simplify complex GST compliance, Tally Prime workflows, and Digital Marketing strategies through practical, formula-driven insights. Follow his expert masterclasses on YouTube @Educationanurag.