As we navigate the 2026 GST landscape, I’ve noticed a shift. The department isn’t just checking your bills anymore; they are eyeing your cash flow. If you are managing clients with high turnovers but low margins, Rule 86B and 37A are your biggest enemies. Here is how we are handling this strategic war on the ground.

This is no longer a simple tax compliance issue; it is a strategic war against a system-driven blockade on your client’s cash flow.

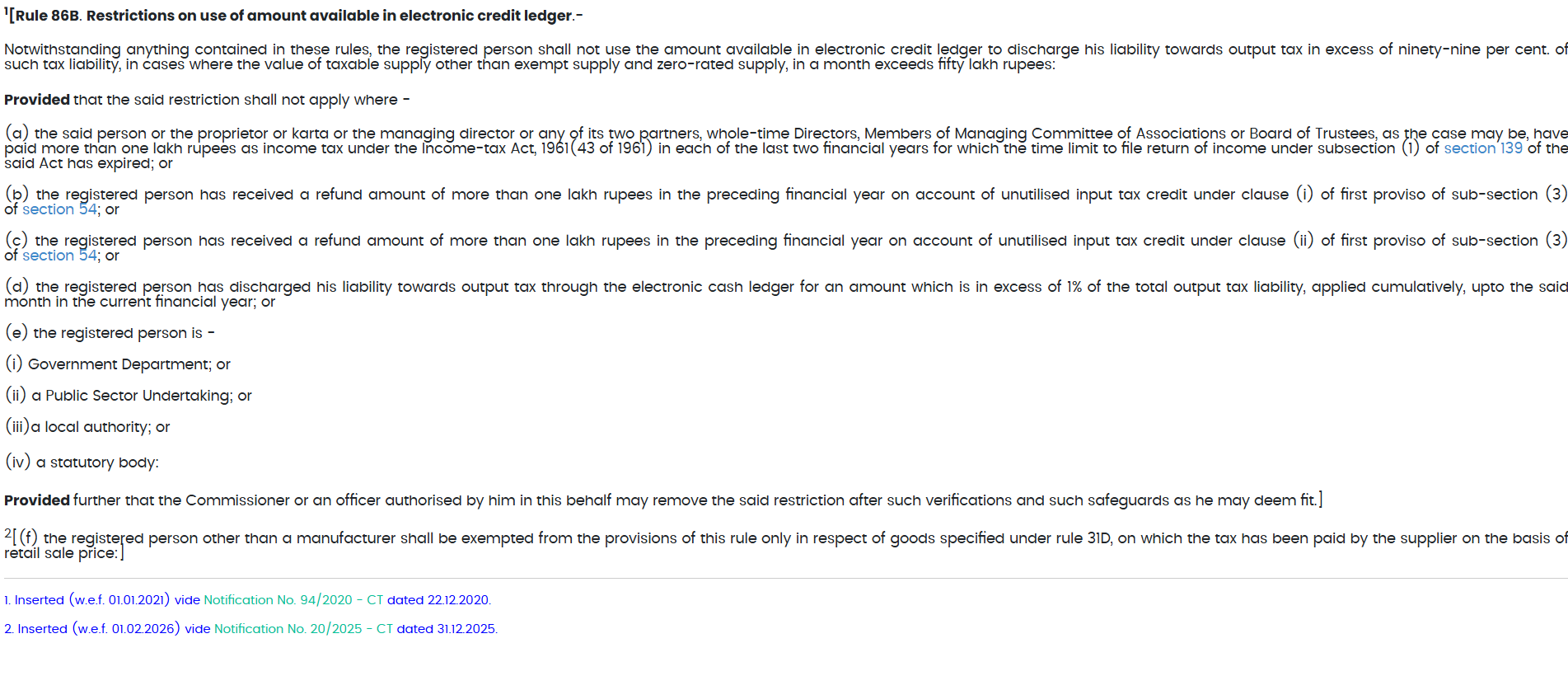

Understanding Rule 86B (The Legal Mandate)

Before discussing the pain, let’s establish the law. Introduced via Notification No. 94/2020 – Central Tax, Rule 86B was inserted into the CGST Rules, 2017.

What is Rule 86B?

It is a Restricted Utilization mandate. It states that notwithstanding anything contained in the rules, certain registered persons shall not use more than 99% of the Input Tax Credit (ITC) available in their electronic credit ledger to discharge their output tax liability.

Rule 86B Legal Provisions CBIC

Caption: Source: CBIC Statutory Text (Notification 94/2020). This confirms the ₹50 Lakh monthly threshold and the 1% cash mandate.

The Criteria:

- Applicability: Taxable supply value (excluding exempt and zero-rated supply) exceeds ₹50 Lakhs in a month.

- The Restriction: You must pay at least 1% of your total output liability in CASH through the Electronic Cash Ledger.

1. Rule 86B: The Artificial Debt for High-Value Taxpayers

Legal Anchor: Rule 86B of CGST Rules (The 1% Mandate).

The Ground-Level Depth: Why 1% is a 100% Headache

On the surface, paying 1% tax in cash seems trivial. But for a professional managing a high-turnover client, it is an Artificial Debt.

The Dead Capital Paradox: I recently handled a case where a client had ₹50 Lakhs in their credit ledger, yet they had to borrow from the bank to pay the 1% mandatory GST under Rule 86B. This is exactly what I call ‘Artificial Debt.’ It’s frustrating because the law treats your genuine tax asset as a non-existent entry.

The Professional’s Calculation:

To determine the mandatory cash outflow, use the following formula:

Rule 86B: The 1% Cash Mandate Math

Audit Strategy: This formula only triggers if monthly taxable turnover exceeds ₹50 Lakhs. Always cross-check the ‘Cumulative Cash Payment’ history to see if your client qualifies for the Rule 86B(d) exemption.

Where: Total Output Tax > ₹50,000 (on taxable turnover > ₹50L).

The Cumulative Escape Hatch (The Professional’s Secret)

Most practitioners forget Proviso (d) of Rule 86B.

The Strategy: If the taxpayer has discharged more than 1% of their cumulative output tax liability through the electronic cash ledger up to the current month in the financial year, the 1% restriction does not apply.

The Cumulative Verification Formula:

The Cumulative Cash Flow Test

Accountant’s Note: This is the most underutilized tool in GST. If your client had high cash outflows in previous months due to low ITC, use this formula to preserve liquidity in months where they have high ITC.

Audit Tip: In 2026, don’t just look at the monthly return. Maintain a Cumulative Cash-Payment

Don’t let Rule 86B suffocate your startup’s cash flow. If your directors have a solid tax history, you can bypass the 1% cash mandate entirely. Use the official Income Tax Department Portal to verify your historical contributions and unlock this liquidity exemption.

Tracker. If your client paid heavy cash in previous months, they might be exempt from the 1% rule this month, saving immediate liquidity.

2. Rule 37A: The Invisible Reversal Trap

Legal Anchor: Rule 37A (The ITC Reversal Clause).

Rule 37A is the ultimate violation of the Doctrine of Impossibility. It mandates that if a supplier fails to file GSTR-3B by September 30th following the end of the FY, the buyer must reverse the ITC.

Rule 37A creates a unique compliance burden where you are held responsible for your vendor’s filing behavior. To strengthen your legal stand against such system-driven reversals, you must understand the Section 16(2)(c) Survival Guide which uses the ‘Doctrine of Impossibility’ to protect innocent buyers from unfair tax demands.

GST Rule 37A Reversal and Re-availment Law

Caption: Source: CGST Rules (Amended 2024). Note the critical September 30th and November 30th deadlines for ITC reversal.

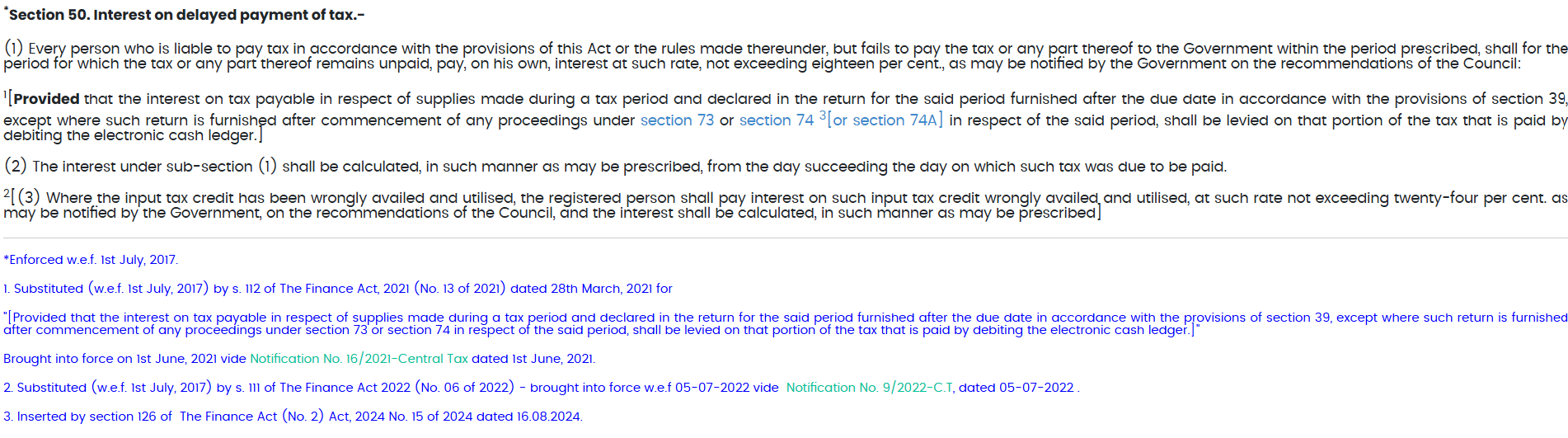

The Minute Doubt: Interest vs. Liability

The biggest debate in 2026 is whether interest is applicable if the ITC was reversed but never utilized.

While Section 50(3) provides a shield for unutilized credit, calculating the exact exposure is key to winning an audit. For a deeper technical breakdown, explore our detailed guide on Rule 37A Defense and Section 50(3) Formulas to learn how forensic calculations can save your business from hefty interest penalties.

GST Interest Liability Section 50(3) Verification

Caption: Source: Bare Act Section 50. This validates that interest applies only to ITC wrongly availed AND utilised .

The Ground Reality: Section 50(3) states interest is only for ITC wrongly availed AND utilized.

The most common doubt my peers ask is—’If we didn’t use the credit, why pay interest?’ My advice is simple: Keep a monthly screenshot of your Electronic Credit Ledger. If your balance never dipped below the reversal amount, you can fight the 18% interest demand using the ‘Doctrine of Impossibility.’ Don’t let the system bully your client into paying for a supplier’s mistake.

The Interest Risk Formula:

Rule 37A: Interest Liability Math

Litigation Shield: If your cash/credit ledger balance always remained higher than the ITC to be reversed, the ‘Days of Over-utilization’ technically become zero. No utilization means no interest!

Note: If Electronic Credit Ledger Balance (ECLB) is always > ITC to be reversed, Interest = 0.

Litigation Defense: If your client always maintained a balance in their credit ledger exceeding the reversal amount, you have a strong case to contest the 18% interest. This is a high-level technical point that saves lakhs for big clients.

The Compliance Shield: Monthly 2B vs. PR Reconciliation

To contest Rule 37A, legal knowledge alone is insufficient; you must possess a robust paper trail. Maintain a monthly reconciliation statement comparing your GSTR-2B with your Purchase Register (PR). Should you receive a notice from the Department in the future, this very statement will serve as your “Defense Document,” proving that you are an “Innocent Buyer” and have exercised complete statutory diligence on your part.

Rule 37A: Reversal & Re-availment Chain

GSTR-2B Check

(Trigger Point)

(Rule 37A)

➔ Re-avail ITC

Statutory Note: Always maintain a screenshot of the GSTR-3B filing status from the public portal before re-availing credit.

3. The 2026 Action Plan for Tax Professionals

To protect your practice, move from Reactive Filing to Proactive Risk Management.

Why is the department moving toward “System-Driven Penalties ? To understand the vision behind these automated blocks, track the latest policy updates on the Press Information Bureau (PIB). Staying aligned with official narratives helps you justify these strict compliance shifts to your clients.

A. The Supplier Risk Rating (SRR) Matrix

In 2026, don’t just rely on GSTR-2B. Implement an internal scoring system for vendors:

| Rating | Vendor Status | Action Plan |

| Green | Files GSTR-1 & 3B on time | Standard Payment Terms. |

| Yellow | Files GSTR-1; 3B delayed | Issue Letter of Non-Compliance. |

| Red | 3B pending > 2 months | Hold GST Component of Payment. |

A high-risk vendor is a direct threat to your ITC. Before you trust a supplier’s GSTR-3B status, verify their legal existence and “Active” compliance status via the Ministry of Corporate Affairs (MCA). Integrating MCA master data into your SRR Matrix is the ultimate move to prevent Rule 37A disasters.

Supplier Risk Score (SRR)

Practical Tip: Integrate this scoring in your monthly review. In 2026, a high SRR score is a leading indicator of an upcoming Rule 37A reversal.

In my practice, we have started adding a ‘GST Clause’ in every purchase agreement. It clearly states that the 18% GST will only be released once the supplier’s GSTR-3B reflects on the portal. It sounds harsh, but in 2026, it is the only way to safeguard your client’s liquidity against Rule 37A.

Pro-Tip: For Red category suppliers, advise clients to hold the GST component of the payment until the 3B filing proof is shared. This is the only way to beat Rule 37A.

B. Drafting the Protective Reversal Note

When reversing ITC under Rule 37A, always add a specific remark in your books: Reversed under Rule 37A without prejudice to the right of re-availment.“This ensures that the Time Limit under Section 16(4) does not haunt you when you eventually reclaim that credit.

4. Advanced F.A.Q. (The Expert’s Corner)

Q1: Can a New Startup avoid the 1% Cash Rule ?

The Harsh Reality: No. Since exceptions require a 2-year history of Income Tax payment (>₹1 Lakh), new businesses with high turnover are unfairly targeted. This is a procedural flaw that CAs must explain to entrepreneurs.

Q2: Is Rule 37A reversal required if the supplier files GSTR-3B after the Nov 30th deadline ?

The Logic: If they file before you reverse, you are safe. If they file after you reverse, you can immediately re-avail it. Use this logic for timing:

Net Liquidity Impact = ITC Reversal Amount x Days or Blockage

Q3: How to handle 86B if the client is an Exporter ?

The Exception: Rule 86B does not apply if the registered person has received a refund of >₹1 Lakh in the preceding FY. Always keep the Refund Sanction Order (RFD-06) mapped with your monthly turnover files.

Once your supplier eventually files their returns, the law allows you to re-claim the reversed credit. To ensure this process doesn’t trigger automated flags, follow the Rule 37A Re-claims (ECRS Math) procedure to avoid ASMT-10 notices and maintain a clean Electronic Credit Reversal and Re-claimed Statement.

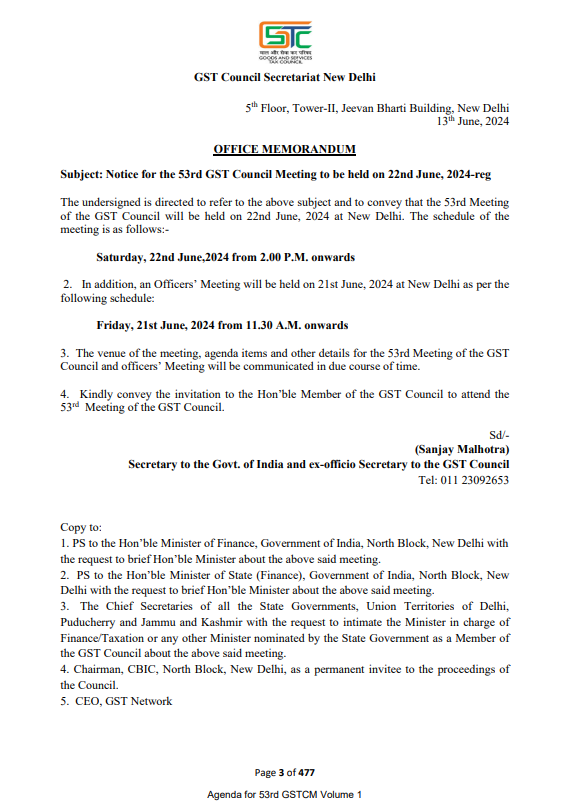

GST Council Secretariat Official Notice 2024

Caption: Source: GST Council Secretariat (gstcouncil.gov.in). Tracking official meeting agendas ensures our strategies stay ahead of system-driven enforcement.

The Working Capital Clog Ratio (WCCR)

Strategic Insight: If your Clog Ratio exceeds 15%, your business is not just paying tax—it is bleeding cash. Use this ratio to justify the need for strict vendor compliance and timely 3B filing to your clients.

Conclusion: Litigation-Proofing your Practice

The shift from Section 16(2)(c) to Rule 86B/37A shows that the department is moving toward System-Driven Penalties.

In 2026, a Smart Professional is not the one who files returns on time, but the one who ensures that their client’s ITC is not sitting as a Dead Entry. Understand the cumulative cash flow, track the vendor’s 3B religiously, and use the Doctrine of Impossibility as your legal shield.

Disclaimer

This guide is for educational purposes for CAs, Advocates, and Tax Professionals. It is based on the 2026 GST framework. Always verify specific facts with the latest GSTN portal updates.

Meet the Expert

Anurag Panchal is a seasoned Digital Marketer and Tech Strategist, widely recognized as the Founder of ServiceMoney.in and AllRoundUpdate.com.

Specializing in simplifying emerging technologies and financial compliance for an Indian audience, Anurag has authored over 135+ technical guides to help more than 10,000+ readers navigate the complexities of GST litigation, Tally Prime automation, and technical SEO.

Through his professional platforms, he focuses on transforming dry statutory laws into formula-driven defense strategies, empowering tax professionals to protect their businesses from automated scrutiny and the ‘Innocent Buyer’s Trap’.

Connect with his expert masterclasses:

- YouTube: @Educationanurag

- Professional Portals: ServiceMoney.in | AllRoundUpdate.com

Legal Disclaimer

Dynamic Nature: GST frameworks for Rule 86B & Rule 37A are based on 2026 interpretations.

Verification: Cross-check with CBIC Notification 94/2020.

“Strategic Insight: For educational use only. Not a substitute for professional advice.”