Calculating Input Tax Credit (ITC) reversals under Rules 42 and 43 is only half the battle. ASMT-10 Notices: GSTR-9 Rule 42/43 mismatches. If you’ve followed our previous guide on the Professional Rule 42 & 43 Formula Strategy, you already know how to compute the “Monthly Provisional Reversal .

However, in 2026, the real danger isn’t the math—it’s the reporting integrity. With the GST portal’s AI-driven scrutiny engines and the fully active Electronic Credit Reversal and Re-claimed Statement (ECRS), a single mapping error between your GSTR-3B and GSTR-9 is an open invitation for an automated ASMT-10 Notice.

This guide moves beyond basic compliance into Strategic Reconciliation and Advanced Reporting.

1. Why the ITC ‘Reversal Gap’ is Your Biggest Risk in 2026

Most accountants are losing sleep over Table 8A mismatches, and honestly, it’s not just about the numbers anymore. In 2026, the GST portal’s AI scrutiny has become incredibly sharp.

It doesn’t just scan for totals; it looks for the ‘why’ behind every gap. If your books don’t talk to your GSTR-2B perfectly, you’re basically sending an open invitation for an automated ASMT-10 notice. We need to stop thinking like data entry operators and start thinking like forensic auditors.

In 2026, the portal’s AI doesn’t just look at totals; it looks at the nature of the gap. If you cannot justify why your claimed ITC is lower than your 2B reflected ITC, the system assumes a clerical error or hidden liability. To solve this, you need a reporting strategy that mirrors the department’s audit logic.

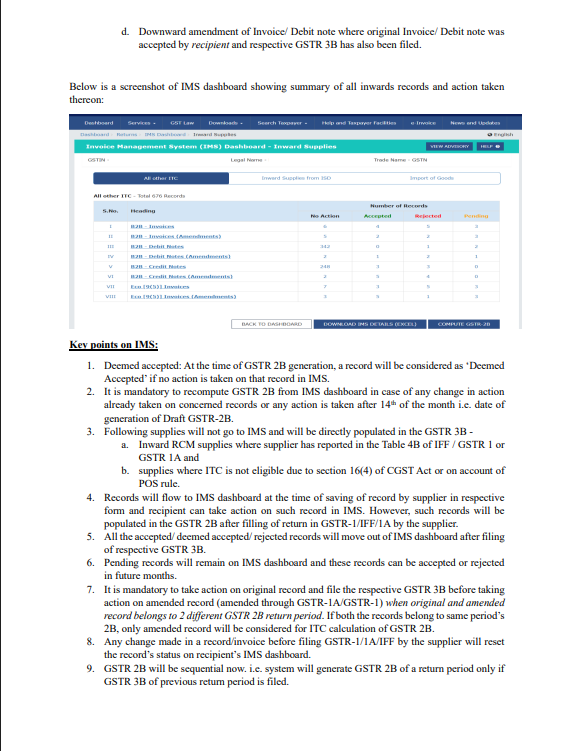

2. The “IMS” (Invoice Management System) Strategy

With the Invoice Management System (IMS) fully operational in 2026, the “Pending” invoice category has created a new reporting layer.

Live GST IMS Dashboard for Inward Supplies Management.

Caption: The 2026 IMS Dashboard allows taxpayers to take strategic action (Accept/Reject/Pending) on inward invoices.

The Problem:

If you have marked an invoice as “Pending” in the IMS, that ITC will not flow into your GSTR-3B, but it will stay in the GSTR-2B ecosystem.

To track real-time portal updates on pending invoices, refer to the Official GSTN Advisory on IMS. It provides the necessary legal framework to handle your 2026 inward supplies without errors.

The GSTR-9 Solution:

When filing GSTR-9, these “Pending” invoices must be excluded from Table 6 but carefully accounted for in Table 8. To avoid an ASMT-10, you must maintain a separate ledger for “IMS Pending ITC” and ensure it matches the difference between Table 8A and Table 6A. This is a futuristic reporting logic that ensures the AI doesn’t flag your “unclaimed” credit as an “omission.”

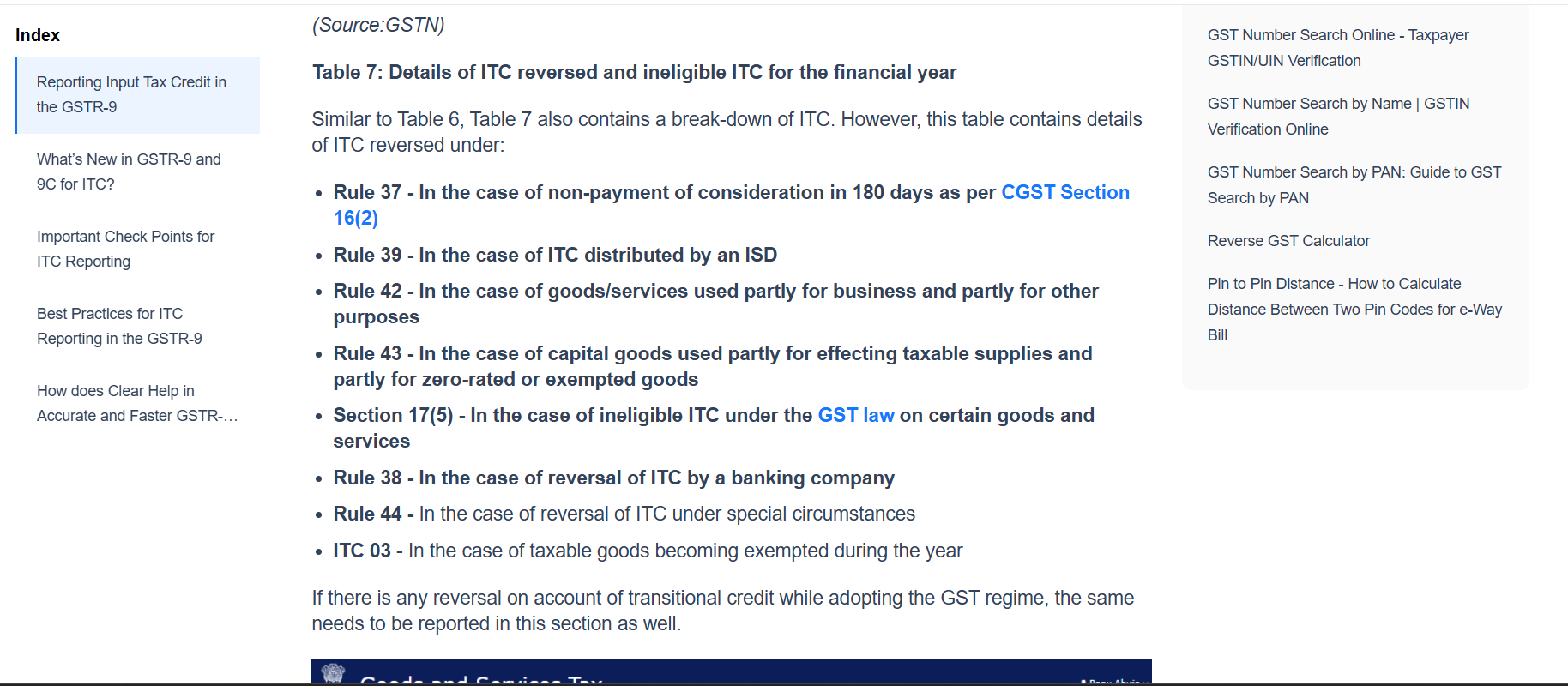

3. The GSTR-9 “Table 7” Mapping Matrix

In your monthly GSTR-3B, you likely dumped all reversals into Table 4(B)(1). For GSTR-9, this “lump sum” approach is a red flag. Professionalism lies in bifurcation.

| Nature of Reversal | Statutory Rule | GSTR-9 Table | Professional Justification |

|---|---|---|---|

| Non-payment to Vendor | Rule 37 | Table 7A | Temporary reversal; highly scrutinized in 2026. |

| Exempt/Personal (Inputs) | Rule 42 | Table 7C | Permanent reversal based on annual turnover ratio. |

| Capital Goods | Rule 43 | Table 7D | 60-month staggered amortization mapping. |

| Ineligible ITC | Sec 17(5) | Table 7E | Blocked credits (Insurance, Food, etc.). |

GSTR-9 Table 7 Statutory Mapping for ITC Reversal

Caption: GSTR-9 Table 7 provides a dedicated structure for reporting reversals under Rules 37, 42, 43, and Section 17(5).

4.How to Audit-Proof Your Annual Calculations

To satisfy a smart audience, we must look at the Annual Aggregate Recalculation.

Reporting accurate data in Table 7 is critical because most reversals are driven by complex calculations. To ensure you don’t miss any credit, it is helpful to master the Professional Rule 42 & 43 Formula Strategy which helps in calculating exempt and business-use ratios effectively.

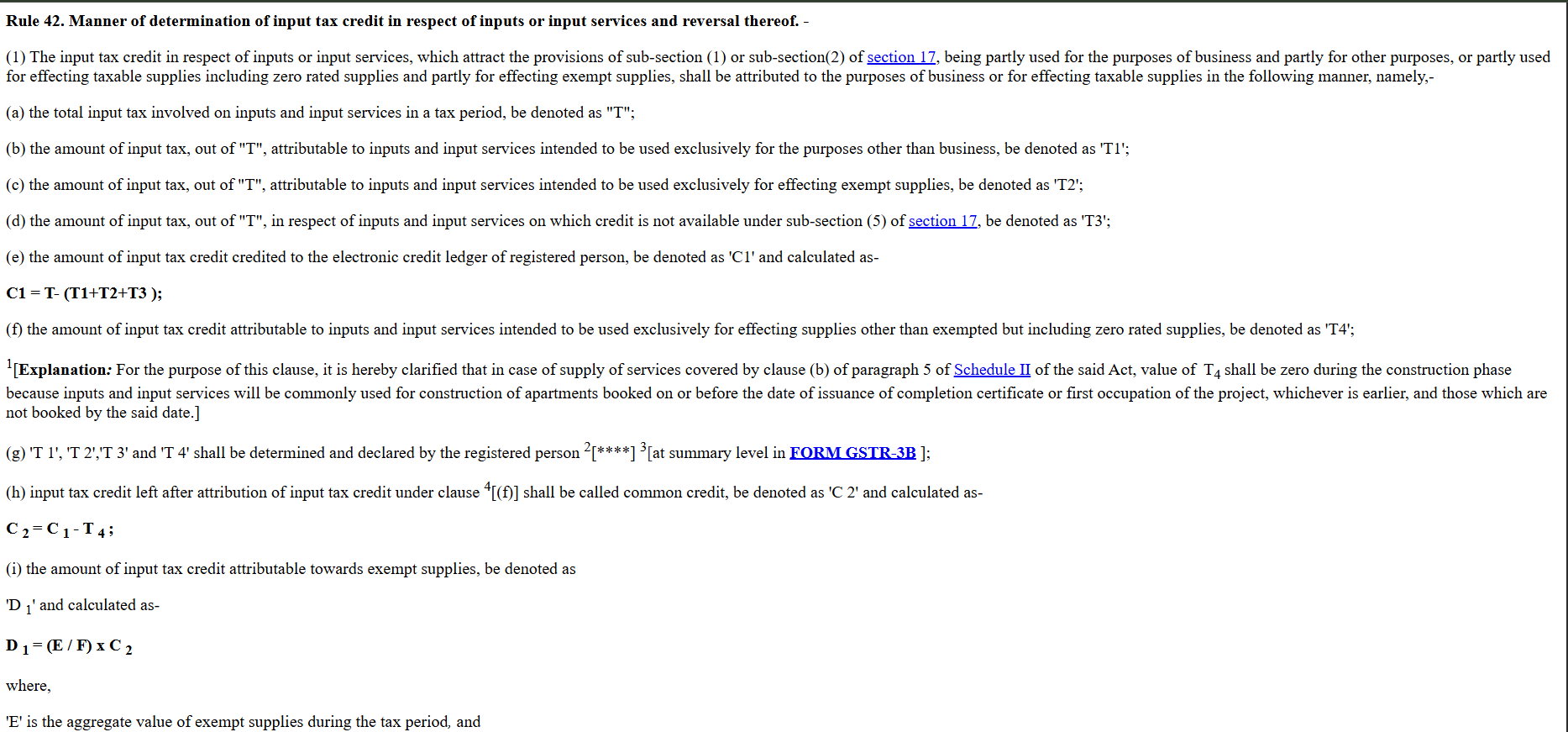

A. The Annual Re-computation (Rule 42)

At the end of FY 2025-26, you must calculate the Final Annual Reversal ($D_1^ + D_2^*$)*.

D1* = Eannual Fannual × C2*

The Professional Trap: If your monthly reversals are less than this annual figure, the shortfall must be paid via DRC-03 with interest.

There’s a lot of noise in the professional community about Rule 37 and interest starting dates. However, the legal ground is quite clear under Section 50(3).

Interest isn’t a penalty for a clerical error; it’s a charge for ‘using’ the government’s money. If your electronic credit ledger balance was consistently higher than the reversal amount, you have a solid technical defense to argue for zero net interest. It’s all about proving ‘non-utilization’ through your ledger history.

Statutory Formula for ITC Reversal under Rule 42.

Caption: The legal definition of Rule 42 formula used for proportionate ITC reversal based on exempt turnover ratio.

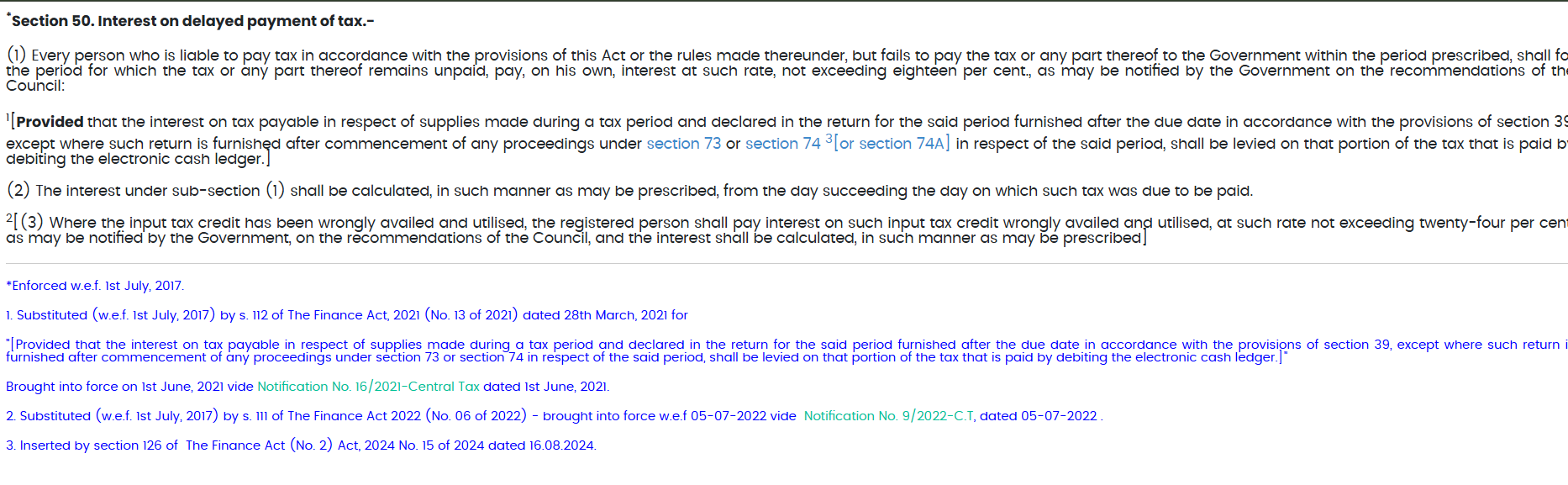

B. The Interest Controversy: Date of Availment vs. 181st Day

There is a massive debate regarding Rule 37 (180-day rule). Does interest start from the invoice date or the date the 180 days expire?

Section 50(3) Interest on Wrongly Availed and Utilized ITC.

Caption: As per Section 50(3), interest is levied only when ITC is both wrongly availed and actually utilized for tax payment.

Any discrepancy between your monthly returns and GSTR-9 reversals can trigger departmental scrutiny. If you receive a notice regarding mismatched ITC, you can follow our comprehensive guide on How to Reply to GST ASMT-10 to draft a professional response and avoid heavy penalties.

The Technical Defense: Based on Section 50(3), interest is only applicable if ITC has been “Availed and Utilized.” If your credit ledger had a balance higher than the reversal amount during the entire period, you can argue for a “Net Interest” liability of zero.

Net Interest = (Utilized ITC) × 18% × ( Period of Utilization 365 )

5. Real-World Case Study: “The Mixed-Supply Precision

Let’s take the example of my firm, Anurag Tech Solutions, to simplify this. Imagine you have a common credit pool of ₹10 Lakhs but your exempt turnover is 20% of the total. While the math says you reverse ₹2 Lakhs, the real professional challenge is where you show this in GSTR-9.

If you don’t map this specifically to Table 7C and Table 8E, the GST portal’s AI will flag the difference between your 2B and 3B as a mismatch. It’s these small mapping details that save you from an unwanted tax notice.

The Data Points:

- Total ITC (T): ₹50,00,000

- Exclusively Exempt (T2): ₹4,00,000

- Blocked Credit (T3): ₹2,00,000

- Common Credit Pool (C_2): ₹10,00,000

- Exempt Turnover (E): ₹2 Crores | Total Turnover (F): ₹10 Crores

Step 1: The Calculations

- D_1 (Proportionate): (2/10) \times 10,00,000 = ₹2,00,000

- D_2 (Personal @ 5%): 5\% \text{ of } 10,00,000 = ₹50,000

- Total Permanent Reversal: ₹2,50,000

Step 2: The “Smart” Mapping

Instead of a single entry, the professional avoids ASMT-10 by populating:

- GSTR-9 Table 7C: ₹2,50,000

- GSTR-9 Table 7E: ₹2,00,000

- GSTR-9 Table 8E (The Reconciliation): Report ₹2,50,000 here.

Why this matters? In 2026, Table 8A will show the full ₹50 Lakhs from your 2B. If your Table 6 (Actual Claimed) shows only ₹45.5 Lakhs, the system sees a ₹4.5 Lakh gap. By populating Table 8E, you “tell” the AI: “I didn’t take this credit because Rule 42 required a reversal.” This prevents the automated notice.

6. GSTR-9 Table 6H vs Table 6A1: The Reclaim Secret

What happens when you finally pay the vendor after the 180-day reversal? You are allowed to reclaim that ITC.

- Rule 37 Reclaims: These must be reported in Table 6H of GSTR-9.

- Other Reclaims: General reclaims from the current year flow into Table 6A1.

For accurate reporting codes and statutory guidelines on ITC reclaims, follow the CBIC Manual on GSTR-9 Filing. This ensures your re-claimed credits are fully verified by departmental standards.

Mixing these up is the quickest way to create a mismatch in the ECRS Ledger. Table 6H is specifically designed for “Amount reclaimed which was reversed earlier,” and using it correctly provides a clean audit trail for the department.

7. Rule 43: Capital Goods Math

Tm = ITC on Capital Asset 60 × ( E F )

Strategic 5-Year (60 Month) Staggered ITC Reversal mapping

Cross-verify your 60-month amortization calculations with the Statutory GST Rules for ITC. This reference helps you justify staggered reversals during high-stakes forensic audits.

Advanced Strategy: If an asset was 100% taxable for 2 years but shifts to “Mixed Supply” in 2026, you must reduce the ITC by 5% for every quarter of “taxable only” use before bringing the remainder into the Common Credit Pool.

8. Table 8A Reconciliation Strategy

This is where 90% of notices originate. Use Table 8E and 8F to explain why ITC available in 2B was not availed. Your goal is to make Table 8I (Grand Total) as close to zero as possible.

I always tell my clients that Table 8A is where 90% of GST notices are born. Your goal should be to explain every single rupee of difference. Whether it’s an invoice you marked as ‘Pending’ in the IMS or a reversal you made under Rule 42, use Tables 8E and 8F to clear the air.

Before finalizing your annual reversals, always ensure that your books are perfectly aligned with your portal data. Using Smart Excel GSTR-2B Reconciliation Automation can simplify this process, making your GSTR-9 filing faster, more accurate, and high-quality for audit purposes.

When the Grand Total in Table 8I stays near zero, you’ve essentially built a firewall around your data that the department’s AI can’t easily penetrate.

9. AI-Ready Documentation Checklist

- [ ] IMS Pending Tracker: List of invoices not accepted in the portal.

- [ ] Rule 42 Working Sheet: Annual aggregate E/F ratio calculation.

- [ ] Table 6H vs 4(D)(1) Reconciliation: Ensuring reclaims match the ECRS statement.

- [ ] Section 50(3) Utilization Summary: To defend against excess interest demands.

Frequently Asked Questions (FAQs)

Q1. Can I reclaim Rule 42 reversals in future years ?

No. Rule 42 (Inputs) and Rule 43 (Capital Goods) reversals based on exempt turnover are permanent in nature. Unlike Rule 37 (180-day non-payment rule), these amounts are not re-claimable. Any attempt to reclaim these will cause an immediate mismatch in your Electronic Credit Reversal and Re-claimed Statement (ECRS), leading to a system-generated alert.

Q2. What are the consequences if Table 8A shows a negative balance after reconciliation ?

A negative Table 8A indicates that your “Actual ITC Claimed” exceeds the “ITC reflected in GSTR-2B.” This is a high-risk scenario that triggers automated ASMT-10 notices. To safeguard your position, you must maintain a granular “Reconciliation Statement” justifying the variance through RCM payments, IGST on Imports (not in 2B), or clerical timing differences.

Q3. Does ITC marked as “Pending” in the IMS reflect in Table 8A ?

Yes. “Pending” invoices remain an integral part of your GSTR-2B ecosystem, so they will auto-populate in Table 8A. However, since you haven’t claimed them in GSTR-3B, they will be absent from Table 6A. To prevent AI-driven scrutiny for this gap, you must report this difference in Table 8E (ITC available but not availed) to keep your portal mapping clean.

Q4. When is interest applicable on Rule 43 Annual Re-computations ?

If your Final Annual Reversal exceeds the total monthly provisional reversals already made, the shortfall must be paid along with interest under Section 50(3). Strategic Tip: If your Electronic Credit Ledger balance remained consistently higher than the shortfall amount throughout the year, you can invoke the “Availed and Utilized” principle to argue for a zero net interest liability.

Q5. Can incorrect mapping in GSTR-9 Table 7 affect the ECRS Ledger ?

Absolutely. In 2026, the GST portal’s AI performs forensic-level validation on Table 7 mapping. If you accidentally map permanent reversals (Rule 42/43) into the temporary reversal category (Rule 37), it will incorrectly inflate your Electronic Credit Reversal and Re-claimed Statement (ECRS) balance. This discrepancy is a primary trigger for automated demand notices during annual processing.

Conclusion: Data Integrity is Your Best Defense

In 2026, GST compliance is about Data Integrity. Moving from “Monthly Calculation” to “Annual Strategic Reporting” separates a bookkeeper from a Tax Professional. By aligning your IMS strategy, GSTR-9 Table 7/8 mapping, and utilizing the reclaim secrets in Table 6H, you build an “Audit-Proof” accounting system.

Disclaimer

This guide is for educational purposes. Always consult a qualified CA for specific filings.

Note: Tax laws are dynamic. While I strive for 100% accuracy based on the 2026 updates, please verify with official GSTN advisories before filing.

Meet the Expert

Author Bio: Anurag Panchal is the Founder of AllRoundUpdate & ServiceMoney and a dedicated Financial Educator. With over 135+ technical guides on YouTube, he has helped 10,000+ readers simplify complex GST compliance, Tally Prime workflows, and Digital Marketing strategies through practical, formula-driven insights. Follow his expert masterclasses on YouTube @Educationanurag.