For investors, founders, and legal counsel, the GST landscape has shifted from a mere filing exercise to a valuation-critical risk. Mastering GST Section 16 & IMS Rules is now essential, as the new Invoice Management System (IMS) integration with GSTR-2B has fundamentally altered the Input Tax Credit (ITC) lifecycle. If you view this as just an operational accounting update, you are likely missing a silent erosion of your company’s EBITDA and cash flow.

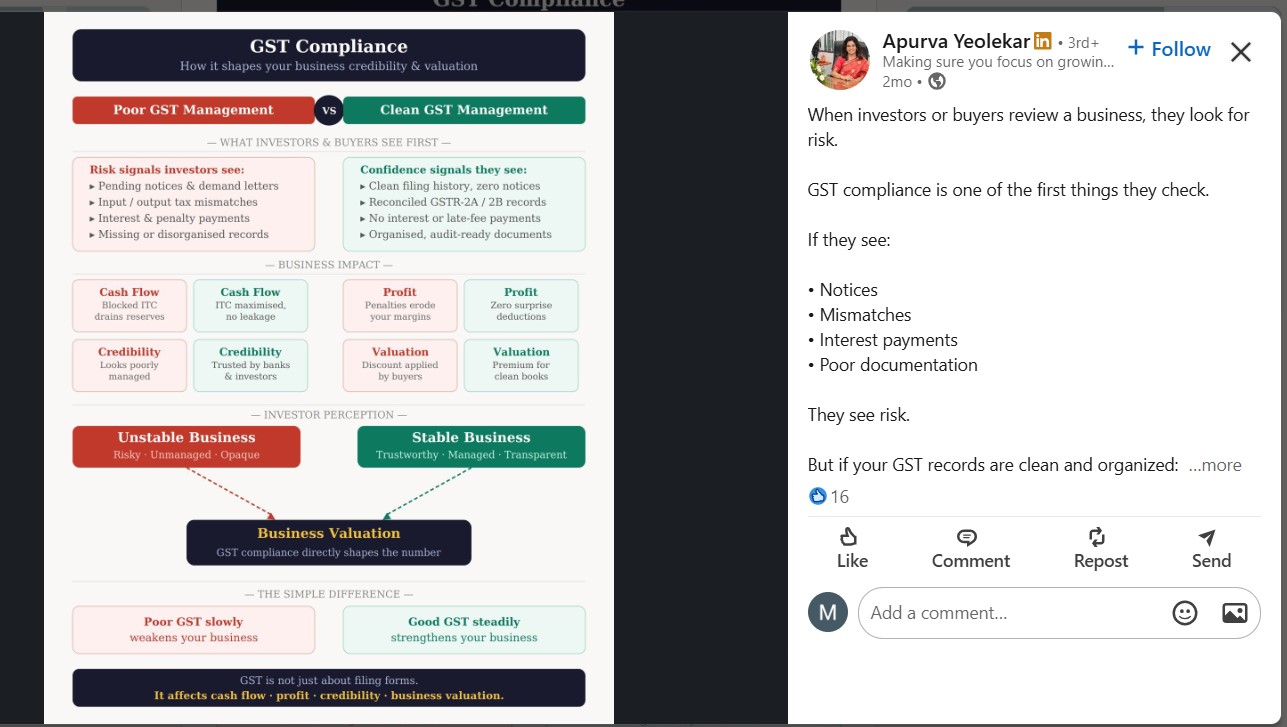

GST Compliance and its impact on Business Valuation

Caption :- A comparative matrix demonstrating how meticulous GST compliance builds investor confidence and improves overall business valuation.

I remember a recent audit defense session where we lost nearly 15% of our ITC just because an automated system sync failed on the 11th of the month. The vendor was compliant, the invoice was valid, but our ‘Accept’ status was missing. That night, I realized that we weren’t just losing tax credit; we were bleeding EBITDA. That was the ‘Aha!’ moment that led us to build the Vendor Health Firewall.

Investors don’t buy companies; they buy ‘Risk-Free’ growth. Discover the Strategic Value of Compliance in today’s M&A landscape.

The Compliance-Valuation Gap: Methodology to Valuation Multiples

In the eyes of a PE/VC investor or a banker, Compliance Quality = Risk Premium.

When conducting due diligence, an investor does not just look at your top-line; they look at the quality of your cash flows. ITC is essentially a cash-flow asset. If your GSTR-2B-IMS reconciliation is flawed, you aren’t just facing a tax demand; you are suffering a Valuation Haircut.

The Formula:

If your ITC reconciliation efficiency is denoted by η (where η < 1), the impact on your valuation V can be expressed as:

Adjusted Valuation Model

Where:

- • M = Valuation Multiple.

- • ΔITCreversal = Disallowed ITC due to non-acceptance in IMS.

- • r = Risk-adjusted discount rate.

The Problem: Because the system is now automated, a failure to Accept an invoice in IMS before the GSTR-3B filing deadline results in an automatic system-driven denial of credit. This creates an immediate Compliance Gap that impacts working capital, forcing founders to pay cash taxes despite having the underlying input tax invoice.

The Anatomy of the ‘GSTR-2B-IMS’ Trap

We’ve all been there—the portal is lagging, the API is throwing 500-errors, and the 3B deadline is just 48 hours away. In that high-pressure window, clicking ‘Accept’ on 500+ invoices feels like a game of Russian Roulette. I’ve seen seasoned finance teams crumble under this manual pressure. This isn’t just about GST; it’s about the sheer anxiety of knowing that a single missed click today equals a tax notice three years down the line.

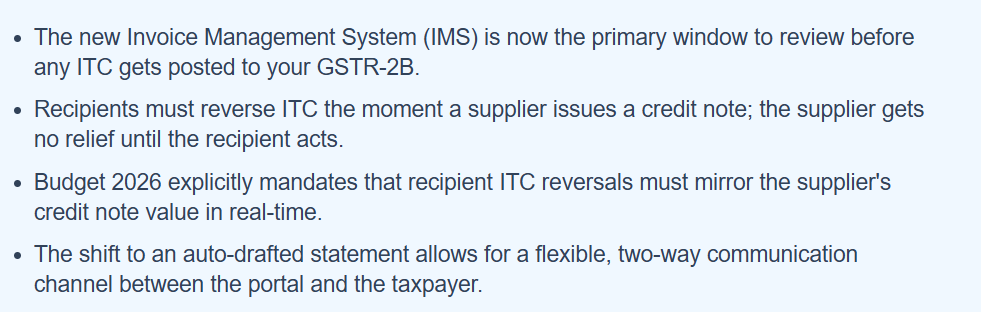

GST Invoice Management System Workflow Guide 2026

Caption :- Source Official GSTN advisory on IMS operational mechanics.

The Compliance Data Chain

💡 Key takeaway: Modern compliance is iterative. Missing the ‘Decision Gate’ (Stage 3) is the primary cause of automated ITC loss.

The Core Problems (and their Legal Realities):

- The Ghost Reversal Effect: If a vendor files GSTR-1, but the system doesn’t sync it with your IMS, and you miss the manual intervention, the ITC is parked in a limbo state.

- Section 16(2) Compliance Hurdles: You may possess the invoice (Section 16(2)(a)), but if the IMS status is not ‘Accepted,’ the department’s automated scrutiny modules will flag the ITC as non-compliant under Section 16(2)(aa).

- Vendor Non-Compliance Cascading: If your vendor files an amendment in GSTR-1, the IMS requires a re-acceptance. If missed, the system rolls back the ITC, triggering interest under Section 50(3) @ 18% p.a.

- The legal reality of IMS is that missing a deadline isn’t just a tax delay—it’s an invitation to a DRC-01C notice. Don’t wait for the department’s automated trigger; master your Audit Defense today before the scrutiny starts.

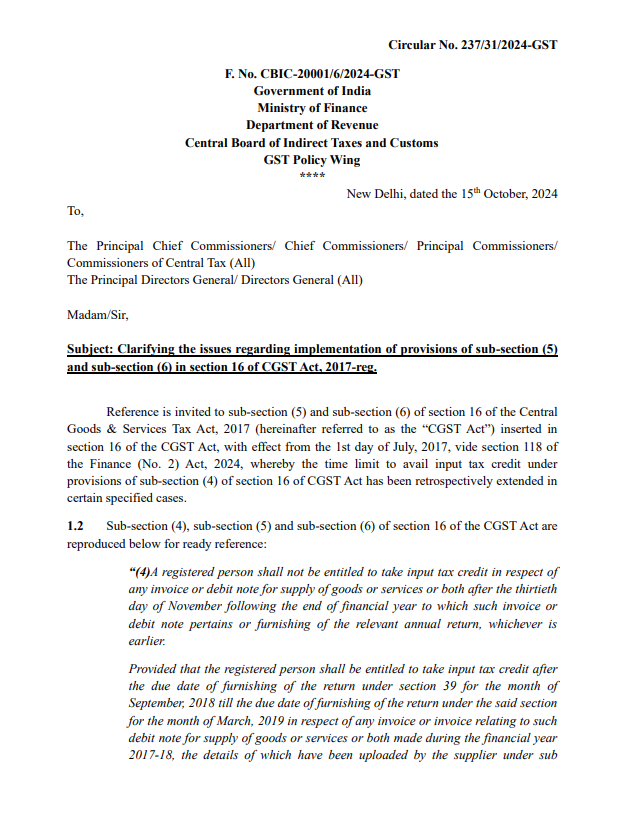

CBIC Circular 237/2024 GST Section 16 Clarification

This official CBIC circular provides the legal framework for resolving historical ITC disputes and retroactive eligibility under Section 16(5) and 16(6)

Quantitative Impact: A Case Study

Imagine a SaaS company with a monthly turnover of ₹5 Crores and an average monthly GST ITC of ₹50 Lakhs.

- Scenario: Due to an internal process gap, 10% of invoices are not ‘Accepted’ in the IMS within the statutory window due to vendor reporting errors and lack of follow-up.

- The Calculation:

- Monthly ITC Loss: ₹5 Lakhs.

- Interest (Section 50(3)): ₹5,00,000 * 18% * (Avg 3 months delay) = ₹22,500 per month.

- Annual Cash Impact: ₹60,00,000 (Blocked ITC) + ₹2,70,000 (Interest cost).

- Valuation Impact: If the company is trading at a 5x EBITDA multiple, the loss of ₹60 Lakhs in annual cash flow results in an effective valuation reduction of ₹3 Crores.

Tax errors aren’t just accounting glitches; they are operational risks. Benchmarking your processes against Global Risk Frameworks is the only way to safeguard your EBITDA.

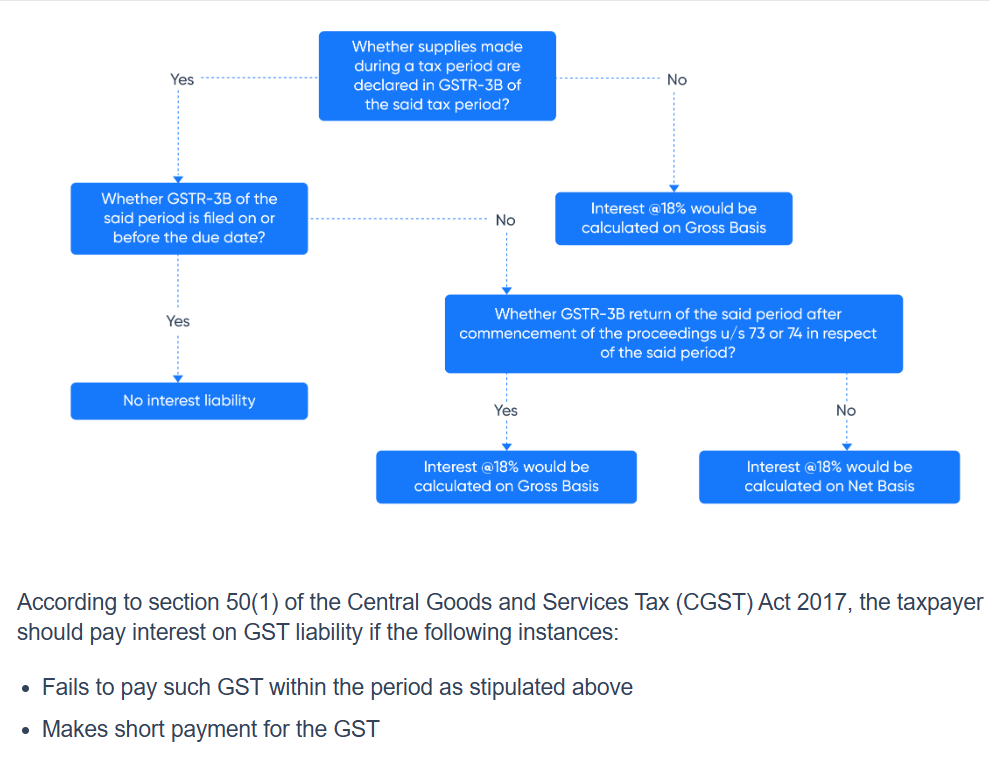

GST Section 50 Interest Liability Calculation Flow

Caption :- A clear guide on interest liability calculation at 18% p.a., distinguishing between gross and net basis based on return filing status

The ‘Vendor Health’ Firewall: A Legal & Operational Solution

To build a preemptive defense, move away from reactive accounting. Implement these four pillars:

Rule 88D is the silent killer of ITC. Our internal data proves that proactive IMS monitoring is the only way to avoid the Rule 88D trap. Build your defense before the portal forces a reversal.

1. The IMS-Sync Contractual Clause

Revise all vendor contracts to include a GST Compliance Clause.

- Legal Language: Vendor must ensure that the invoice is reflected in GSTR-2B within 72 hours of upload. Failure to rectify mismatches within 5 days of notice constitutes a material breach.

2. The 3-Tier Reconciliation Protocol

- T1 (System Match): Real-time automated API sync between ERP (SAP/Tally/Zoho) and GST Portal.

- T2 (The ‘Accept’ Rule): Mandatory weekly Acceptance cycle in IMS. Do not wait for the month-end.

- T3 (The Discrepancy Escrow): Withhold the GST component of the payment to the vendor if the invoice does not reflect in IMS by the 10th of the following month.

THE IMS MATRIX RECONCILIATION PROTOCOL (IMRP)

Swipe Left ⬅️Right➡️ Explore Full Compliance Blueprint

+------------------------------------------------------------------------------------------------------------------------+ | ARCHITECTURAL COMPLIANCE BLUEPRINT | +------------------------------------------------------------------------------------------------------------------------+ | | | STAGE 1: DATA EXTRACTION (INPUT LAYER) | | Sync JSON API Data from GST Portal (IMS) + Internal Purchase Ledger (ERP). | | Execution Triggers: Day 2, 5, and 9 of the month. | | | | | v | | STAGE 2: LOGIC GATE (FILTER LAYER) | | Validation of Statutory Time-Limit (Section 16(4) Compliance Engine): | | Check: [Current Date] vs [Invoice Date] proximity to Nov 30th cutoff. | | | | | +-------------------------------+-------------------------------+ | | | | | | | v (YES: DEADLINE RISK) v (NO: WITHIN TIMELINE) | | STAGE 3A: PRE-EMPTIVE BLOCKADE STAGE 3B: OPERATIONAL VALIDATION | | Action: Enforce Hard Portal Reject. Action: Trigger 3-Tier Match (PO/GRN/Invoice). | | Compliance Logic: Eliminate risk Compliance Logic: Validate underlying | | of reversal/interest. procurement truth. | | | | | | +---------------+---------------+ | | | | | v | | STAGE 4: DECISION MATRIX (ESCROW LAYER) | | Is GRN Missing or Vendor Status = 'Non-Filer'? | | +---------------+---------------+ | | | | | | v (YES) v (NO) | | Route to Discrepancy Escrow. Route to Active ITC Claim. | | (Hold GST Component Payment). (System Ready for GSTR-3B Push). | | | | v | | STAGE 5: AUDIT DEFENSE (OUTPUT LAYER) | | Generate Electronic Audit Trail (EAT). | | Compliance Logic: Stores logs of 'Accept'/'Reject' actions for 8-year scrutiny proof. | | | +------------------------------------------------------------------------------------------------------------------------+

This framework is designed to move your finance function from ‘Reactive Tax Filing’ to ‘Proactive Compliance Architecture

3. Utilizing Rule 37A for Pre-emptive Reversals

If you have claimed ITC but the vendor has not filed GSTR-3B (and thus not paid tax), the system will force a reversal.

- The Proactive Fix: If your dashboard shows a vendor as Non-Filer for two consecutive months, trigger a system-automated reversal to avoid the penalty under Section 50.

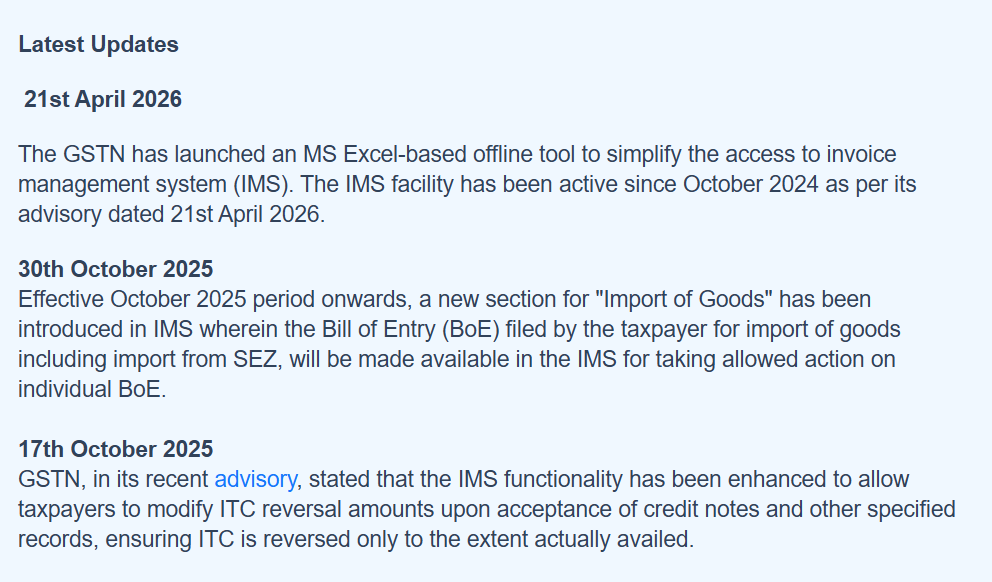

Latest IMS Updates and Rule 37A Compliance Advisories

Caption :- A compilation of the latest GSTN functional updates and Rule 37A requirements, ensuring your business stays ahead of regulatory changes

4. The Valuation Protection Formula (Metric)

Monitor your Compliance Efficiency Ratio (CER):

Compliance Efficiency Ratio (CER)

Target: Maintain CER > 98%. Anything below 95% triggers an automatic audit by the CFO.

ITC is liquid cash. Don’t let compliance bottlenecks freeze it. Here’s how leaders optimize Working Capital Liquidity to fuel growth.

The Supplier Risk Rating Matrix (New Section)

Instead of treating all vendors equally, implement a risk-based categorization. This shows investors that you have a mature internal control environment.

| Risk Tier | Profile | Impact on Cash Flow | Mitigation Strategy |

| Tier 1 (Elite) | Consistent filer, zero errors | Nil | Auto-Accept rules in ERP. |

| Tier 2 (Latency) | Files late, often misses deadlines | High Working Capital Risk | Hold payment until IMS sync. |

| Tier 3 (Chronic) | Non-compliant, frequent amendments | High Tax Liability Risk | Terminate contract or 100% GST-deduction at source. |

- Calculation Logic: Assign a Vendor Reliability Score (VRS) based on:

Vendor Reliability Score (VRS)

| Date | Action Item | Responsibility | Tool |

| 5th | Reconciliation of 2B vs Purchase Register | Finance Manager | ERP/API Tool |

| 10th | Flagging Non-compliant / Missing Invoices | Finance Manager | Vendor Portal |

| 12th | Final IMS Acceptance & Error Logging | CFO | GST Portal |

Advanced Performance Metrics for CFOs & Founders

Compliance is no longer just a post-facto audit requirement; it is a critical operational KPI. To maintain a zero-leakage finance function, founders and CFOs should monitor the following performance metrics:

1. ITC Utilization Velocity (IUV)

This metric measures the speed and efficiency with which your finance team locks ITC in the IMS to ensure zero working capital blockage.

ITC Utilization Velocity (IUV)

- Target: > 0.95 (Minimum 95% efficiency).

- Strategic Insight: If your IUV falls below this threshold, your working capital cycle is artificially slowed down. You are essentially paying cash taxes to the government that you should have offset with your input tax credits, directly hurting your monthly cash flow.

2. Vendor Compliance Risk Score (VCRS)

This is the mathematical backbone of your Supplier Risk Rating framework. It quantifies the operational friction caused by your supply chain.

VCRS Index

- Strategic Insight: The VCRS provides a clear, data-backed justification for any Payment Holds. A high VCRS identifies Chronic vendors who require immediate contract renegotiation or termination. Investors value this metric as it demonstrates that your procurement and finance teams are actively managing risk rather than just reacting to it.

2. Advanced Case Study: The Vendor Amendment Paradox

- The Scenario: You accept an invoice in Month 1 for ₹10 Lakhs + ₹1.8 Lakh GST. In Month 2, the vendor files a credit note or an amendment in GSTR-1, reducing the value to ₹8 Lakhs + ₹1.44 Lakh GST.

- The Trap: If you don’t monitor the Amendment tab in the IMS specifically, you will continue to carry the original ₹1.8 Lakh ITC in your GSTR-3B.

- The Consequence: The system eventually flags the difference, leading to an ineligible ITC claim + interest at 18% + penalty of 10% of the tax amount (under Section 73/74) if deemed a deliberate evasion.

- The Solution: Implement a Variance Reconciliation Report that triggers an alert the moment a vendor status changes from ‘Accepted’ to ‘Amended’ in the GST portal.

3. Data-Driven Compliance: The Hidden Leakage Audit

When I first proposed the transition to API-driven automation, the board was hesitant about the upfront cost. But I argued that we weren’t paying for ‘software’; we were paying for ‘peace of mind’ and ‘valuation integrity.’ Looking back, the biggest gain wasn’t just the ₹8.4 Lakhs saved—it was the fact that my team could finally focus on financial strategy instead of playing ‘match-the-invoice’ every month.

- Case Study Example: An e-commerce firm with 500 vendors spends 40 man-hours per month manually matching 2B to IMS.

- Calculation:

- Cost of Finance Team (Hourly): ₹1,500.

- Monthly Compliance Cost: ₹60,000.

- Annual Operational Burn: ₹7,20,000.

- The Strategic Fix: Investing in an API-driven automated reconciliation tool costs ~₹1.5 Lakhs/year.

- ROI Calculation: By switching from manual to automated, you save ₹5.7 Lakhs annually, plus eliminate the ~₹2.7 Lakhs interest risk identified earlier. Total Annual Value Addition: ₹8.4 Lakhs.

4. Legal Safe Harbor Clauses for Contracts

It changed the way our vendors viewed us. We moved from being a client who ‘follows up’ to a client who ‘enforces compliance.’ Trust me, when your vendor knows that your MSA has teeth, their GST reporting suddenly becomes remarkably accurate.

The Vendor agrees to indemnify the Company for any loss of Input Tax Credit, including applicable interest and penalties under the CGST Act, 2017, arising directly from the Vendor’s failure to report, incorrectly report, or delay in reporting invoices in GSTR-1/IMS. The Company shall be entitled to set off such losses against any future payments due to the Vendor.

FAQ: Addressing the Unspoken Concerns

Q1: Can we claim the ITC later if we missed the IMS ‘Accept’ window?

Legally, while you have a window under Section 16(4), you can claim ITC up to the 30th of November of the following year. However, the system is designed to create a reversal notice immediately. You will have to fight a legal battle to prove the credit was valid, which is a drain on resources.

Q2: Does the IMS status override the physical invoice?

In the eyes of the current automated assessment modules, Yes. Even if you have the physical invoice, without the ‘Accepted’ status in the IMS, the system treats the ITC as non-existent.

Q3: How do we handle vendors who are perpetually late?

Use the Withholding Tax mechanism on the GST component. Legally, the vendor cannot claim interest if the contract explicitly states that payment is contingent upon successful GST reflection

Compliance isn’t a one-time task; it’s a structural necessity. For a deeper dive into preventing automated notices, explore our Litigation-Proof Manual to shield your firm from future GST litigation.

Conclusion

The GSTR-2B-IMS trap is not a technical glitch; it is a structural change in how the tax department verifies the chain of tax payment. For founders and investors, this is now a core operational metric. Building a Vendor Health Firewall is no longer optional—it is a prerequisite for maintaining your company’s valuation integrity.

Stop viewing compliance as a post-facto audit requirement. View it as a real-time cash management strategy.

Disclaimer: This blog is for informational purposes and does not constitute legal or tax advice. The GST laws are subject to frequent amendments by the GST Council. Please consult with your tax counsel or Chartered Accountant before implementing changes to your financial workflows or contracts.

Anurag Panchal

Founder & Chief Editor of ServiceMoney.in & AllRoundUpdate.com.

Strategic architect of IMS Reconciliation Frameworks and Litigation-Ready Compliance Blueprints.

Focused on converting complex tax laws into actionable, risk-free automated systems for business owners.

Deep-dive insights: @Educationanurag.