Managing GST ASMT-10 Risks Professional Rule 42 & 43 approach to ensure total compliance. Most accountants are good at claiming ITC, but very few know how to handle reversals correctly. If you’ve recently noticed a GST ASMT-10 in your dashboard, it’s likely because of a tiny error in Table 4 of GSTR-3B. With the 2026 ECRS rules, the GST portal is now smarter than ever. Let’s look at how to protect your business from unnecessary notices using this professional Rule 42 & 43 strategy.

GST ASMT-10 Risks: Professional Rule 42 & 43 Strategy Map

With the Electronic Credit Reversal and Re-claimed Statement (ECRS) now fully active in 2026, the GST portal tracks every rupee you reverse. One wrong entry in Table 4 of GSTR-3B can trigger a system-generated notice faster than you can say “Audit.” This guide dives deep into the high-stakes world of Rule 42 and 43, providing the exact formulas, real-world examples, and reporting strategies that most blogs skip

1. The “Common Credit” Dilemma: Why Rules 42 & 43 Matter

Most businesses don’t just sell taxable goods. They might have bank interest (Exempt), sell raw materials (Taxable), and occasionally use the office car for personal trips (Non-business).

When you buy an asset or service used for both taxable and exempt purposes, it is called Common Credit. By law, you cannot keep the full ITC. You must reverse the portion related to exempt supplies and personal use.

- Rule 42: Governs Inputs and Input Services (e.g., Rent, Audit Fees).

- Rule 43: Governs Capital Goods (e.g., Machinery, Computers).

Calculating common credit is the first step toward safety. However, a small mismatch between your 2B and 3B can lead to severe warnings. To stay fully protected, you should check our GST 2026 Guide on Avoiding DRC-01C Notices to optimize your tax compliance using AI logic.

2. How to Calculate Your Reversals: The Pro-Accountant’s 10-Step Workflow

To ensure your GSTR-3B is 2026-compliant, you must follow the precise computational chain defined in the CGST Rules. To gain the trust of a CA, you cannot just look at the final figure; you must categorize the pool.

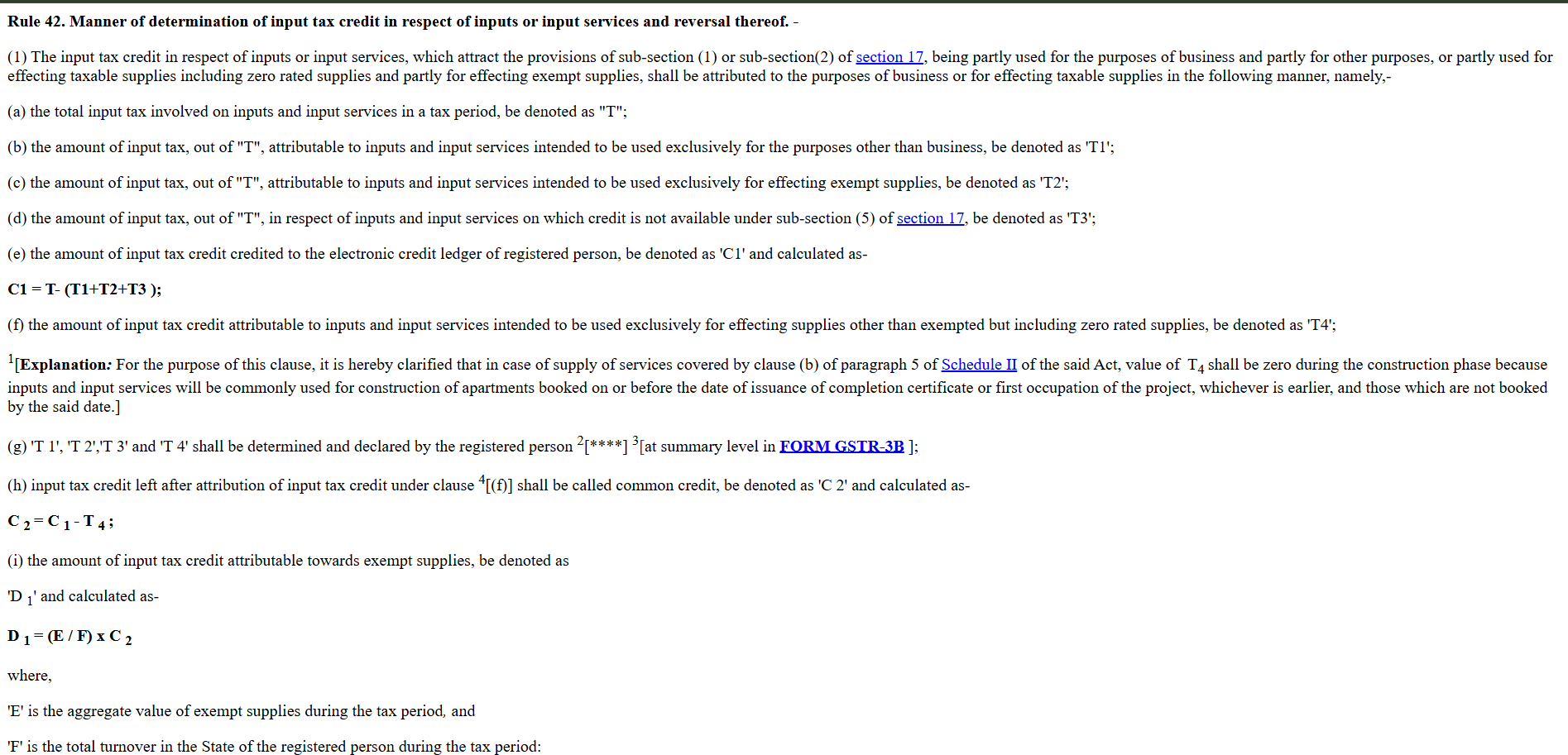

Rule 42 Official Law Extract

Caption : Official Legal Provision: Extract of Rule 42 from the Government’s Tax Information Portal.

For precise legal compliance, it is always recommended to verify the statutory language. You can read the official text directly from the CBIC GST Rules Portal to ensure your data matches the government’s latest gazette.

Verification Note: The above extract is sourced directly from the Central Board of Indirect Taxes and Customs (CBIC). It confirms the specific categorization of T_1 to T_4 that we have simplified in our 10-step guide. Aligning your accounting software with these official symbols ensures that your audit trail remains clean and legally defensible.

The Input Tax Pool Identification

Step 1: Start by pulling your GSTR-2B data…” to “First, log into your portal and download your GSTR-2B. This total number is your starting point (T).” * Why? Mentioning “logging into the portal” adds a layer of real-world experience.

Before applying any reversal formulas, ensure that your purchase register is perfectly matched with your portal data. If you find this process difficult, you can use our latest tool for Smart Excel GSTR-2B Reconciliation Automation to stop any potential ITC loss instantly.

Step 2: Specific Reversals (T_1, T_2, T_3) Before reaching “Common Credit,” eliminate what is clearly non-creditable:

- T_1: ITC for exclusively Non-Business purposes.

- T_2: ITC for exclusively Exempt Supplies.

- T_3: Blocked Credits under Section 17(5) (e.g., Health insurance, Food).

Step 3: Calculating Net Eligible Credit ($C_1$)

The Common Credit Engine

Step 4: Exclusive Taxable Credit (T_4) Identify ITC used only for taxable sales (e.g., raw material for GST goods).

Step 5: Defining Common Credit (C_2) This is the “Grey Area” pool that requires reversal formulas.

Step 6: The Exempt Proportion Reversal (D_1)

(Where E = Exempt Turnover and F = Total Turnover in the State)

Basically, this formula is just finding the percentage of your sales that were exempt and applying that same percentage to your common tax credit. It’s simpler than it looks.

Step 7: The Deemed Personal Reversal (D_2) Govt assumes a 5% personal use for common business expenses.

Step 8: Final Eligible Credit (G) The actual amount that stays in your ledger.

3. Real-World Strategy: The “Mixed-Supply” Proof

Scenario: Anurag Solutions has a total ITC (T) of ₹5,00,000.

- T1 (Personal): ₹10,000

- T2 (Exempt Goods): ₹40,000

- T3 (Section 17(5)): ₹50,000

- T4 (Taxable Raw Material): ₹2,00,000

- Exempt Turnover: ₹20,00,000 | Total Turnover: ₹1,00,00,000

The Calculation:

- C_1 (Net Eligible): 5,00,000 – (10,000 + 40,000 + 50,000) = ₹4,00,000.

- C_2 (Common Credit): 4,00,000 – 2,00,000 = ₹2,00,000.

- D_1 (Exempt Reversal): (20L / 100L) \times 2,00,000 = ₹40,000.

- D_2 (Personal Reversal): 5\% \text{ of } 2,00,000 = ₹10,000.Total Reversal for Table 4(B)(1): ₹50,000 (D_1 + D_2) + Specifics (T_1+T_2+T_3).

4. Rule 43: The 60-Month Capital Goods Commitment

Unlike inputs, Capital Goods are expected to last for 5 years. You don’t reverse the whole amount at once.

Step 9: Monthly ITC Identification (T_m)

Capital goods reversal involves complex 60-month tracking. If you need a deeper technical analysis on industry-specific scenarios, check out this research guide on Rule 43 by Taxmann for expert clarity.

Step 10: The Monthly Reversal Apply the (E/F) ratio to T_m every month for the next 60 months. If you sell the asset early, you must pay back the proportionate ITC for the remaining months or tax on the sale value, whichever is higher.

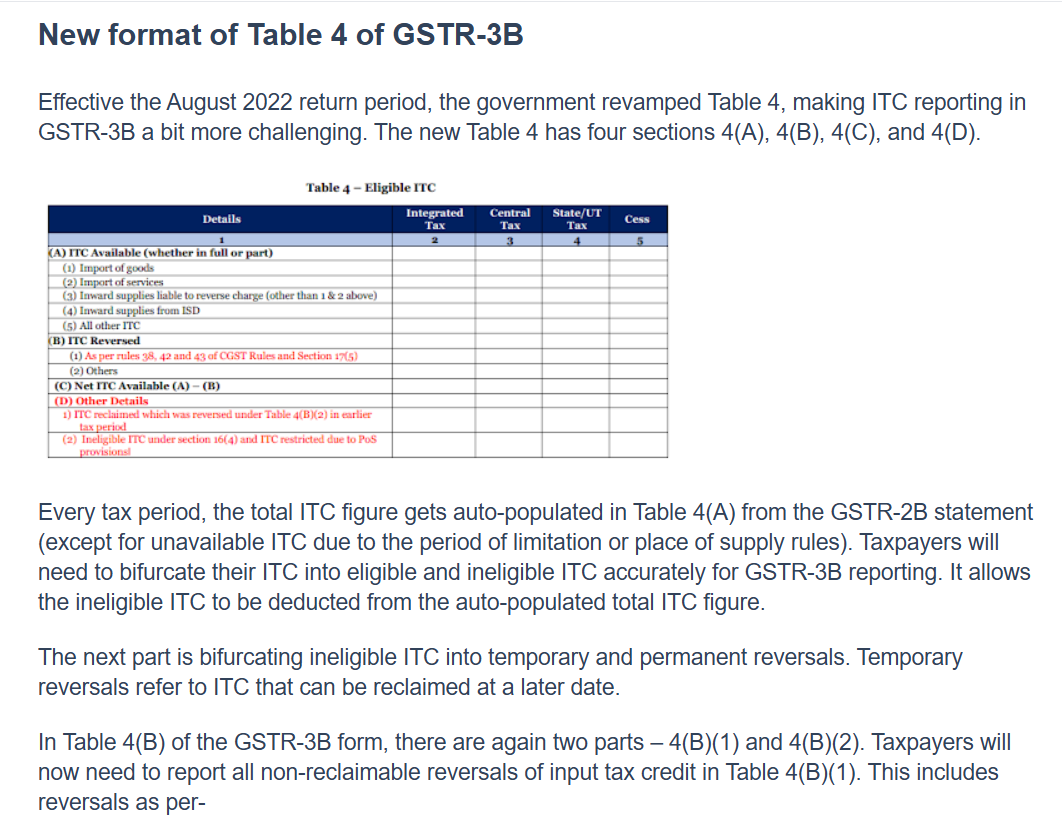

5. The 2026 Reporting Framework: GSTR-3B Table 4

Here is a tip that saves my clients a lot of trouble: When you re-claim credit in 2026, don’t just fill Table 4(A)(5). You must mention it in Table 4(D)(1) as well. If you don’t, your ECRS ledger will show a negative balance, and you’ll get an automated warning from the GST system. It’s a double-entry, but it’s mandatory for a clean record.

Evolution of Table 4: Why the 2026 Reporting is Different.

| Reporting Category | Old Format (Pre-2022) | New Format (Current) |

|---|---|---|

| Ineligible ITC (17/5) | Reported in Table 4(D) | Reported in Table 4(B)(1) |

| Rule 42 & 43 Reversal | Reported in Table 4(B)(1) | Reported in Table 4(B)(1) |

| Temporary Reversals | Not clearly bifurcated | Reported in Table 4(B)(2) |

| Reclaimed ITC | Not separately tracked | Reported in Table 4(D)(1) |

Even with careful reporting, the GST portal might flag old entries for scrutiny. If you have received a notice regarding past mismatches, don’t panic. We have prepared a complete AI-Drafting Guide & Templates for GST ASMT-10 Replies to help you respond professionally.

Rule 42 & 43: The Strategic Guide to ITC Reversal & Re-claim (2026 Edition)

Caption : Official GSTR-3B Table 4 Reporting Map: A step-by-step guide for Rule 42 & 43 disclosures in 2026.

Note :- As shown in the table above, all Rule 42 & 43 reversals go into Table 4(B)(1), while any re-claims must be reported in Table 4(D)(1).

I’ve seen many smart accountants miss this, and it’s the quickest way to get a system-generated notice in 2026.

A. Permanent Reversals (Table 4B1)

These cannot be reclaimed. This includes Rule 42 & 43 reversals (Exempt portion) and Blocked Credits.

B. Temporary Reversals (Table 4B2)

These can be reclaimed later, such as Rule 37 (Non-payment to supplier within 180 days).

The 2026 Re-claim Secret: When you re-claim, you must report in Table 4(A)(5) AND Table 4(D)(1). This double-entry is essential for the Electronic Credit Reversal and Re-claimed Statement (ECRS). Skipping 4(D)(1) will trigger an automated red flag for inconsistent balances.

6. Strategic Checklist for Accountants & CAs

- Interest Income Check: Interest on FDRs or Loans is “Exempt Supply.” You must reverse common ITC against it.

- The 180-Day Tracker: Monitor creditors closely. If unpaid for 170 days, flag for reversal to avoid interest.

- Annual True-Up (Section 50): Every year, re-calculate Rule 42 based on Annual turnover. If you reversed less during the year, pay the balance with 18% interest by November 30th.

GST rules on exempt income are frequently updated by the council. To stay safe from outdated practices, always monitor the Official GST Council Press Releases for the most recent administrative decisions.

Frequently Asked Questions (FAQs)

Q1: Is D_2 (5%) mandatory even if I don’t use assets personally ?

Yes, it is a “deemed” provision under Rule 42 unless you can prove the asset is used exclusively for taxable business.

Q2: What if my Exempt Turnover is zero in a particular month ?

Then D_1 will be zero. However, D_2 (5%) might still apply to common credits unless they are specifically T_4.

Q3: Can we perform the Rule 42 “True-up” or final reconciliation during the GSTR-9 filing ?

Technically, the Law (Rule 42) requires you to finalize the annual re-computation by November 30th of the following financial year. If your annual calculation shows you reversed less ITC during the year, you must pay the balance via DRC-03 with 18% interest. If you reversed in excess, you can reclaim the difference in GSTR-3B before the November deadline.

Q4: Does Rule 42 apply if my main business is 100% taxable but I receive bank interest ?

Yes. Under the GST Law, Bank Interest is treated as an “Exempt Supply”. Even if your primary operations are taxable, the presence of interest income turns your overheads (like Audit fees, Rent, and Tech subscriptions) into Common Credit. Therefore, a proportionate reversal is mandatory to avoid automated system flags.

Q5: What are the consequences of skipping Table 4(D)(1) while reclaiming ITC in 2026?

Under the 2026 ECRS (Electronic Credit Reversal and Re-claimed Statement) framework, skipping Table 4(D)(1) is a high-risk move. Even if you claim the credit in Table 4(A)(5), failing to report it in 4(D)(1) will cause a mismatch in your portal’s reversal ledger. The GST portal’s smarter AI will likely trigger an automated ASMT-10 notice, assuming you are claiming “double credit” without a valid reversal history.

Conclusion

In 2026, GST compliance is about Data Integrity. Rules 42 and 43 are the gatekeepers of your profit. By mastering the 10-step computational chain and keeping your ECRS ledger clean, you build an “Audit-Proof” accounting system that stands up to any scrutiny.

Disclaimer: This blog is for educational purposes. GST laws change frequently. Consult a professional CA for specific case filings.

Meet the Expert

Author Bio: Anurag Panchal is the Founder of AllRoundUpdate & ServiceMoney and a dedicated Financial Educator. With over 135+ technical guides on YouTube, he has helped 10,000+ readers simplify complex GST compliance, Tally Prime workflows, and Digital Marketing strategies through practical, formula-driven insights. Follow his expert masterclasses on YouTube @Educationanurag.