If you think accepting an invoice on the IMS portal means your ITC is safe, you might be in for a rude shock. In 2026, the GST portal’s AI doesn’t care if your 2B matches perfectly; it’s looking for the supplier’s 3B filing status. One small gap, and an automated ASMT-10 notice is at your door. To survive this AI-driven scrutiny, you need a bulletproof Rule 37A Defense. Let’s decode the practical litigation strategies and forensic formulas I’ve developed to protect your credit in high-stakes audits.

If you followed my previous guide on ASMT-10 & GSTR-9 Mapping, you’ve mastered internal reversals. But here is the 2026 nightmare: You accepted an invoice in the IMS (Invoice Management System), your GSTR-2B looks perfect, but your supplier never filed their GSTR-3B.

The Result? An automated ASMT-10 notice triggered by the portal’s AI, demanding a full reversal of ITC with interest. This guide isn’t about reporting; it’s about litigation defense. We’re decoding that tricky overlap between the IMS “Acceptance” and the Section 16(4) time-bomb using professional-grade formulas and forensic strategies.

1. The 2026 Reality Check: IMS Acceptance ≠ Guaranteed ITC

The Invoice Management System (IMS) is a great tool, but it’s not a safety net. It only tells you that the vendor has uploaded the data. For a professional, the real job starts after ‘Accepting’ the invoice. You need to ensure the tax actually reaches the government treasury, otherwise, Rule 37A will force you to pay it back with interest.

Before handling Rule 37A, ensure your internal GSTR-9 mapping is accurate. This is crucial for AI-driven audits. Follow our guide to Stop ASMT-10: GSTR-9 & IMS Guide to align your data perfectly.

To identify your risk, you must calculate your Vendor Compliance Scorecard (VCS).

Formula 1: Vendor Compliance Scorecard (VCS)

Vendor Compliance Scorecard (VCS)

In simple terms: VCS = (Total Invoices Filed in GSTR-3B by Vendor ÷ Total Invoices Accepted by you in IMS) × 100. It measures how many of your ‘Accepted’ invoices are actually backed by tax payments.

Professional Benchmark: If a vendor’s VCS is below 95%, they are a “High-Risk” entity. Under the 2026 scrutiny norms, the portal’s AI flags the gap between IMS Acceptance and Supplier filing instantly.

2. Strategic Shift: From GSTR-9 Mapping to Rule 37A Defense

To satisfy a smart audience, we must differentiate between what we did in GSTR-9 and what we must do now.

| Feature | The GSTR-9 Phase (Rule 42/43) | The 2026 Defense Phase (Rule 37A) |

| Risk Source | Internal (Your Exempt Turnover) | External (Vendor’s Default) |

| Timeline | Annual Re-computation | Monthly Surveillance |

| Notice Trigger | Table 7 Mapping Errors | GSTR-3B Filing Gaps |

| ECRS Impact | Permanent Reversal | Temporary Reversal & Reclaim |

For more context, you can read the Official Rule 37A Notification. This CBIC document outlines the legal grounds for all ITC reversal and reclaim procedures.

Rule 37A Reversal Liability (RL)

In simple terms: Reversal Liability = Total ITC of all ‘Accepted’ IMS invoices whose suppliers have NOT filed GSTR-3B by the 30th September deadline.

3. The Mathematics of Rule 37A: Reversal & Interest Formulas

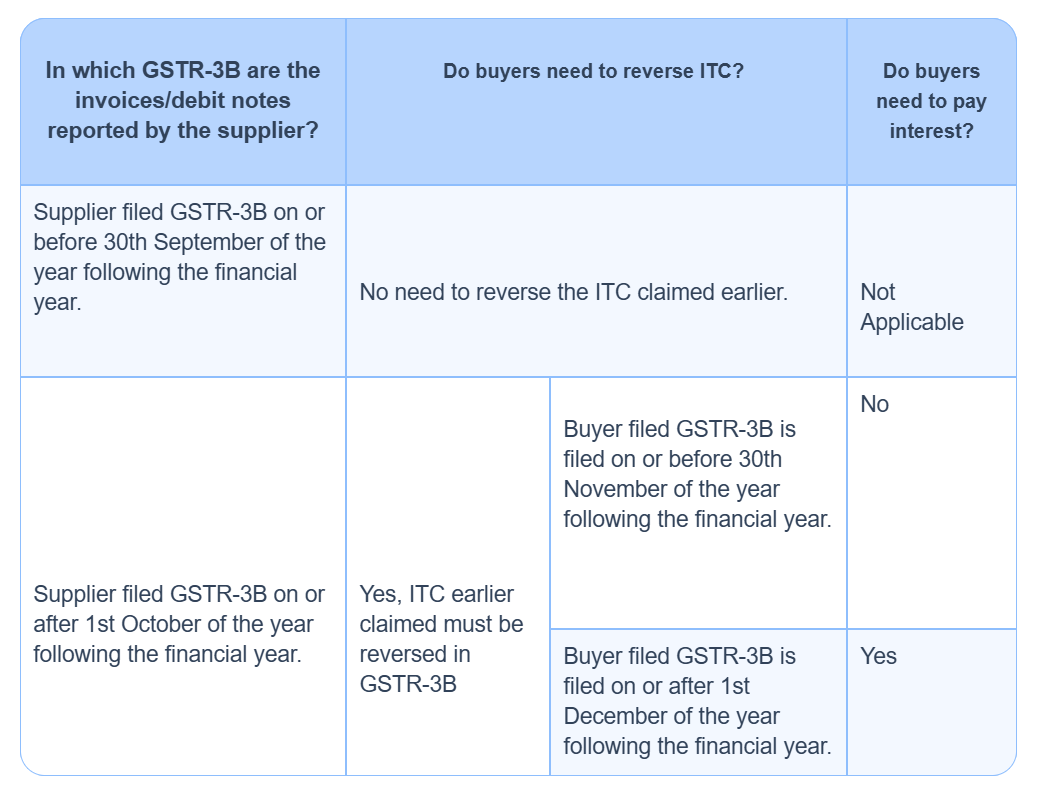

In 2026, the GST portal doesn’t allow for vague explanations. If the supplier fails to file GSTR-3B by the 30th of September following the end of the FY, you must calculate your Rule 37A Reversal Liability (R_L).

Rule 37A ITC Reversal and Interest Scenarios

Caption: Source: Statutory Provisions of Rule 37A. This table outlines the critical deadlines (Sept 30th & Nov 30th) for ITC reversal and interest applicability based on supplier’s filing status.

Formula 2: The Rule 37A Reversal Liability (R_L)

If you fail to reverse this by November 30th, interest kicks in. However, smart professionals use the Section 50(3) Defense to save costs.

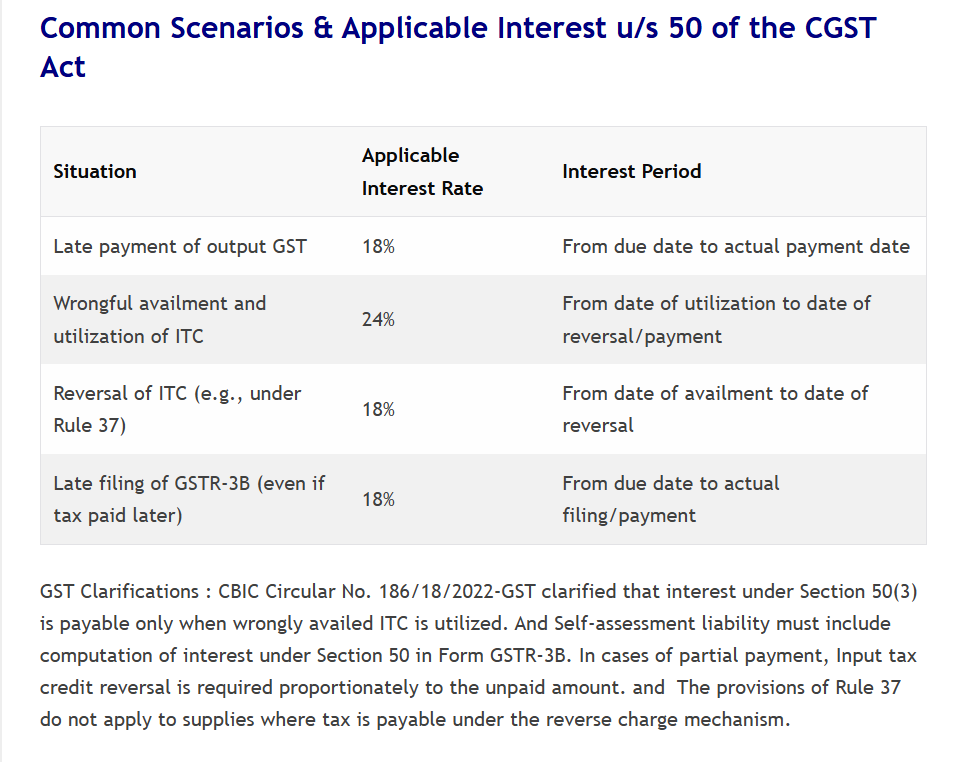

Formula 3: The Net Interest Liability (The 50(3) Defense)

GST Interest Rates Table Section 50

Caption: Source: CBIC Circular No. 186/18/2022-GST. A comparative study of interest rates applicable on delayed payments and wrongful utilization of ITC.

Simply calculating liability isn’t enough; you must eliminate the root cause. Learn how to Eliminate ASMT-10 Risks using our professional Rule 42 & 43 strategies to secure your credit

Net Interest Liability (IntLiability)

In simple terms: Interest = (Wrongly Utilized ITC Amount) × 18% × (Number of days utilized ÷ 365). Remember, interest applies only if your cash liability was saved using this credit.

The Pro Secret: If your Electronic Credit Ledger (ECL) balance remained higher than the disputed ITC during the entire period, your ITC_{Utilized} is Zero, and thus your interest liability is Zero.

4. The Section 16(4) & IMS “Time-Bomb”

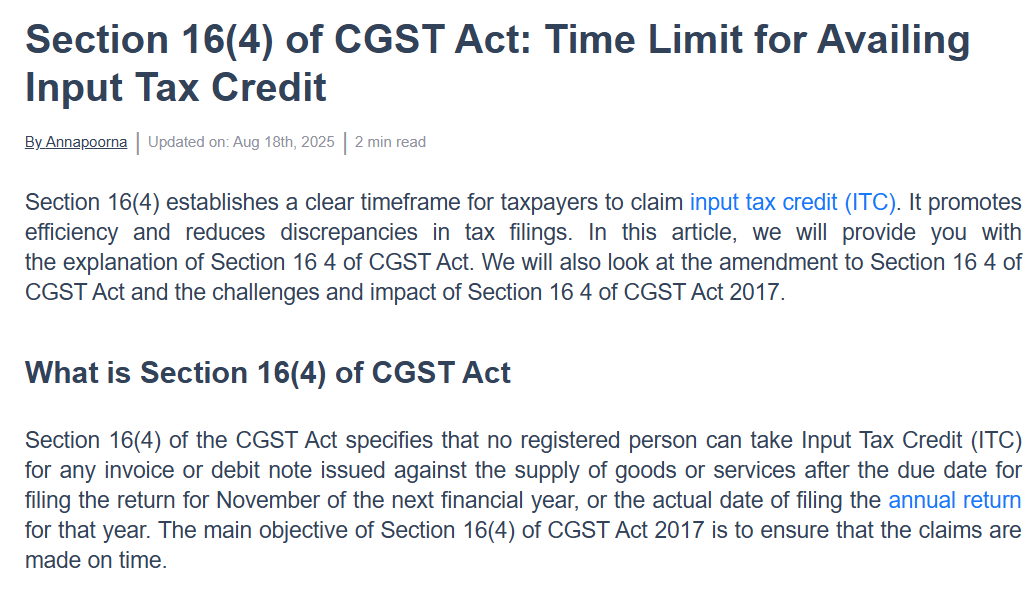

The ‘Pending’ folder in your IMS is a double-edged sword. While it helps you defer credit for goods not received, it has a strict expiry date under Section 16(4). If you leave an invoice in ‘Pending’ past the November 30th deadline, that money is gone forever. I recommend a monthly aging report to keep this in check.

Section 16(4) CGST Act ITC Time Limit

Caption: Source: Central Goods and Services Tax Act. Section 16(4) defines the ‘Hard-Stop’ deadline for availing ITC, emphasizing why IMS ‘Pending’ invoices must be cleared before November 30th.

Deadlines are non-negotiable under GST law. Refer to the statutory language of Section 16(4) CGST Act to ensure your credits don’t lapse after the November 30th deadline.

Formula 4: The IMS “Pending” Aging Ratio (P_A)

IMS “Pending” Aging Ratio (PA)

In simple terms: Aging Ratio = (Invoices pending in IMS for more than 90 days ÷ Total Available ITC) × 100. This helps you track credit that is at high risk of expiring under Section 16(4).

The Strategy: If your P_A is higher than 10%, your cash flow is at risk. Any invoice marked as “Pending” that crosses the Nov 30th deadline without being “Accepted” is permanently lost. You cannot reclaim it even if the goods are received later.

5. Case Study: The “Silent Default”

I recently came across a client case similar to this, where a small oversight led to a massive notice. Here is how we tackled it.

Scenario: Anurag Tech Solutions accepted an invoice of ₹5,00,000 in the IMS in July 2025. The vendor filed GSTR-1, so it appeared in 2B. However, the vendor skipped GSTR-3B for the entire year.

The Trap: In October 2026, the portal triggered an automated ASMT-10.

The Solution:

- Calculate R_L :- Identify the ₹5,00,000 liability.

- Action :- Reverse it in GSTR-3B (Table 4B2) before Nov 30th to avoid interest.

- Reconcile ECRS :- Use the ECRS Reconciliation Formula to ensure the portal tracks your “Right to Reclaim.”

Formula 5: The ECRS Reconciliation Formula (E_{Rec})

ECRS Reconciliation Formula (ERec)

In simple terms: Final ECRS Balance = (Opening Balance + New Reversals) – Total Reclaims. This ensures your Electronic Credit Reversal and Re-claimed Statement stays accurate to avoid automated notices.

A mismatch in this formula is the #1 reason for DRC-01 notices in 2026.

6. Forensic Reply to ASMT-10: The Legal Defense

When you reply to an ASMT-10 notice, don’t just quote the law—quote the intent. The Arise India judgment is your strongest shield. It clearly says that a buyer cannot be expected to do the ‘impossible’ task of policing the supplier. Use this judgment to argue that your ITC is a vested right, as long as your payment and e-way bills are genuine.

Arise India vs Commissioner GST Delhi High Court Judgment

Caption: Source: Delhi High Court Judicial Records. This landmark judgment serves as a legal defense for buyers against ITC reversals caused by supplier-side defaults (Vicarious Liability).

- Case Law Reference: Arise India Ltd vs. Commissioner of Trade & Taxes — The buyer cannot be expected to do the “impossible” (verify the supplier’s actual payment to the Treasury).

Already received an ASMT-10 notice? Don’t panic. Use our proven framework and Download ASMT-10 Reply Templates to draft a legally strong response today.

7. Automated Vendor Compliance SOP

Standard practice in 2026 requires an Automated Compliance Dashboard.

1. Monthly Export :- Download IMS “Accepted” vs. “Supplier 3B Filing Status.

2. Filter Mismatches :- Flag vendors where VCS < 100%.

3. The Nov 30 Hard Stop :- Clear all “Pending” IMS entries for the previous FY before the clock strikes midnight on Nov 30th.

To implement your SOP effectively, I recommend downloading the Official GST IMS Advisory (PDF). This technical manual provides step-by-step instructions for managing and accepting invoices on the new portal dashboard.

8. Frequently Asked Questions (FAQs)

Q1. If I reverse ITC under Rule 37A, can I reclaim it later ?

Yes. Unlike Rule 42/43, Rule 37A reversal is temporary. You can reclaim it in Table 4(A)(5) once the supplier files their return.

Q2. Does IMS acceptance protect me from Rule 37A ?

No. IMS acceptance only validates the Existence of the invoice, not the Payment of Tax.

Q3. What happens if I don’t reverse by Nov 30th ?

You will be liable to pay the amount via DRC-03 with 18% interest from the date of utilization.

Q4. Can I pay Rule 37A reversal using ITC ?

Yes, since it is a reversal of wrongly availed credit, you can use your Electronic Credit Ledger to pay it back before Nov 30th.

Q5.Will the GST Portal send a prior warning before Rule 37A reversal ?

Ideally yes, the portal is designed to send system-generated intimations. However, in 2026, the AI triggers automated ASMT-10 notices immediately after the deadline. Waiting for a warning is risky; proactive reversal is the best defense.

Q6. Do I need to pay interest if I have sufficient balance in my Credit Ledger ?

This is the Section 50(3) Defense. If your Electronic Credit Ledger balance never fell below the disputed amount, you have not “utilized” the credit. In such cases, no interest is payable even if the reversal is done after the deadline.

Conclusion: Data Integrity is Your Shield

In 2026, GST compliance is no longer about filing; it is about Data Integrity. The IMS Trap is designed to catch those who rely on automation without oversight. By applying the Aging Ratio and Compliance Scorecards, you turn your accounting department into a forensic fortress.

Action Item: Review your “IMS Pending” folder today. If those invoices relate to the previous Financial Year, your window to act is closing fast.

Disclaimer

This guide is for educational purposes for the 2026 tax regime. Always consult a qualified CA for litigation support.

Meet the Expert

Author Bio: Anurag Panchal is the Founder of AllRoundUpdate & ServiceMoney and a dedicated Financial Educator. With over 135+ technical guides on YouTube, he has helped 10,000+ readers simplify complex GST compliance, Tally Prime workflows, and Digital Marketing strategies through practical, formula-driven insights. Follow his expert masterclasses on YouTube @Educationanurag.