I’ve spent the last three months watching top-tier CFOs and seasoned CAs scramble because of a single automated email from the GST portal: the Section 16(2)(c) & DRC-01C. We are past the stage of ‘glitches.’ We are now in a ‘Compliance Deadlock’ where the law says one thing, and the algorithm does another. If you think your software-based reconciliation will save you in an adjudication, you are betting your company’s working capital on a false sense of security

I’ve lost count of how many times I’ve woken up to an automated DRC-01C notice on a Saturday night. The GST portal doesn’t care about your holidays, and it certainly doesn’t care about your ‘intent.’ It only cares about the data. We’ve moved from an era of tax compliance into an era of algorithmic warfare

Judicial relief for bona fide taxpayers

Caption :- Explains court’s view on buyer-supplier tax liability. Source: Taxmann 2026.

Don’t gamble with the algorithm. Verify every move you make against the Official GST notifications at cbic.gov.in before you draft your response.

1. The Core Concepts: Why the Deadlock Occurs

The deadlock is a conflict between Section 16(2)(c) (Actual Payment Condition) and the Doctrine of Impossibility (Lex non cogit ad impossibilia).

Understanding ITC conditions Section 16(2)(c)

Caption :– Section 16(2)(c) mandates that ITC is available only when the supplier has discharged tax liability. Source: TaxGuru Analysis on ITC Denial.

- The Buyer’s Passive Victim Concept: A buyer is passive because they cannot force a vendor to file a return. When the system blocks ITC, the buyer is effectively being held liable for the vendor’s financial delinquency—a violation of the principle that a taxpayer should only be responsible for their own compliance.

- The Vendor’s Technical Trap Concept: A vendor becomes a victim when they have discharged liability, but an incorrect HSN code, a portal glitch, or a buyer’s reversal of an invoice leads to a Mismatch Notice, freezing the vendor’s cash flow.

But watch the calendar—even a valid claim dies if you miss the deadline. Don’t let your hard-earned credit vanish into a Permanent ITC lapse timing is everything.

2. The System-vs-Law Conflict: The Bridge Strategy

The portal’s black-box algorithm doesn’t care about your intent; it only cares about the data match. And when that match fails, you become the bank for the tax department.

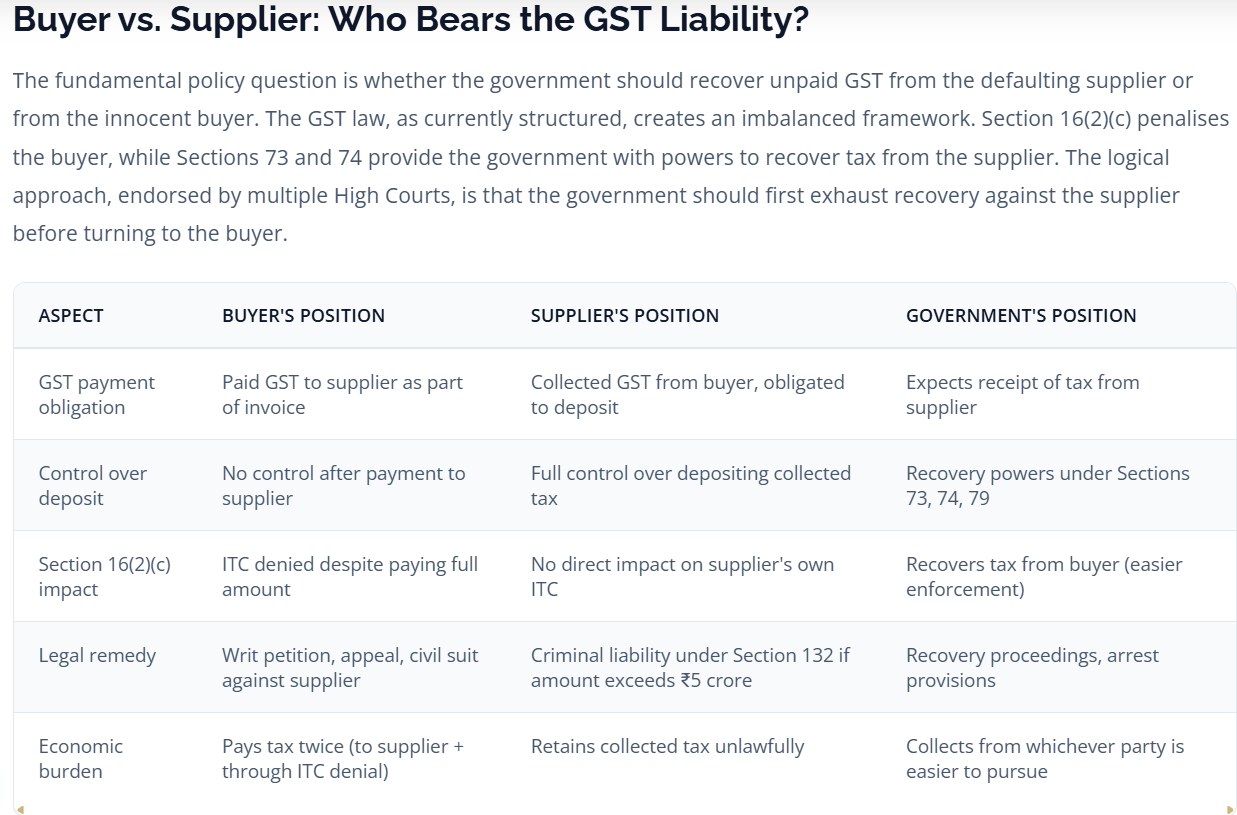

Buyer vs Supplier GST responsibility matrix

Caption :- Highlights the unfair economic burden shift in GST. Source: Legal Compliance Study.

The First Defense Metric:

When you face a notice, first calculate your Mismatch Impact Exposure (MIE):

Maximum Impact Exposure (MIE)

Use this formula to determine if the battle is worth the cost or if it’s a pure Write-off case.

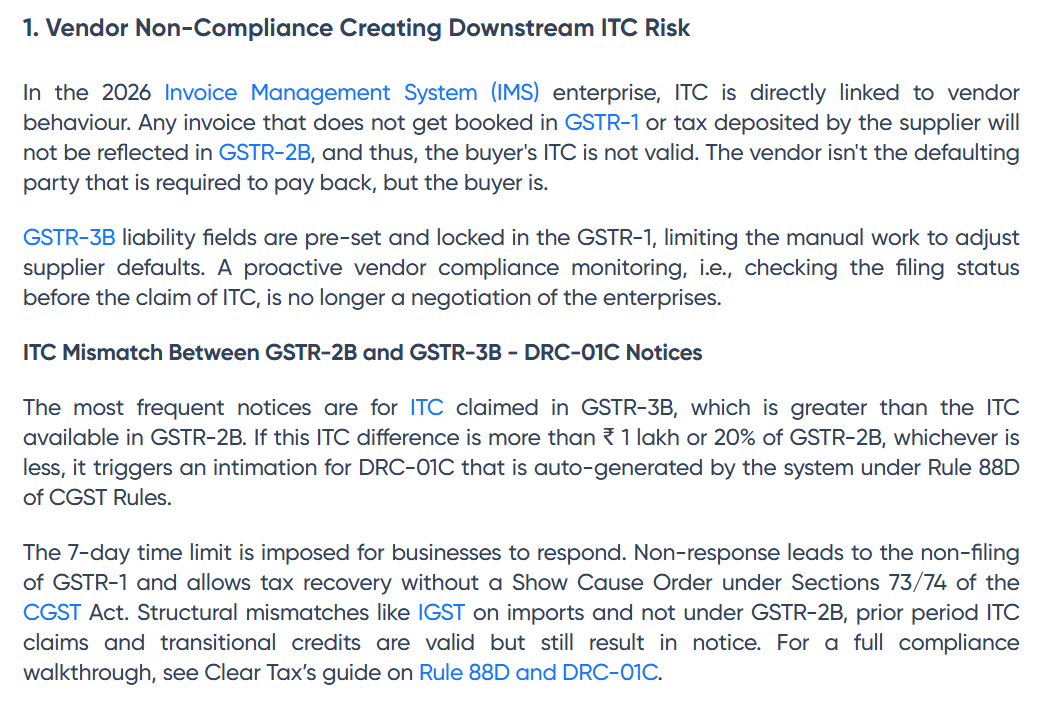

3. The Automated Reconciliation Trap

Many accountants rely solely on software-based GSTR-2B matching. This is a strategic error. Reconciliation identifies the What, but it ignores the Why. Software cannot detect Fake Invoice fraud or Circular Trading patterns.

The portal’s algorithm is relentless. Don’t wait for a notice to arrive—proactively use a Rule 88D strategy to clean your records before the system flags you.

To avoid this trap, apply your Vendor Reliability Score (VRS):

Vendor Reliability Score (VRS)

If VRS < 0.5, your internal audit must flag this vendor for immediate review, regardless of what the software reconciliation says.

Last year, I handled a case where a client had 100% GSTR-2B matching, but the tax officer still demanded a reversal. Why? Because the supplier was part of a ‘circular trading’ ring that the portal didn’t flag until six months later. My software told me we were ‘clean.’ The ground reality was that we were sitting on a ticking time bomb. This is why the VRS (Vendor Reliability Score) isn’t just math—it’s an early warning system that saved my client ₹15 Lakhs in avoidable litigation.

DRC-01C notice triggers under Rule 88D

Caption :- Shows when a mismatch automatically triggers a notice. Source: ClearTax Guidelines.

I’ve seen ‘Green Ticks’ in accounting software lead to ‘Red Notices’ in reality. Software sees a match; it doesn’t see a scam. If you trust the green tick blindly, you’re not doing an audit—you’re just clicking buttons.

IMS Matrix Reconciliation Protocol (IMRP)

STAGE 1: DATA INGESTION Sync GSTR-2B + ERP Ledger. | v STAGE 2: 16(4) FILTER Is date > Sept/Nov cut-off? | ---------+--------- | | (YES) (NO) | | [REVERSAL] [STAGE 3: RECON GATE] Is 2B "Filed"? | -------+------- | | (YES) (NO) | | [ACTIVE] [STAGE 4: ESCROW] Route 3B. Flag & Deduct 10%.

Protocol Note: Automated checks for Section 16(4) compliance & vendor default mitigation via Escrow Lock.

4. The Litigation-Proof Documentation Trail

If you reach the courtroom, you must demonstrate Proactive Vigilance. You aren’t just saying I didn’t know; you are proving that you fulfilled your Commercial Due Diligence.

The Gold Standard Metric: Bona Fide Buyer Index (BFI):

Business Financial Integrity (BFI)

Documentation isn’t just paperwork; it’s a strategic asset. My defense dossiers are built on the same International trade diligence principles used by global firms to justify complex cross-border transactions.

When you present this to an officer, you are objectively proving that you paid the tax and the vendor’s default is an external factor, not collusion.

5. Advanced Case Study: The Phantom Supplier Crisis

- Situation: A firm purchased goods worth ₹20 Lakhs. The supplier filed GSTR-1 but vanished before filing GSTR-3B.

- The Failed Strategy: Reversing ITC under portal pressure.

- The Litigation-Proof Strategy: The firm submitted a Compliance Dossier containing:

- Bank records proving payment.

- Email trails demanding compliance.

- A formal Legal Notice (post-default).

- Due Diligence Sufficiency Ratio (DDSR

- By showing a DDSR > 0.8, the firm proved Due Care, and the officer dropped the demand.

Dispute Documentation Success Ratio (DDSR)

I remember a case where the supplier vanished into thin air. We didn’t have the vendor, but we had the bank trail. That bank statement was the only thing standing between the client and a 100% tax recovery order. It wasn’t the GSTR-2B that saved us; it was the paper trail we kept from Day 1.

6. Advanced Documentation Protocol (Buyer & Vendor)

| Feature | Buyer’s Defensive Strategy | Vendor’s Defensive Strategy |

| Contractual Shield | Include a GST Indemnity Clause in every PO. | Include a Liability Waiver for portal glitches. |

| Evidence | Bank Statement + Email trail of follow-up. | GSTR-2B Reconciliation + Ledger Match. |

| Action | If default persists, stop payments/offset. | If buyer refuses to update, issue legal notice. |

When I present this to a jurisdictional officer, I don’t hand over a pile of papers. I hand over a Dossier. Officers are trained to find holes in your story. This dossier shuts them down because it forces them to look at your evidence, not just the ‘mismatch’ screen.

7. Strategic Pivot: Recovery vs. Write-off

If the vendor is non-traceable, don’t just reverse and accept the loss. Convert this into a Business Loss under the Income Tax Act.

Final Financial Assessment: Recovery Probability (RP):

Recovery Potential (RP)

If RP is low, don’t waste legal fees. Write it off as Bad Debt using the formal Demand Notice as your supporting evidence.

Don’t let your working capital get locked in artificial tax cycles. Learn the legal shortcut to Avoid 1% cash tax payments and keep your business cash flow moving.

8. Actionable Checklist: 5-Point Vendor Risk Assessment (2026 Edition)

- Contractual Indemnity: Ensure every PO includes: Supplier agrees to indemnify Buyer for any loss of ITC resulting from Supplier’s failure to discharge tax liability.

- The 12th-Day Trigger: If GSTR-1 is not filed by the 12th, trigger an automated notification. Log this as evidence.

- The KYC-Plus File: Maintain an annual folder for each vendor: Udyam Certificate, Cancelled Cheque, and GST Registration status.

- Quarterly Sign-off: Have your internal auditor sign a quarterly Reconciliation & Compliance Report. This is your primary shield.

- Evidence Memo: For all disputes, create a digital Compliance Folder containing email follow-ups and bank transaction IDs.

Compliance is a cycle, not a one-time task. To build a robust supply chain, integrate these Tax risk management frameworks into your internal audit to stay ahead of the audit trail.

Vendor’s Compliance Pipeline (LDR)

STAGE 1: LIQUIDITY CHECK (SSC) Calc SSC = Assets / (Liabs + Tax). | v STAGE 2: TRIGGER FILING If SSC < 1.2: Trigger Auto-Draft. | v STAGE 3: PORTAL "HANDSHAKE" Is HSN Mapping correct? -------+------- | | (NO) (YES) | | [RE-VALIDATE] [STAGE 4: AUTO-FILE] Run Mismatch. Confirm 3B Discharge. Issue Certificate.

Pipeline Note: Automated vendor compliance flow ensuring HSN accuracy and timely 3B liability discharge.

Don’t just keep these folders in the cloud; keep them print-ready. When a tax officer walks into your office for an audit, being able to pull that ‘KYC-Plus’ file in 60 seconds completely changes the power dynamic. It tells them: ‘We are prepared, and we aren’t easy targets.

9. The Supplier Liquidity Health Check (The Proactive Filter)

Most businesses focus on compliance history but ignore the supplier’s financial ability to pay GST. A supplier with high turnover but low cash reserves is a structural risk.

Financial solvency calculation for vendors

Caption :– Formula to assess a vendor’s ability to discharge tax. Source: Financial Accounting Standards.

Concept: The Supplier Solvency Coefficient (SSC)

Integrate this into your vendor onboarding. If a vendor is cash-strapped, they will prioritize operational payments (wages, rent) over tax remittances.

Statutory Solvency Coverage (SSC)

- Strategic Application: If a vendor’s SSC < 1.0, do not offer advance payments. Link your payment terms to the actual reflection of tax in GSTR-2B, rather than just the receipt of the invoice.

10. The Automated Reconciliation (The Dynamic Buffer)

You rightly noted that software-based reconciliation is a strategic error. We must evolve this into a Reconciliation-as-a-Service (RaaS) Protocol.

- The Delta Log: Maintain a real-time Delta Log of all invoices where GSTR-1 reflects, but 3B is delayed.

- The Compliance Credit Strategy: Instead of just flagging, use your procurement software to trigger an automated Escrow Lock on 10% of the invoice value for vendors who consistently cross the 15th-day threshold. This provides the exact liquid cash needed to pay the tax if you are forced to reverse ITC later.

11. The Judicial Precedent Mapping (The Legal Anchor)

Your manual should explicitly distinguish between Procedural Lapses and Substantive Compliance.

- The Substantive Principle: Courts (including the Supreme Court in Bharti Airtel) have often held that the electronic credit ledger is a reflection of the taxpayer’s entitlement.

- The Concept of Input Tax Ownership : Treat ITC not as a grant by the government, but as a vested property right once the goods/services are received and payment is made to the vendor. Your defense strategy must shift the burden of proof back to the department by asking: Has the tax reached the exchequer ? rather than Did the vendor file?

Arise India vs Commissioner of Trade Taxes case

Caption :- Establishes the ‘bona fide purchaser’ immunity principle. Source: Delhi High Court Archives.

12. The Tax-Indemnity Insurance (Financial Hedging)

For critical vendors who are high-risk but indispensable (e.g., sole-source manufacturers), traditional indemnity clauses are often toothless if the vendor goes bust.

- Concept: The GST Security Deposit (GSD):Introduce a formal GST Security Deposit clause in master service agreements for high-value contracts. A sum equivalent to 5% of the annual transaction value shall be held as a GST Security Deposit, refundable upon the successful reconciliation of the final annual return (GSTR-9) and validation of no outstanding tax liability.

- Why it works: It acts as a financial hedge against the MIE (Mismatch Impact Exposure) you calculated earlier.

13. Updated Strategic Framework: The 3-Layer Defense

| Layer | Focus | Key Metric |

| I. Onboarding | Vendor Financial Health | SSC (Solvency) |

| II. Operational | Real-time Reconciliation | VRS (Reliability) |

| III. Litigation | Evidence Documentation | DDSR (Due Diligence) |

14. Refined Actionable Checklist Addition:

- The Zero-Tax Payment Clause: Explicitly mention that payment of the GST component of an invoice is subject to its reflection in the GSTR-2B. This provides the legal basis to withhold payment legally until the tax is actually paid to the government.

- The Audit Trail Repository: Move beyond paper files. Use a WORM (Write Once, Read Many) cloud storage for all GSTR-2B snapshots and email communication. A digital timestamp is more credible to an officer than a printed invoice.

Strategic Question for you: Given the complexity of these protocols, are you looking to implement these as internal SOPs for your firm, or are you looking to develop these into a standardized contract addendum to be sent to all your existing vendors?

Example:

Look, I’ve seen many businesses spend ₹2 Lakhs in legal fees to fight an ITC mismatch of ₹50,000. That’s ego, not strategy. You need to know when to fold. The ‘3-Minute Decision Matrix’ below is what I personally use in my office before I tell a client to fight a notice or to just cut their losses and write it off. Use it to keep your sanity and your cash flow intact.

The 3-Minute Decision Matrix for Notices:

- If MIE < Cost of Legal Representation: Pay the tax (with protest) and claim as Business Loss.

- If MIE > Cost of Legal Representation AND DDSR > 0.8: Initiate Formal Adjudication.

- If MIE > Cost of Legal Representation AND DDSR < 0.5: Negotiate settlement with vendor/supplier or write off as bad debt.

FAQ

Q1:Does Due Diligence actually stop a DRC-01C notice?

It provides the legal foundation to get the notice dropped during the adjudication phase, preventing the need for costly litigation.

Q2: Can a small accountant use these formulas?

Yes. These formulas turn subjective arguments into objective reports. An officer is much less likely to argue against a DDSR report backed by real bank-validated documents.

Q3 : If my vendor is non-traceable, does the bank payment trail save me?

Yes. Under the doctrine of bona fide purchase, if you can prove payment through formal banking channels and demonstrate Due Diligence (via DDSR), you build a strong defense. Courts have frequently ruled that a buyer cannot be penalized for the supplier’s subsequent delinquency.

Q4 : Does the “Reconciliation-as-a-Service” (RaaS) Protocol require expensive software?

No. RaaS is an operational discipline, not just a software tool. It focuses on the process of GSTR-2B validation, timely vendor alerts, and documented evidence storage. It can be implemented using standard ERPs and systematic manual compliance logs.

Disclaimer

This manual is for strategic and educational purposes only. GST law is complex, subject to frequent updates, and open to interpretation based on jurisdictional nuances. The methodologies, metrics, and formulas shared here are for educational purposes only and should not be considered professional legal or tax advice. Always consult with your tax advisor or legal counsel for case-specific representation

Anurag Panchal

Founder & Chief Editor of ServiceMoney.in & AllRoundUpdate.com.

Architect of IMS Matrix Reconciliation & Vendor Compliance Pipeline (LDR).

Specializing in automated ITC protection, financial shield integration, and liquidity risk mitigation.

Stay ahead: @Educationanurag.